A common way to reassure clients that a worst-case scenario won’t ruin their financial plan is to show how investments recovered after the Great Depression, the tech bubble, or the global financial crisis. The U.S. stock market may stumble, but portfolios recover over the long run.

A common way to reassure clients that a worst-case scenario won’t ruin their financial plan is to show how investments recovered after the Great Depression, the tech bubble, or the global financial crisis. The U.S. stock market may stumble, but portfolios recover over the long run.

But the U.S. is one country – and a country that avoided some serious bad luck that affected other countries during the 20th century. A 2020 paper for the Rodney L. White Center for Financial Research at Wharton showed that investors who base their beliefs about the distribution of possible stock returns on historical data from their home country underestimate the probability of experiencing a significant crash. The authors concluded that the U.S. got lucky, and that this luck may result in underestimating the risk of a significant crash and the extra return we get from accepting investment risk.

Historically, investing in stocks globally has resulted in higher returns on average, especially over longer investment periods. Investors don’t always have a long time horizon, though, and a significant drop in stock prices can wreak havoc on accomplishing many financial goals – for example if a retiree is dealt a bad portfolio return early in retirement. If advisors are underestimating the downside risk by relying too much on the historical resilience of U.S. stocks, they may not be providing investors with an accurate perception of downside risk.

Did the U.S. Get Lucky?

Financial advisors often use historical time periods to provide clients context around how a bad market could impact a financial goal. Using a historical sequence of U.S. investment returns can be far more useful than projecting returns based on historical averages, but we are drawing from a limited sample. We can’t assume scenarios such as the crash during the Great Depression being followed by a historical subsequent boom in the stock market. Actual return sequences outside of the U.S. were much worse.

To estimate how unique U.S. stock market performance has been, we use a relatively new historical dataset that is freely available online: the Jordà-Schularick-Taylor (JST) Macrohistory Database. The JST dataset includes data on 48 real and nominal returns for 18 countries from 1870 to 2020. In this analysis, we focus on historical stock market performance which begins in the year 1872 for the U.S.

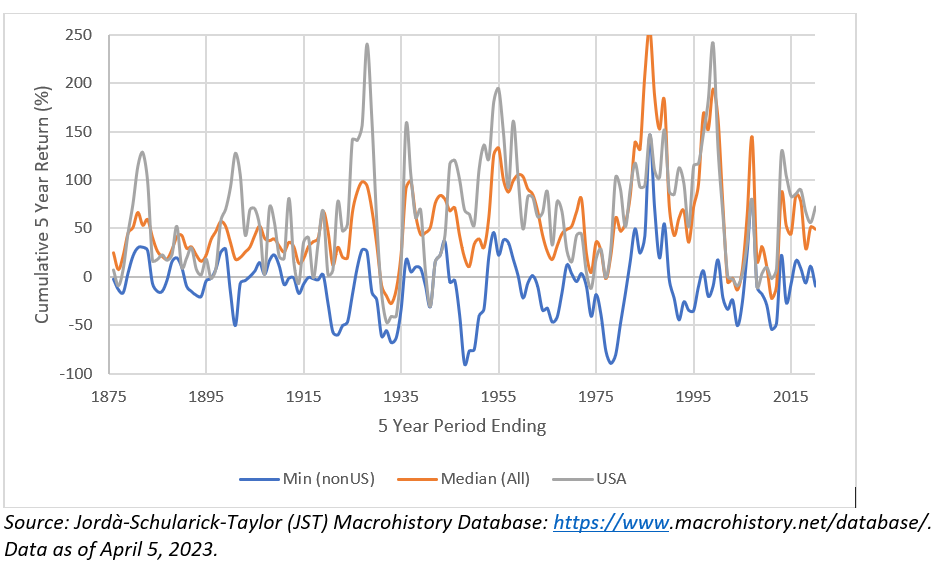

Here is some context on the historical rolling five-year returns of the U.S. stock market versus other countries. The figure below shows the minimum return of all countries with available returns (excluding the U.S.), the median return of all countries, and the return for the U.S. stock market.

Historical Cumulative Five-Year Returns: 1872-2020

Global stock markets have done relatively well historically, with an average cumulative five-year return of 55%, which corresponds to an average annual geometric return of approximately 9.2%. There have been periods of pronounced negative returns, though, especially when looking at the minimum return across all countries.

The U.S. has experienced the lowest cumulative historical return globally during only nine periods, which represent 6% of all potential instances. More importantly, when the U.S. stock market has done relatively poorly, its returns haven’t been that bad – averaging 24% cumulative over those periods. This is the second highest average return when a given country has the lowest return, only behind Australia, which has averaged 26% when it was the lowest returning country.

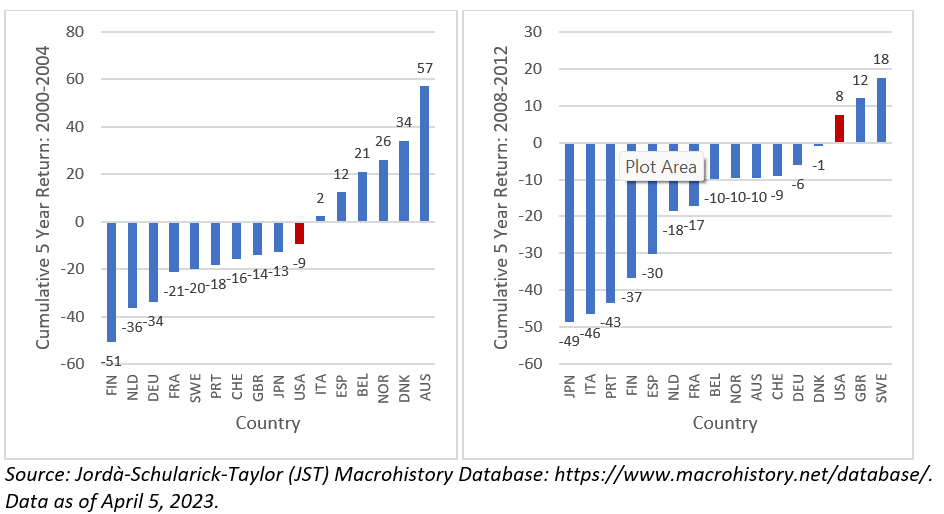

This effect also becomes clearer when we look at specific periods, such as the tech bubble and the global financial crisis, which are commonly used to illustrate a worst-case scenario. This information is included in Panels A and B, respectively, in the Exhibit below (returns for Canada and Ireland aren’t available).

Five-Year Returns for Various Country Stock Markets For Specific Periods

Panel A: Tech Bubble (2000 to 2004) Panel B: Global Financial Crisis (2008-2012)

While the U.S. stock market wasn’t the best performer in either period, it was notably better than other countries. For example, for the five-year period that included the global financial crisis (2008 to 2012 inclusive) the cumulative return for the U.S. stock market was positive (8%) compared to returns that were significantly negative for other countries, for example -49% for Japan.

Historical U.S. returns have been better than other developed countries (barring potentially Australia). In addition, the worst-case scenarios have been far more dramatic for investors outside the U.S. International diversification would have helped many investors who overweighted domestic stocks during a major crash. U.S. investors may hope that we are somehow insulated from the idiosyncratic risk of holding our portfolio in domestic equities, but there is no reason to believe that investors 120 years ago in former economic powerhouses such as the UK, Germany and Russia weren’t equally confident in their domestic equity market.

Coming to terms with equity risk

Stress testing portfolios using historical downturns is a good way to help clients understand how their portfolio will withstand a worst-cast scenario. However, the U.S. didn’t experience a worst-case scenario nearly as dramatic as most countries. The tendency to invest in domestic stocks may appear safer to Americans than the risk experienced by global stock investors. While it is important to use expected returns as the primary input in a financial plan, advisors should be aware that the possibility of extreme losses that could derail a plan isn’t limited to the worst-case scenarios experienced only by U.S. investors.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an adjunct professor of wealth management at The American College of Financial Services and a research fellow for the Retirement Income Institute.

Michael Finke, PhD, CFP®, is a professor of wealth management, WMCP® program director, and the Frank M. Engle Distinguished Chair in Economic Security Research at The American College of Financial Services.

Read more articles by Michael Finke, David Blanchett

A common way to reassure clients that a worst-case scenario won’t ruin their financial plan is to show how investments recovered after the Great Depression, the tech bubble, or the global financial crisis. The U.S. stock market may stumble, but portfolios recover over the long run.

A common way to reassure clients that a worst-case scenario won’t ruin their financial plan is to show how investments recovered after the Great Depression, the tech bubble, or the global financial crisis. The U.S. stock market may stumble, but portfolios recover over the long run.