Silicon Valley Bank suffered probably the quickest bank run in history and the fastest bailout of depositors, too. The lender to the venture capital industry had operated under lighter rules and fewer restrictions than larger banks after a successful lobbying effort back in 2018. Until a few weeks ago, it was judged too small to cause any real damage if it hit problems, but the moment it got into trouble, everyone realized it was systemic after all.

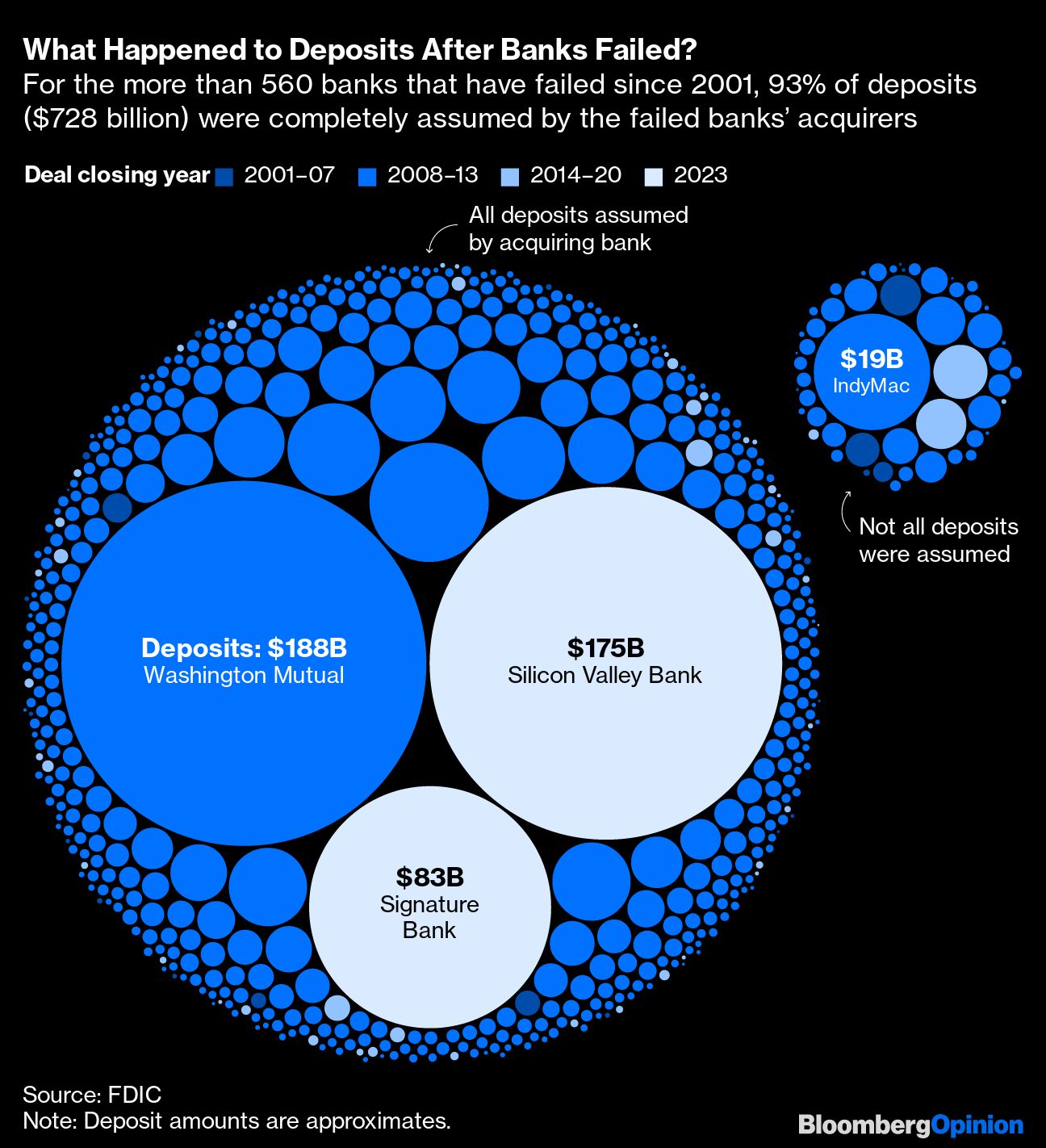

In fact, the scale of SVB’s deposits rescued wasn’t much smaller than Washington Mutual, which failed during the 2008 meltdown and was taken over by JPMorgan Chase & Co. Depositor bailouts aren’t as rare as you might think. In the past 22 years, depositors at failing banks have been helped more often than they have been hurt in bank failures. Typically, a mix of public backstops and white-knight acquirers assume these obligations.

Why did SVB fail? The basic story is that it grew very fast, nearly trebling deposits in just three years, and its managers took too much risk by plowing most of its spare cash into long-term, mainly government-backed, bonds. Then when the Federal Reserve rapidly raised interest rates, the value of these bonds dropped, leaving SVB in need of extra capital.

SVB’s deposits ballooned at a time when investors were throwing money at startups, betting on high returns from future growth while returns on many other assets were suppressed by ultra-low interest rates. Its depositors were similar companies prone to act in similar ways, which would prove part of its downfall. But strong deposit growth and excess cash have been the trend among banks for years. Bank balance sheets have become a lot more liquid and most banks have put a lot more depositor funds into Treasuries and other bonds, just like SVB

A simple way to track this trend is the difference between total deposits and total loans in the US banking system. After the financial crisis of 2008, regulators globally decided that banks needed to be less reliant on funding from financial markets — borrowing from other banks and funds in the form of interbank loans, commercial paper and shot-term bonds. The flightiness of such funding had been a big part of the story of the last crisis. Banks were told they needed more deposit-based funding compared with their hard-to-sell assets, like loans.

The shaded area below shows the growth in excess liquidity on bank balance sheets since 2008. Then, when the Covid-19 pandemic erupted in 2020, the Fed and government combined to unleash a huge infusion of cash into the economy.

The main gauge for investors looking at individual banks is a ratio of loans to deposits. Normally expressed as a percentage, it describes how many dollars of loans a bank has made for each dollar of deposits. The current level for all US banks taken together is 69% - or 69 cents of loans for each dollar of deposits.

Large banks have to meet stricter regulations on the stability of their funding and the sources of liquidity available on their balance sheets to repay depositors, so they tend to have lower loan-to-deposit ratios than smaller banks.

All banks saw deposit growth outpace lending growth during the pandemic and the reopening afterward. People and companies built up savings and paid down debt during lockdowns and then slowly spent excess cash as economic activity began again. But SVB and Silvergate really stand out, they had even more spare cash to manage than peers, so what did they do with it and was it much different to others?

Banks make a choice of how to invest their spare funds. Cash is instantly accessible but typically produces the lowest interest income. Bonds offer a higher return but their values will change with interest rates.

Look at Bank of America Corp. and JPMorgan above. The latter put much more in cash, making it easily available and easy to redeploy. The former put more into securities for a higher interest income earlier, which risked sacrificing the opportunity to invest in higher yielding bonds when rates rose. Bank of America also put more money into bonds that it would hold to maturity: It did this because when rates rose accounting rules for hold-to-maturity (HTM) bonds mean it didn’t have to recognize market value losses in its results. Available-for-sale (AFS) bonds can be sold more easily if a bank wants to invest in higher earning assets instead, but any change in their value has to be reported in results straight away.

For big banks, these decisions are mainly choices between current and future earnings. For SVB and Silvergate, the same choices turned out to be existential.

SVB had 57% of its assets in bonds and other securities at the end of 2022, all of which suffered market-value losses as rates rose. These bonds were extremely unlikely to default, so the valuation changes wouldn't matter unless the bank had to sell them and realize the losses. SVB kept most of its bonds as HTM, to a far greater extent than other banks.

This became SVB's biggest headache. Although it didn’t have to recognize value losses on its HTM bonds, investors could see how big those losses were and how badly SVB would be hurt if it had to sell them.

At the same time, SVB’s deposits stopped growing and started to contract and the bank decided sell a lot of its existing AFS bonds and buy securities with higher yields and shorter maturities. That would free up cash more regularly to reinvest or to make up for shrinking deposits. However, the bonds it sold forced it to crystalize $1.8 billion of market value losses. For its shareholders and some of its clients, this made its huge HTM portfolio more troubling, too.

The rules of accounting say that if you have to sell any HTM bonds, you have to mark all of them to market value. And if SVB was worried enough about deposits to realize such a big loss on its AFS bonds, then maybe it wouldn’t be so long until it had to start selling HTM bonds too. That could mean start a process of realizing more losses than the bank had in capital. The run of the bank began after some venture capital fund managers got worried about this. SVB has since been partly taken over by First Citizens and partly by the Federal Deposit Insurance Corp.

All the other small banks with large bond portfolios have a stronger bias towards AFS holdings, which means they report their market value in their quarterly results. Unlike big banks, however, they don’t have to deduct valuation losses from equity, which means they can appear healthier than they are. If stricter rules had been maintained for smaller banks, that would have reduced the chances of bond valuations turning into a nasty surprise. But at the same time, SVB was far out of line with how most banks behave – big or small.

Methodology: We examined banks in the KBW Bank Index, excluding Bank of Mellon New York and State Street because they are custodial banks and Capital One because it is mainly a credit card company. We also evaluated some banks not in the index, including First Citizens, PacWest, Signature Bank, Silicon Valley Bank, Silvergate and UBS.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.