It’s big news that Envestnet is moving into the RIA custodial space and will soon be competing head-to-head with its biggest integration partners: an expanded Schwab platform, Fidelity and Pershing. I suspect that this is just the first of many so-called software “platforms” that will jump into the custody competition.

It’s big news that Envestnet is moving into the RIA custodial space and will soon be competing head-to-head with its biggest integration partners: an expanded Schwab platform, Fidelity and Pershing. I suspect that this is just the first of many so-called software “platforms” that will jump into the custody competition.

Why? As Jason Wenk of Altruist (what was the newest custodial platform until the Envestnet announcement) put it in a keynote panel discussion at my Insider’s Forum conference, virtually every software vendor is totally reliant on custodial platforms to remain viable. If those custodians decided that they no longer wanted to integrate with the platform's software offerings, all of the software vendor's users would scramble to find an alternative. And it’s possible that the custodian itself will have developed the competing solution – as a nice profitable side business that could effortlessly steal the software vendor’s customer base.

We are repeatedly told that custody is a low-margin business, but that may not be true. If interest rates rise, custodians can earn a decent spread on the sweep accounts and cash balances that advisors have to maintain to collect their fees at the end of the quarter. But the bigger issue, which is the key to Envestnet’s decision to compete with some of its biggest strategic partners, is that when you custody for advisory firms, you have access to them as customers for other products and services – which is where the real money is.

I see Envestnet’s new venture as a protective move. If one of the major platforms decides to sever ties and/or compete with them, it can offer its stranded customers a better custodial deal than they're currently getting (a loss leader?) and maintain control of its own software/solution ecosystem. But second, Envestnet, with a software suite that includes financial planning (MoneyGuidePro), portfolio management (Tamarac), account aggregation (Yodlee) and pipelines to insurance, annuities and TAMP solutions, has far more profitable opportunities per RIA customer than any of the major custodians.

The more customers a custodian can attract, the more cross-selling opportunities it has. To expand market share, Envestnet’s service team could pull together what an RIA firm’s custodian currently is charging clients (in terms of cash spreads, trading costs and other nickels and dimes), and offer more services for less money. If the RIA firm takes itself seriously as a fiduciary, it would have to listen to that offer on behalf of clients.

Orion and Morningstar, the other major platforms, should be watching very carefully how this new move fares in the competitive custodial marketplace, and how their own cross-selling opportunities could be enhanced.

This introduces an entirely new dynamic into our business landscape. We may see the custodial industry migrating into the territory of loss-leader pricing, like how companies will sell ink-jet printers at below their manufacturing price when the real money is in the replacement cartridges.

That, however, raises an interesting question: Is it likely that advisory firms will shift their custodial relationships to these platform options? There are several crosswinds to consider.

The first is the huge recent improvements in onboarding technology. Few advisory firms want to go through the process of repapering their clients – not just because of the hassle in their own offices, but also because they don’t want to put their clients through an unpleasant paperwork experience. But with Nest Wealth and similar features at competing custodians TradePMR and Altruist, the paperwork hassle has been reduced to an online exercise in filling out a questionnaire. Not every advisor firm realizes how easy this has become, but you can bet Envestnet and others will show them. Repapering is shifting from a burden to a hassle to a simple online exercise, and the competitive custodial market will become much more fluid as a result.

The second issue is a continuation of a larger trend, where software companies are creating more pleasant, feature-rich interfaces to traditional services. The obvious comparison is online banks, where a company slaps a more user-friendly front-end onto a traditional banking back office that sits in the background. The platforms, with their comprehensive software suites, will offer a nice contrast to the clunky legacy technology that the larger custodians are constantly wrestling to update. There is a reason why most advisory firms don’t use their custodians’ technology to trade, rebalance, track and report client performance – they use outside software that makes those legacy custodial systems more user-friendly.

A third consideration, and a big one, is that advisory firms are fiercely independent and have traditionally resisted vertical integration, which means having all your software and service provided by a common vendor. No profession understands the value of diversification like advisors. Will advisors put those ancient traditions aside and affiliate with one company to provide them with all (or most) of their software and custodial services?

The accepted wisdom says not just ”no,” but ”hell no.” However, the results of our most recent (2022) T3/Inside Information Software Survey made me wonder if this is still true. Out of the 4,500 responses that Joel Bruckenstein and I collected, just over 20% said they were using one of the all-in-one software packages – Orion, Morningstar Office, Envestnet’s Tamarac, or Advyzon. This represents a huge shift in the marketplace and tells me that tighter integration and operational convenience is a bigger factor, for a growing number of firms, than the once-cherished tech stack diversification.

Adding a more fully integrated custodian to the mix is not out of the question.

Finally, there’s an interesting issue that hasn’t been considered in all the discussion about Envestnet’s new custodial offering: How satisfied are advisory firms with their current custodian (and its technology and service responsiveness)? Are they ready to move?

We’ve all heard about advisory firms griping about how they’ve had to spend up to an hour on the phone just to get in touch with an under-trained Schwab or TD rep, and how smaller RIAs worry that their service teams will be replaced by call centers. But is there any way to measure advisors’ overall satisfaction?

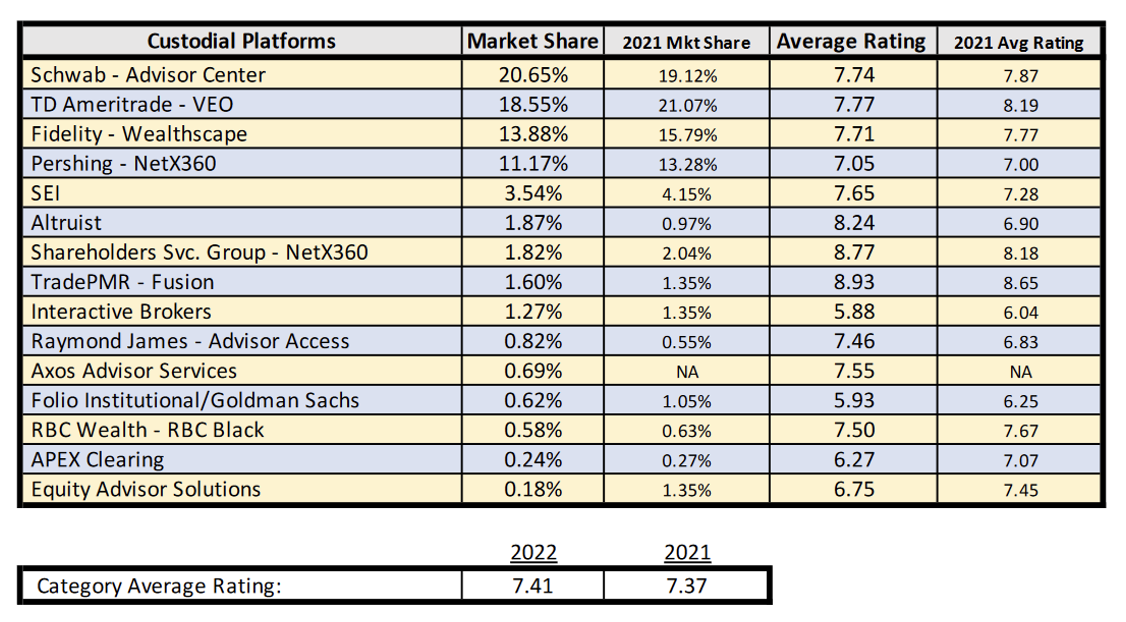

If we turn to page 61 of our 2022 T3/Inside Information Software Survey, we see that Schwab, Fidelity and Pershing achieved average user ratings of 7.74, 7.71 and 7.05 respectively. Those are high marks, which suggest a high level of contentment and little inclination to shift allegiances. I’ve reproduced the full results below. As you can see, some of the smaller custodial competitors are rated even higher; notice TradePMR at 8.93, Shareholders Service Group at 8.77 and Altruist at 8.24. SEI (7.65) and Axos (7.55) have ratings very similar to the Big Three.

Most advisory firms are content with their existing custodial relationships, and if they’re not, there are some good options already in the custodial space for them to consider.

In the short term, Envestnet executives are going to be surprised at how hard it is to move even their most active customers from their existing custodians over to the new in-house platform. They are going to have to cut some deals, and the custodial marketplace will respond by offering better deals of their own, resulting in a slow, inexorable industry-wide custodial margin compression, trench warfare fought through many thousands of individual negotiations with many thousands of RIA firms. Add a couple of additional platforms to this land war, and the RIA world will reap some real cost benefits.

Meanwhile, the much improved, more convenient digital onboarding technology will gradually, as advisors become more aware of them, make custodial relationships less sticky, more fluid. The largest custodians have relied on inertia to maintain their dominant market share, but as they take calls from platforms that offer more user-friendly interfaces and notice that the service levels are better at some of the smaller competitors, we will see a less concentrated custodial landscape.

Let me end by inviting all of you to add to our collective data set and participate in this year’s T3/Inside Information software survey. Once again, among the 38 different software categories, participants can assign a user satisfaction score to their custodial platform (or, if relevant, their broker-dealer).

Here’s the link. Everybody gets a copy of the final report (free of charge), and all of us, Envestnet especially, will be interested to see whether the custodial platforms are as popular this year as they have been in the past.

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com.

It’s big news that Envestnet is moving into the RIA custodial space and will soon be competing head-to-head with its biggest integration partners: an expanded Schwab platform, Fidelity and Pershing. I suspect that this is just the first of many so-called software “platforms” that will jump into the custody competition.

It’s big news that Envestnet is moving into the RIA custodial space and will soon be competing head-to-head with its biggest integration partners: an expanded Schwab platform, Fidelity and Pershing. I suspect that this is just the first of many so-called software “platforms” that will jump into the custody competition.