Lessons from the Markets in 2022

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Every year the markets provide us with lessons on prudent investment strategies. With great frequency markets offer remedial courses, covering lessons they taught in previous years. That’s why one of my favorite sayings is that there’s nothing new in investing, only investment history you don’t know. Investors were provided with a dozen lessons in 2022 (and a bonus one in the postscript). Many of them are repeats from prior years. Unfortunately, too many investors fail to learn them – they keep making the same errors.

Every year the markets provide us with lessons on prudent investment strategies. With great frequency markets offer remedial courses, covering lessons they taught in previous years. That’s why one of my favorite sayings is that there’s nothing new in investing, only investment history you don’t know. Investors were provided with a dozen lessons in 2022 (and a bonus one in the postscript). Many of them are repeats from prior years. Unfortunately, too many investors fail to learn them – they keep making the same errors.

Lesson 1: Just because something hasn’t happened doesn’t mean it can’t or won’t

For many investors, 2022 was a particularly difficult year because it was the first time that both the S&P 500 Index, which lost 18.1%, and long-term Treasury bonds (20-year maturity), which lost 26.1%, experienced double-digit declines. In fact, it was only the third year – 2009 and 2013 were the other two – when long-term Treasury securities produced double-digit losses. And in 2009 the S&P 500 returned 26.5%, and in 2013 it returned 32.4%.

The closest we had come previously to both producing double-digit losses was in 1969, when the S&P 500 lost 8.5% and long-term Treasury bonds lost 5.1%. While the S&P 500 lost 18.1% in 2022 and long-term Treasuries lost 26.1%, resulting in a portfolio loss of 20.3%, it was not the worst year for the “traditional” 60/40 portfolio. That was in 1937, when the S&P 500 lost 35% and long-term Treasury bonds gained just 0.2%, resulting in a portfolio return of -21%.

The fact that both stocks and safe bonds produced large losses was a big surprise to investors who, influenced by recency bias, came to believe that safe bonds were a sure hedge against risky stocks. The data over the period January 2000-November 2022 provided the rationale, as the monthly correlation between the two was -0.2. That led them to believe in what came to be referred to as the “Fed put” – if stocks fell sharply, the Fed would rescue them by lowering interest rates. Unfortunately, for investors who do not know their history, correlations are not constant; they are time varying/economic regime dependent. For example, over the period 1926-1999, the correlation was, in fact, positive at 0.18. Positive correlation means that when one asset tends to produce better-than-average returns, the other also tends to do so. And when it produces worse-than-average returns, the other tends to do so at the same time. With stocks and bonds, time-varying correlation is logical. For example, if we are in an economic regime when inflation is rising from very low levels (such as when coming out of a deflationary recession), stocks will tend to do well as economic activity is picking up, boosting demand, while bonds will tend to perform poorly as rates rise. However, when inflation begins to increase at levels that begin to concern investors (as it did in 2022), stocks can perform poorly at the same time bonds do (1969 was such a year, as the Consumer Price Index rose above 6%).

Looking at the historical data, prior to 2022 there had been five years when both the S&P 500 Index and long-term Treasury bonds produced negative returns (1931, 1969, 1973, 1977 and 2018). There had also been 21 years when the S&P 500 produced positive returns and long-term bonds produced negative returns. And finally, there had been 18 years when the S&P 500 produced negative returns and long-term bonds produced positive returns.

The lessons for investors are to avoid recency bias, know your investment history, and consider diversifying your portfolio to include assets whose risks have little to no correlation with the risks of stocks and bonds – such as reinsurance, long-short factor strategies, trend following, and senior, secured, sponsored, floating rate private credit.

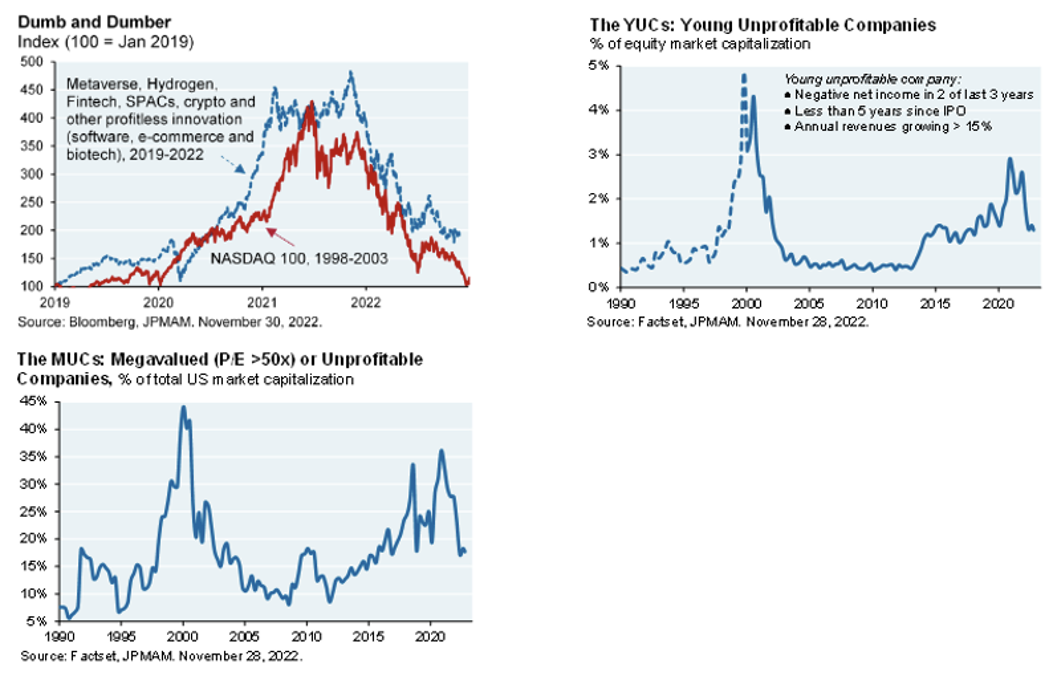

Lesson 2: It’s never different: Young, unprofitable companies are not good investments

While it may be hard to define a financial bubble (and thus know when you are in one), one rule of thumb is that it could be a bubble when you hear the phrase “this time it’s different.” Whenever you hear that, be sure to check the historical evidence because, while something is always different (e.g., an investment with an exciting narrative that captures the public’s attention), the basic principles of investing remain the same. The most recent mania was investing in “disruptive” innovation companies, like those touted by Cathie Wood and owned by ARK Innovation ETF (ARKK).

Investing in young companies (small-cap growth stocks) that are unprofitable but have high investment spending has never been a good strategy. Research/evidence-based investment management firms such Dimensional have long screened out such firms from their eligible universe because their returns have been so poor.

The Wall Street Journal reported that more than one in four of the nearly 600 companies that went public via a traditional IPO in 2020 or 2021 were trading at less than $2 a share as of December 17, 2022. Many of those companies were unprofitable and were valued based on big multiples of expected revenue.

In his December 1, 2022, “Eye on the Markets” article, J.P. Morgan’s Michael Cembalest explained: “Like 2002, 2022 was also a year when unprofitable companies got repriced. The 2019-2022 cycle was arguably ‘dumber’ since there was a historical precedent for this kind of thing.” The three charts below from his article explain why he referred to the mistake of investing in such companies as “dumb and dumber.”

The same “dumb and dumber” tag could be applied to those who bought into the hype around SPACs. As explained in my April 30, 2021, article for Advisor Perspectives, the evidence demonstrates that SPACs fall into the category of products designed to be sold, never bought. Michael Klausner, Michael Ohlrogge and Emily Ruan, authors of the March 2021 study “A Sober Look at SPACs,” concluded: “SPAC sponsors have proposed losing propositions to their shareholders, which is one of the concerns raised by the incentives built into the SPAC structure. … Sponsors do quite well, even where SPAC shareholders have experienced substantial losses.” They added: “It is difficult to believe that it is a sustainable arrangement. At some point, SPAC shareholders will become more skeptical of the mergers that sponsors pitch.” And finally, they stated that, with rare exception, “SPACs are a poorly designed vehicle by which to bring a company public.”

The lesson for investors is that financial suppression through stimulative monetary policy almost always leads to financial folly as investors search for yield/return. As they say, history may not repeat, but it often rhymes.

Lesson 3: Markets are less liquid and thus more volatile

Markets, including even the Treasury bond and municipal markets, became less liquid and thus more volatile in 2022. The reasons are that the dramatic increase in the market share of passive investing has negatively impacted liquidity (passive funds trade infrequently), and because of the regulatory changes made after the great recession (the Volcker Rule), banks can no longer hold significant trading assets on their balance sheets. The result is that banks no longer act as significant providers of liquidity, which has led to increased bid-offer spreads and increased volatility. For example, just over the past few months, there were many single-day moves in the yield on the 10-year Treasury bond that were much larger than had typically been the case. And municipal bond spreads have widened so much that it often made it too expensive to engage in tax-loss harvesting.

Evidence of the reduction in liquidity in stock markets was presented by Xavier Gabaix and Ralph Koijen in their March 2022 study, “In Search of the Origins of Financial Fluctuations: The Inelastic Markets Hypothesis.” They found that today, “investing $1 in the stock market increases the market’s aggregate value by about $5.”

The lesson is that you need to be prepared for higher than historical levels in volatility, as the trend toward increased market share of passive investing isn’t likely to reverse because the evidence favoring it as the winner’s game is overwhelming (recommended reading: The Incredible Shrinking Alpha).

Lesson 4: Gold is not an inflation hedge over most investors’ horizons (nor is bitcoin)

Gold ended 2020 at about $1,894. With many investors concerned about the inflation risks caused by the combination of very stimulative fiscal policy (record budget deficits) and very loose monetary policy (significantly negative real interest rates), they may have looked to gold as a way to hedge that risk. Another factor that may have influenced investor interest in gold was that it had performed extremely well recently (creating recency bias) – in September 2018 it was trading at about $1,300. While the inflation risk was realized, with the CPI increasing by 7% in 2021 and another 7% year-over-year through November 2022, gold actually fell in value over the period, closing at $1,799 in 2021 and at $1,824 in 2022. Thus, while inflation increased by 14% over the two years ending 2022, gold fell 3.7% in nominal terms and by more than 17% in real terms. And in 2022, just when an inflation hedge was needed most, as stocks and bonds produced double-digit losses, in real terms gold fell by more than 5%.

Was gold a good inflation hedge? The following example should help provide an answer. On January 21, 1980, the price of gold reached a then-record high of $850. On March 19, 2002, gold was trading at $293, well below where it was 20 years earlier. The inflation rate for the period from 1980 through 2001 was 3.9%. Thus, gold’s loss in real purchasing power was about 85%. How can gold be an inflation hedge when, over the course of 22 years, it lost 85% in real terms? However, gold has been a good hedge of inflation over the very long run, such as a century. For example, 2,000 years ago an ounce of gold could pay for a Roman centurion’s apparel. Today, an ounce of gold can pay for a good suit of clothes for an executive. Unfortunately, that’s a much longer investment horizon than that of most investors. And it also shows that over the last 2,000 years, gold has provided no real return.

Claude Erb and Campbell Harvey, authors of the 2016 study, “The Golden Constant,” examined the historical evidence on gold as an inflation hedge and concluded: “While gold might protect against inflation in the very long run, 10 years is not the long run. In the shorter run, gold is a volatile investment which is capable and likely to overshoot or undershoot any notion of fair value.”

Turning to bitcoin, since its creation crypto investors and advocates have promoted it as a hedge against inflation and a store of value against fiat currency given that it has a fixed supply of 21 million bitcoins. Bitcoin ended 2021 at $46,306 and ended 2022 at $16,591. While inflation increased 6.5%, bitcoin fell about 64% in nominal terms and thus lost more than 70% in real terms. Again, just when inflation hedging properties were needed most, bitcoin collapsed in price.

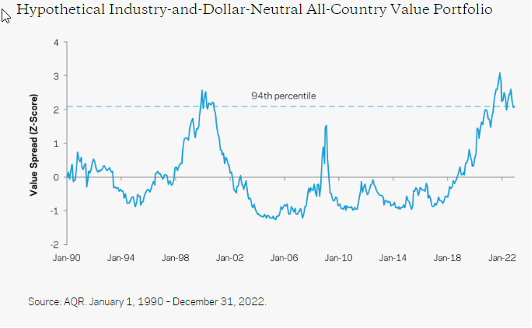

Lesson 5: This time is not different: Value investing is not dead

Value investing is the age-old investment strategy that buys securities that appear cheap relative to some fundamental anchor. There is a large body of academic research demonstrating that the value premium has been persistent over long periods; pervasive across asset classes (stocks, bonds, commodities and currencies) and also across and within industries, countries and regions; robust to various fundamental metrics; and is implementable (survives transactions costs). In addition, there are intuitive risk- and behavioral-based explanations for why the premium should be expected to persist. Andrew Berkin and I presented the evidence in Your Complete Guide to Factor-Based Investing. However, the performance of value in equities, especially U.S. equities, over the recent past called into question whether the value premium was dead.

Consider the following. From July 1926 through October 2016, the Fama-French U.S. value research index outperformed its growth counterpart by 3.4 percentage points per annum (12.8% versus 9.4%). And from 2000 through October 2016, the outperformance was a virtually identical 3.2% (7.5% versus 4.3%). Then the value premium underwent its largest drawdown in history. Over the four years November 2016-October 2020, the value research index underperformed by 16.9 percentage points per annum (20.4% versus 3.5%). That relatively brief four-year period led many pundits to declare the death of the value premium – and many investors fled value stocks. Those who did so ignored the long-term evidence and the fact that all risk assets go through long periods of poor performance.

Over more than 25 years as an investment advisor, I’ve learned that one of the greatest problems preventing investors from achieving their financial goals is that when it comes to judging the performance of an investment strategy, they believe that three years is a long time, five years is a very long time, and 10 years is an eternity. Even supposedly more sophisticated institutional investors, including those that employ highly paid consultants, typically hire and fire managers based on the last three years’ performance. This tendency causes investors to make the critical mistake of engaging in “resulting” – the assumption that good outcomes are the result of a good process and bad outcomes the result of a bad process.

While investors consider 10 years to be an eternity, financial economists know that when it comes to investment returns involving risk assets, 10 years can be nothing more than “noise,” a random outcome. For example, we have had three periods of at least 13 years over which the S&P 500 underperformed totally riskless one-month Treasury bills: 1929-43, 1966-82 and 2000-12. Those abandoning value were likely also ignoring the fact that value had been through a similar “dark winter” not long ago during the dot-com era. From 1998 through 1999, the Fama-French U.S. value research index underperformed its growth counterpart by 23.6 percentage points per annum (8.4% versus 32.0%).

Explaining value’s underperformance

As Ronen Israel, Kristoffer Laursen and Scott Richardson of AQR Capital Management explained in their 2020 paper, “Is (Systematic) Value Investing Dead?”: “Value strategies ‘work’ when the wedge between fundamental value and price converges. For a value investor this primarily comes from prices reverting to fundamentals. Value could also ‘work’ by buying cheap cash flows with prices remaining unchanged. If fundamentals converge to price, or the wedge between price and fundamentals continues to grow, value strategies will ‘not work’. This can happen when stock prices respond less to fundamental (cash flow) news.”

They explained: “Changes in expectations of fundamentals matter for stock returns, particularly when examining return intervals of a year or longer. Similarly, expected returns are strongly associated with realized returns after conditioning for cash flow news.” They noted that the two major exceptions were the latter part of the dot-com period (1998 and 1999) and the period they were still in the middle of (late 2016 through late 2020). Those were periods when the stock market placed less weight on fundamental information. What mainly drove returns in both of the dark winters for value stocks was multiple expansion (what John Bogle called the “speculative return”), not changes in fundamentals. They concluded: “When value underperforms the most, it is due to a combination of deterioration in fundamentals of cheap stocks (but not too much greater than normal) and a widening in the gap between prices and fundamentals (but considerably more so than average).” They added: “Fundamentals do matter for stock returns, but there are periods where stock prices become less connected with fundamental information, and in such periods value strategies underperform. This has happened before, is happening now, and will likely happen again. However, absent a crystal ball allowing an investor to know ahead of time if the market is less in tune with fundamentals, the implication for value strategies is not clear.”

Having patience and the wisdom to rely on long-term historical evidence – not falling prey to recency bias, not chasing yesterday’s winners, and tuning out the “this time is different” stories spun by the financial media – are the keys to being a successful investor. Those with the patience and wisdom to stay the course have been rewarded: Over the period November 2020-November 2022, the value research index outperformed its growth counterpart by 28.2 percentage points per annum (35.4% versus 7.2%). As can be seen in the following chart, while value outperformed by a wide margin since November 2020, it is still trading at historically cheap levels relative to growth – and relative valuations are the best predictor we have of future premiums.

Lesson 6. Don’t make the mistake of recency; last year’s winners are just as likely to be this year’s dogs

The historical evidence demonstrates that individual investors are performance chasers – they buy yesterday’s winners (after the great performance) and sell yesterday’s losers (after the loss has already been incurred). This causes investors to buy high and sell low – not a recipe for investment success. As I wrote in my book, The Quest for Alpha, that behavior explains the findings from studies that show investors can actually underperform the very mutual funds in which they invest. For example, as cited in The Quest for Alpha, a 2005 study published by Morningstar FundInvestor found that in all 17 fund categories they examined, the returns earned by investors were below the returns of the funds themselves. Unfortunately, a good (poor) return in one year doesn’t predict a good (poor) return the next year. In fact, great returns lower future expected returns, and below-average returns raise future expected returns.

A “poster child” for the recency mistake is Cathie Wood’s ARK Innovation Fund (ARKK). The fund’s inception was November 2014. While the fund performed poorly in its first two full years (Morningstar percentile ranking of 75 in 2015 and 98 in 2016), at that point the fund had only about $200 million of assets under management (AUM). The fund performed well in 2017, earning a 1st percentile ranking (returning 87.3%), and again in 2018, earning a 17th percentile ranking (even though it gained just 3.5%). In 2019 ARKK’s performance reverted, earning a 57th percentile ranking even though it returned 25.6%. From inception through 2019, ARKK earned 20.6% per annum versus 11.8% for VOO. That type of performance attracts investors who believe the past performance of active managers is a predictor of future performance, and AUM grew to about $1.9 billion.

ARKK turned in a spectacular performance in 2020, earning a 1st percentile ranking, returning 153%. AUM grew to about $21.5 billion. And cash continued to flood in; by February 12 the fund was up about 25% for the year. AUM reached a peak of about $28 billion that month. Unfortunately for investors, the fund lost 23.6% for the full year, earning it a 100th percentile ranking. And investors who continued to pour money into the fund in early 2021 did much worse, as the fund lost about 37% from its peak on February 12. AUM had fallen to about $16 billion at year’s end, falling by far more than the losses alone could explain as some investors abandoned ship. In other words, the strongest performance came when assets were just a small fraction of what they had been when the fund had its worst performance. It is often the case that the mistake of recency leads to investor returns that are below the reported returns of the funds in which they invest. Sadly, for ARKK investors 2022 was even worse than 2021, as the fund once again finished in the 100th percentile, losing almost 67%. And assets had fallen to $6 billion by year’s end. Morningstar also shows that the fund’s performance put it in the 99th percentile over the last five years.

The following table compares the returns of various asset classes in 2021 and 2022. Sometimes the winners and losers repeated, but other times they changed places. For example, the best performer in 2021, U.S. REITs, finished in last place in 2022.

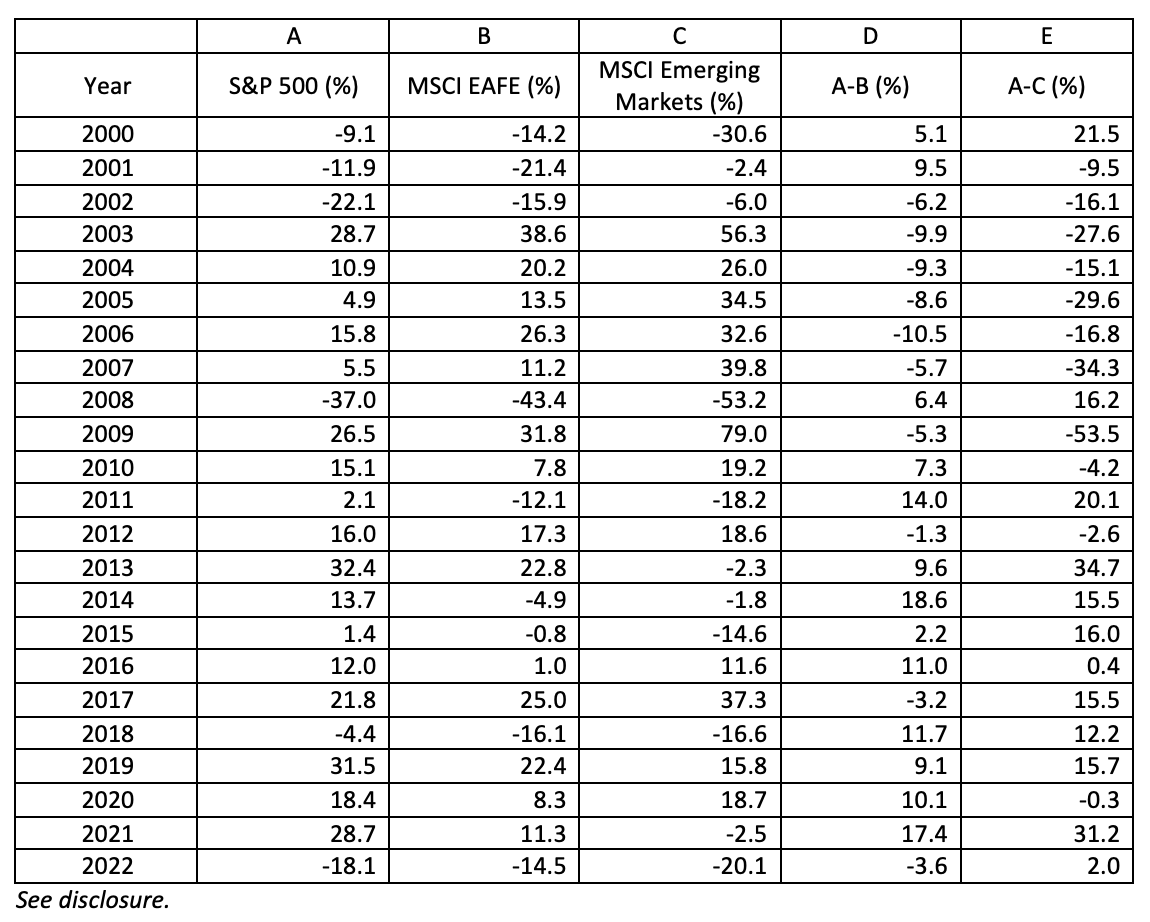

Lesson 7: The investment world isn’t flat, and the diversification of risky assets is as important as ever

The great recession caused the correlations of all risky assets to rise toward 1. This led many in the financial media to report on the “death of diversification” – because the world is now flat (interconnected), diversification no longer works. This theme has been heard repeatedly since 2008. Yet, diversification benefits come not just from correlations but from the dispersion of returns as well. And a wide dispersion of returns in almost every year since 2000 demonstrates there are still large diversification benefits.

There were only four years of the 23 when the difference in returns between the S&P 500 Index and the MSCI EAFE Index was less than 5 percentage points. On the other hand, there were 13 years when it was at least 8 percentage points. In only six years was the return on the S&P 500 Index within 10 percentage points of the return of the MSCI Emerging Markets Index. There were eight years when it was at least 20 percentage points and four when it was at least 30 percentage points. The largest gap was more than 53 percentage points. The data presents powerful evidence that the investment world is far from flat and that there are still significant benefits in international diversification.

Lesson 8. It has become riskier to short stocks

Short sellers play a valuable role in keeping market prices efficient by preventing overpricing and the formation of price bubbles in financial markets. This promotes both market efficiency and an efficient allocation of capital across risky assets. If short sellers were inhibited from expressing their views on valuations, securities prices could become overvalued (as only the optimists would be able to express their views), and excess capital would be allocated to firms favored by the most optimistic investors.

The importance of the role played by short sellers has received increasing academic attention in recent years. Research into the information contained in short-selling activity – including the 2016 study, “The Shorting Premium and Asset Pricing Anomalies,” the 2017 study, “Smart Equity Lending, Stock Loan Fees, and Private Information,” the 2020 studies, “Securities Lending and Trading by Active and Passive Funds” and “The Loan Fee Anomaly: A Short Seller’s Best Ideas,” and the 2021 study, “Pessimistic Target Prices by Short Sellers” – has consistently found that short sellers are informed investors who are skilled at processing information (though they tend to be too pessimistic).

While short sellers play a valuable role in keeping market prices efficient by preventing overpricing and the formation of price bubbles in financial markets, it is the limits to arbitrage, the high risks and high costs of shorting that allow some inefficiencies to persist, explaining the information provided by short sellers. The recent GameStop episode in which retail investors banded together to engineer a short squeeze demonstrated just how risky shorting can be, with the potential for unlimited losses. That type of risk, with retail investors using social media to band together with sufficient capital to attack the short positions of well-capitalized hedge funds, was one that had never been experienced and almost certainly was not expected.

Compounding the risks of shorting is that, as noted in lesson 3, markets have become less liquid and thus more inelastic and more volatile. As noted, the authors of the March 2022 study, “In Search of the Origins of Financial Fluctuations: The Inelastic Markets Hypothesis,” found that today, “investing $1 in the stock market increases the market’s aggregate value by about $5.” The reduced liquidity increases the risk of shorting. Adding further to the risk is the now-demonstrated ability of retail investors to “gang up” against shorts (who might be right in the long term, but dead before they reach it). The bottom line is that the limits to arbitrage have now increased, allowing for more overpricing of what can be called “high sentiment” stocks, making the market less efficient and increasing the likelihood of bubbles occurring in the future, as overvaluation is more likely to persist.

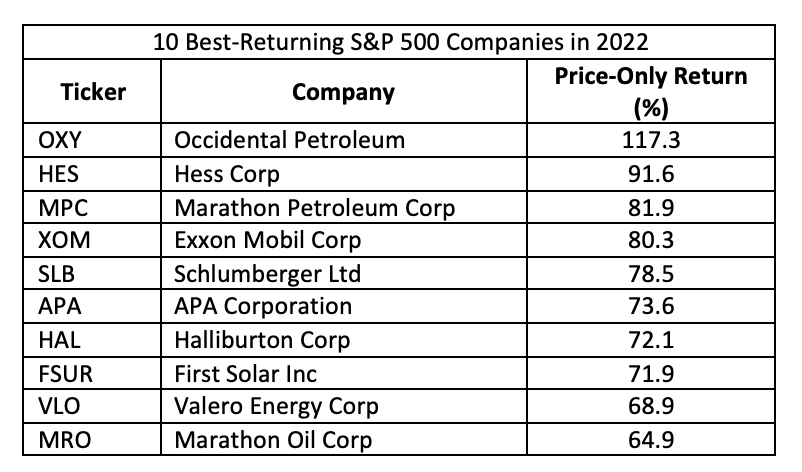

Lesson 9: Active management is a loser’s game in bull or bear markets

Despite an overwhelming amount of research (summarized in The Incredible Shrinking Alpha) demonstrating that passive investing is far more likely to allow you to achieve your most important financial goals, the vast majority of individual investor assets are still held in active funds. For example, S&P’s U.S. Persistence Scorecard Mid-Year 2022 concluded: “Regardless of asset class or style focus, active management outperformance is typically relatively short-lived, with few funds consistently outranking their peers.” Unfortunately, investors in active funds continue to pay for the triumph of hope over wisdom and experience.

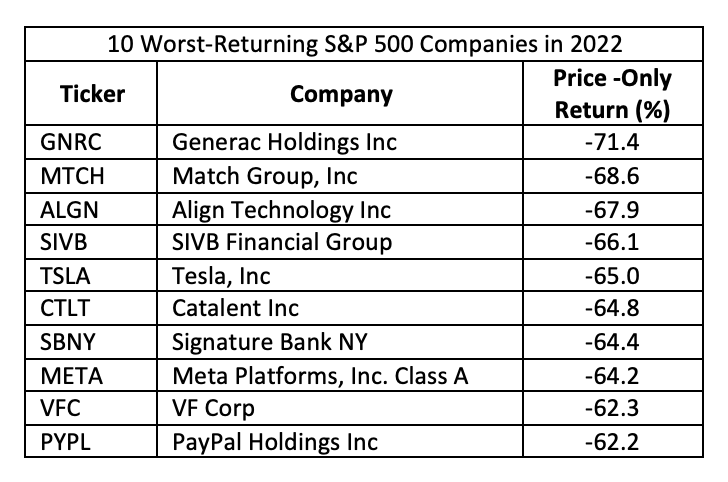

Last year was another in which the majority of active funds underperformed despite the fact that the industry claims active managers outperform in bear markets. In addition to their advantage of being able to go to cash, active managers had a great opportunity to generate alpha through the large dispersion in returns between 2022’s best-performing and worst-performing stocks. For example, while the S&P 500 Index lost 18.1% for the year, including dividends, in terms of price-only returns, the stocks of 10 companies were up at least 64.9%. The following table, with data from S&P Dow Jones Indices, shows the 10 best returners:

To outperform, all an active manager had to do was to overweight those big winners, each of which outperformed the index by at least 83%. On the other hand, 10 stocks lost at least 62.2%, with the worst performer losing 71.4% on a price-only basis.

To outperform, all an active manager had to do was to underweight, let alone avoid, these dogs, each of which underperformed by at least 44%.

This wide dispersion of returns is not at all unusual. Yet, despite the opportunity, year after year in aggregate, active managers persistently fail to outperform. Because indexes don’t incur expenses, while funds do, we need to compare the performance of active funds to those of live index/systematic funds. The following table shows the Morningstar percentile rankings for funds from two leading providers of passively managed funds – Dimensional (which are managed in a systematic, transparent and replicable manner) and Vanguard (which are index funds) – in 2022 and over the 15-year period ending December 2022.

|

Fund |

2022 Percentile Ranking |

15-Year Percentile Ranking |

|

Domestic |

||

|

Vanguard 500 Index (VFIAX) |

51 |

15 |

|

DFA U.S. Large Company (DFUSX) |

52 |

16 |

|

Vanguard Value Index (VVIAX) |

21 |

24 |

|

DFA U.S. Large Cap Value III (DFUVX) |

50 |

25 |

|

Vanguard Small Cap Index (VSMAX) |

62 |

17 |

|

DFA U.S. Small Cap (DFSTX) |

23 |

13 |

|

DFA U.S. Micro Cap (DFSCX) |

18 |

23 |

|

Vanguard Small Cap Value Index (VISVX) |

39 |

16 |

|

DFA U.S. Small Value (DFSVX) |

11 |

20 |

|

Vanguard Real Estate Index (VGSLX) |

59 |

35 |

|

DFA Real Estate Securities (DFREX) |

26 |

26 |

|

International |

||

|

Vanguard Developed Markets Index (VTMGX) |

46 |

33 |

|

DFA Large Cap International (DFALX) |

17 |

31 |

|

DFA International Value III (DFVIX) |

8 |

29 |

|

DFA International Small Company (DFISX) |

17 |

19 |

|

DFA International Small Cap Value (DISVX) |

26 |

20 |

|

Vanguard Emerging Markets Stock Index (VEIEX) |

30 |

49 |

|

DFA Emerging Markets I (DFEMX) |

25 |

23 |

|

DFA Emerging Markets Value I (DFEVX) |

5 |

40 |

|

DFA Emerging Markets Small Cap I (DEMSX) |

18 |

2 |

|

Average Vanguard Ranking |

44 |

27 |

|

Average DFA Ranking |

23 |

22 |

Morningstar’s data contains a significant amount of survivorship bias, as it only reflects funds that have survived the full period. About 7% of actively managed funds disappear every year, their returns buried in the mutual fund graveyard. Thus, the longer the period, the worse the survivorship bias becomes, and at 15 years it’s a large degree. For taxable investors, the data is even more compelling because taxes are typically the highest cost of active management. Thus, the survivorship bias-free, after-tax rankings for Vanguard and Dimensional funds would be significantly better.

The results make clear that active management is a strategy that can be “fraught with opportunity.” Year after year, active managers come up with an excuse to explain why they failed, and then argue that next year will be different. Of course, it never is.

Despite the fact that Dimensional’s funds have higher expense ratios than Vanguard’s, their percentile ranks were higher in both 2022 and over the 15-year period ending 2022. The lesson is that while expenses are important, they should not be the only criteria you consider when selecting a fund that will provide exposure to the asset class/factors you are accessing.

Lesson 10: The (Il)liquidity premium is not a free lunch

Liquidity refers to how easily an investment can be converted to cash. Assets with public markets, such as listed stocks, ETFs and U.S. Treasury bills, are considered highly liquid because they can usually be sold at any time at the prevailing market price. On the other hand, assets such as real estate, private equity, venture capital and many debt instruments are understood to have low liquidity. The liquidity premium, then, is a risk premium – the incremental return compensating investors for owning an asset that is not highly liquid (commonly referred to as an “illiquidity premium”). And the illiquidity risk typically appears during difficult economic times, just when investors may desire liquidity – it is not a free lunch, but compensation for taking incremental risk.

Investors were provided a remedial course in 2022 in the illiquidity premium, as several interval funds (such as Stone Ridge’s Reinsurance Risk Premium Interval Fund, SRRIX, and its Alternative Lending Risk Premium Fund, LENDX, and some large private funds such as Blackstone’s and Starwood’s private real estate funds, BREIT and SREIT) were “gated,” limiting redemptions (either monthly or quarterly), to their required minimums.

The redemption limitations of illiquid funds are features, not bugs, of such vehicles. They are there to protect patient and disciplined investors from bearing the costs of panicked selling into illiquid markets by those less patient and disciplined. Without such limitations, investors would be unable to access these asset classes and gain both the diversification benefits they provide and the opportunity to earn the illiquidity premium.

The lesson for investors is that the first caveat to investing in illiquid assets is that it is only appropriate for the portion of investments the investor can afford to allocate to illiquid holdings.

Lesson 11: Credit quality matters – a lot

With interest rates on riskless Treasury bills remaining close to zero – and rates on FDIC-insured CDs not much higher – through much of the early months of the year, many yield-hungry investors were attracted by the double-digit interest rates offered on U.S. dollar-pegged “stablecoins.” The mistake those investors made was believing that the stablecoins were in fact fully backed by high-quality dollar assets, making the risk of losing money seem small.

Investors in the algorithmically based “stablecoin” TerraUSD learned the lesson about credit quality the hard way. TerraUSD began 2022 trading at $1. And it maintained that level, or very close to it, until early in May, when it became untethered and crashed. By year’s end it had lost 98% of its value. The TerraUSD was linked to a sister token, Luna, whose price was set by the market. At the start of the year, Luna was trading at about $98. By year’s end it was trading at $0.00013. At their height, Luna and the TerraUSD had a combined market value of almost $60 billion. Now they’re essentially worthless, making them the purveyors of perhaps the most expensive lesson in financial history.

Tether and many other of the largest cryptocurrencies maintain, at least in theory, a reserve of cash or cash-equivalent assets whose value matches the total value of the stablecoin in circulation – when a user pays Tether $1 for a token, that money is supposed to be held in Tether’s bank accounts. (However, in October 2021, Tether agreed to pay a $41 million civil monetary penalty after the U.S. Commodity Futures Trading Commission found that the company did not back up the stablecoin appropriately – it had reserves to fully back USDT in circulation only for 27.6% of the days between September 2016 and November 2018.) Other stablecoins, like MakerDAO’s DAI, maintain a reserve of cryptocurrencies (whose values can fluctuate wildly, or even crash toward zero) rather than traditional money. However, none of those stablecoin deposits are backed by FDIC insurance, and they don’t carry credit ratings like corporate bonds do, allowing investors to judge the quality of the assets/collateral. And the crypto markets have been unregulated.

The lesson for investors is that credit quality matters a lot, and there is no substitute for the guarantees of Treasury obligations or FDIC insurance, or at the very least a credible credit rating of the issuer.

Lesson 12: Ignore all market forecasts from so-called gurus

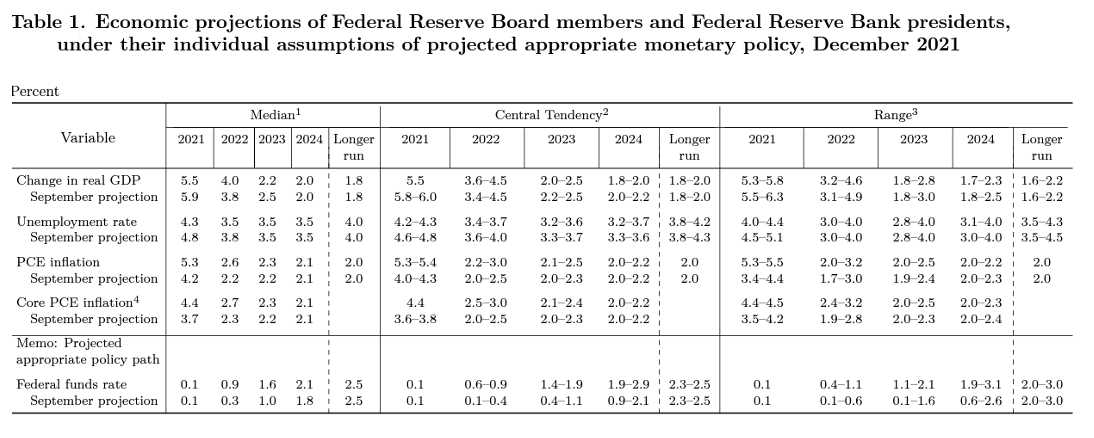

The following chart shows the Federal Reserve’s forecast of the number of interest rate increases it would implement and the implied forward rates. It shows that the Fed believed they would increase rates just three times and that their policy rate would end the year below 1%.

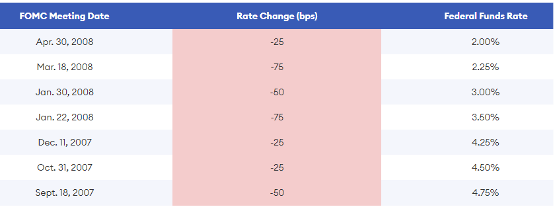

As the table below shows, the Federal Reserve raised the Fed funds rate seven times in 2022, ending the year with the target rate at 4.25%-4.50%. If the Federal Reserve, which sets the Fed funds rate, can be so wrong in its forecast, it doesn’t seem likely that professional forecasts are likely to be accurate in theirs.

This example demonstrates that market movements are often dominated by surprises, which by definition are unforecastable. One of the surprises, at least to the Fed, was that inflation turned out to be much higher than its forecast. Its December 2021 forecast for 2022 inflation, as can be seen in the table below, was for the core CPE to be between 2.5% and 3.0%. Inflation turned out to be more than double that. It was also wrong in its forecast of real GDP growth of 3.4%-4.5%. The real GDP fell 1.6% in the first quarter, and fell another 0.6% in the second, before growing 3.2% in the third.

If the economic forecast isn’t right, it isn’t likely a market forecast is right. How did the professional forecasters do with their predictions for the S&P 500? In December 2021 Reuters polled 45 market strategists asking for their prediction for the S&P 500 in 2022. Their median forecast called for the S&P 500 to end 2022 at 4,910, a gain of 7.5% from its close at the time. With the S&P 500 ending the year at 3,840, the median forecast was only 28% too high.

The evidence on the inability of professionals to accurately forecast markets is what led Warren Buffett, in his 2013 letter to Berkshire shareholders, to issue this warning: “Forming macro opinions or listening to the macro or market predictions of others is a waste of time. Indeed, it is dangerous because it may blur your vision of the facts that are truly important.”

One of my favorite sayings about the market forecasts of so-called experts is from Jason Zweig, financial columnist for The Wall Street Journal: “Whenever some analyst seems to know what he’s talking about, remember that pigs will fly before he’ll ever release a full list of his past forecasts, including the bloopers.” You will almost never read or hear a review of how the latest forecast from some market guru actually worked out. The reason is that accountability would ruin the game – you would cease to “tune in.”

The lesson for investors is to tune out the forecasts of market strategists and adhere to your well-thought-out investment plan, rebalancing and tax-loss harvesting along the way.

Summary

Even smart people make mistakes. What differentiates them from fools is that they don’t repeat them, expecting different outcomes. 2023 will surely offer us more lessons, many of which will be remedial courses. The market will provide opportunities to make investment mistakes. You can avoid them by knowing your financial history and having a well-thought-out plan. Reading my book, Investment Mistakes Even Smart People Make and How to Avoid Them, will help prepare you with the wisdom you need. And consider including in your New Year’s resolutions that you will learn from the lessons the market teaches.

My greatest hope is that you have learned that the key to successful investing is to get the plan right in the first place, and then stick to it. That means imitating the lowly postage stamp, which does one thing but does it well – sticking to its letter until it reaches its destination. Your job is to stick to your well-developed plan until you reach your financial goals. And if you don’t have a plan, write one immediately, and make sure the plan includes the actions you are prepared to take if the “unexpected” happens (your “Plan B”).

Postscript

The markets offered another remedial course in 2022: Success, whether on the field or on the screen, doesn’t always translate into investment success. In other words, don’t be fooled by celebrity endorsements. For example, these celebrities all appeared in ads promoting cryptocurrency: Tom Brady (in April he purchased a Bored Ape NFT #3667 for $430,000, and on December 19th the price was about $76,000, a loss of more than 80%); Larry David (after the price of crypto started collapsing, Jeff Schaffer, David's longtime collaborator and the director of the commercial, told the New York Times that neither he nor David knew much about crypto); Jimmy Fallon; Lebron James; Kim Kardashian (who was fined $1.26 million by the SEC for failing to disclose that she was paid $250,000 for promoting an Ethereum cryptocurrency); Matt Damon; Floyd Mayweather (in 2018 he agreed to pay the SEC more than $600,000 in fines for failing to disclose payments he received for promoting initial coin offerings); Seth Curry; Reese Weatherspoon; and many others. Familiarity or admiration are not a substitute for evidence-driven advice.

Larry Swedroe is the head of financial and economic research at Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party sources which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Total return includes reinvestment of dividends and capital gains. Mentions of securities are to demonstrate passive funds versus active funds, and low-cost funds. The mentions of specific securities should not be construed as recommendations of securities. Performance is historical and past performance is not an indication of future results. Alternative securities mentioned are for informational purposes only and should not be construed as a recommendation. Alternative funds present unique risks including liquidity risk. For full information ask a financial professional. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements, or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability, or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. LSR-23-435

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All