Financial Planning Needs a Makeover!

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Usually when people (like me) rail on the planning profession for being non-transparent, they are referring to annuities, crypto, private REITs, etc. Here’s a new take: Financial planning can be opaque, vague, and perceived as non-valuable by the consumer. I’m about to give financial planning a transparency makeover.

Usually when people (like me) rail on the planning profession for being non-transparent, they are referring to annuities, crypto, private REITs, etc. Here’s a new take: Financial planning can be opaque, vague, and perceived as non-valuable by the consumer. I’m about to give financial planning a transparency makeover.

Get out that eyelash comb!

Nobody knows what financial planning is

Do you remember the children’s book entitled Are You My Mother?

My dad used to read it to me. It’s about a baby bird whose mom flies away from the nest, causing it to wander around lost, needlessly asking the same question to a bulldozer, a dog, etc., “Are you my mother?” I am on a similar mission with this question, “What is financial planning?” Every time I ask someone, the person responds back with a confused expression as if I’ve asked them something absurd.

I remember a close friend of mine and his wife hired an advisor I recommended. We’re sitting on my couch watching our kids play, and he says, “Thanks for introducing us to Steven. He’s going to get started on our portfolio after he does our financial plan.”

“Financial plan – whatever that means!” chimes in his wife from the kitchen, “Do you want lettuce or tomato on your sandwich?”

Another time, an older relative of mine was telling me about her first meeting with a financial advisor. “He wants to sell my stocks and buy some mutual funds or somethings. And then I have to pay another $4,000 for a financial plan. Do you think I need it? I’ve already retired. What else is there to plan for?”

Listen to that.

Just listen for a minute to what people are saying.

And here’s a direct quote from the Ongoing Financial Planning Guide from the Colorado Division of Securities:

Staff has found advisers unable to produce documentation demonstrating the financial planner-provided services to clients, the detailed accounting of fee to work deliverables, itemized invoices as well as clear and detailed fee schedules.

See, even they’re dubious there is any deliverable here!

Does anyone know what financial planning is?

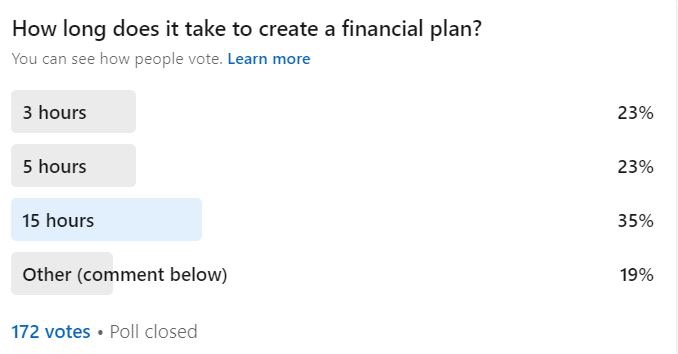

Not even advisors do! I asked a group of advisors in my LinkedIn network how long it takes to create a financial plan and I got responses of 1.5 hours to 30+ hours.

How can that be?

Are you my mother?

Where is my mother?

I’ve got to find her before she gets sold some one-hour financial plan, lol!

New hairstyle and eye makeup for financial planning!

Confusion translates into lack of value. Without clarity about what it is, it’ll just be seen as a “nice to have” as the previous examples illustrated, never taken as seriously as it should be.

Somebody has to defend financial planning – so I will.

Here are the components of the financial planning “makeover”:

- Regulators at the state and federal level have to understand what it entails.

- Fees should be charged that correlate with its value.

- Advisors have to adopt new terminology when they discuss it.

A free lip gloss and hairbrush are included and, even better, it’ll be manufactured cruelty-free for all of you in the woke crowd. 😂 😂 😂

1. Regulators need to be brought up to speed

The regulators have no idea what a financial plan is. Can you blame them? Look at what we’ve taught them about ourselves.

Imagine you are the Alabama state securities commissioner – we’ll use the name “Mrs. Alabama” for the purpose of this article (doesn’t that sound like we’re at a pageant?).

In your work, you deal with advisors daily and you audit ADVs where you are constantly reading some of the following:

“We charge a monthly retainer fee (but can’t document any of the work done).”

“We charge a fee for service (when it’s a one-time plan).”

“We are financial planners in Bethesda, Maryland. We charge an AUM fee which includes investment management and financial planning.”

“We didn’t deliver any actual tangible services this month but we were available for questions.”

Mrs. Alabama then goes to dinner with her husband, who is a physician. Over the filet mignon he says, “Today the guy who sold me my disability insurance came in and said he wanted to review my policy. He said he’d do a financial plan for free! Isn’t that sweet?”

(Are you my mother?…)

Really, people, can you blame them for being totally confused and skeptical of planning?

How about this for a new eyeshadow pallet?

- They’re not “registered investment advisers”; they are financial planners. Financial planners are regulated by the Investment Advisors Act of 1940. This is highly illogical and moreover confusing for everyone involved. Ideally there should be a separate, codified body of law governing the provision of financial planning, promulgated by a regulatory organization dedicated to financial planning, not by parties like the CFP Board with a political agenda such as making their (highly insurance-biased) code become the standard for the entire profession.

- Financial planning needs better lobbying. Look at how strong the insurance lobby is, and it gets everything it wants. It got annuities into 401k plans, for goodness sake!

- Exercise our democratic rights as U.S. citizens. Start by contacting our Congressional staffers. Last weekend I emailed my senator, Chuck Schumer. I contacted other Congressional offices and, to my surprise, in some cases I was able to get through.

- It takes as much time to complain to your friends at the FPA conference or on social media as it does to the government. If you have opinions, do that instead. You can submit comments to the SEC on proposed rules, rulemaking petitions, etc.

In a recent Senate Banking committee hearing, Senator Sherrod Brown said, “Our democratic institutions are only as strong as the people who empower them.” (Forbes, November 2022)

The United States is not a dictatorship. It’s still “by the people, for the people.” We don’t work for the lawmakers; they work for us. If there is an aspect you disagree with, it is your right as an American to empower policymakers with education and knowledge. If the point is made with enough strength you’d be surprised how far it can go.

2. Fees should correlate with services

Financial advisor: We put planning first, as it is the foundation for everything we do for you

Financial advisor also: That is why our fees are assessed as a % of your AUM 🤣

Now I know that some of y’all are going to argue with me on this until the end.

Having a financial plan paid for with:

- Commissions;

- A fee that relates to the size of the client’s portfolio; or

- Nothing (free, not paid for at all, given away to convince you to buy whole life insurance)

doesn’t make logical sense.

Financial planning, if it is ever going to command the respect it deserves, can only be paid for with fees that are specifically correlated with the services being provided.

Come on now, people.

There’s no logic in running the fee off non-related services. The fact you are going to charge me 1% of my $500,000 portfolio speaks nothing to the amount of hours that will be required to help me deal with a 300% capital gain on a $50,000 position, which may involve setting up a DAF so I can send it to Afghanistan. Which means you haven’t assessed how long it would take to do this planning work, because all I am to you is a portfolio. Instead, I’m charged 1% for work you are outsourcing to a roboadvisor anyway.

Whoooooooops did I write that? Where’s the delete button, quick!

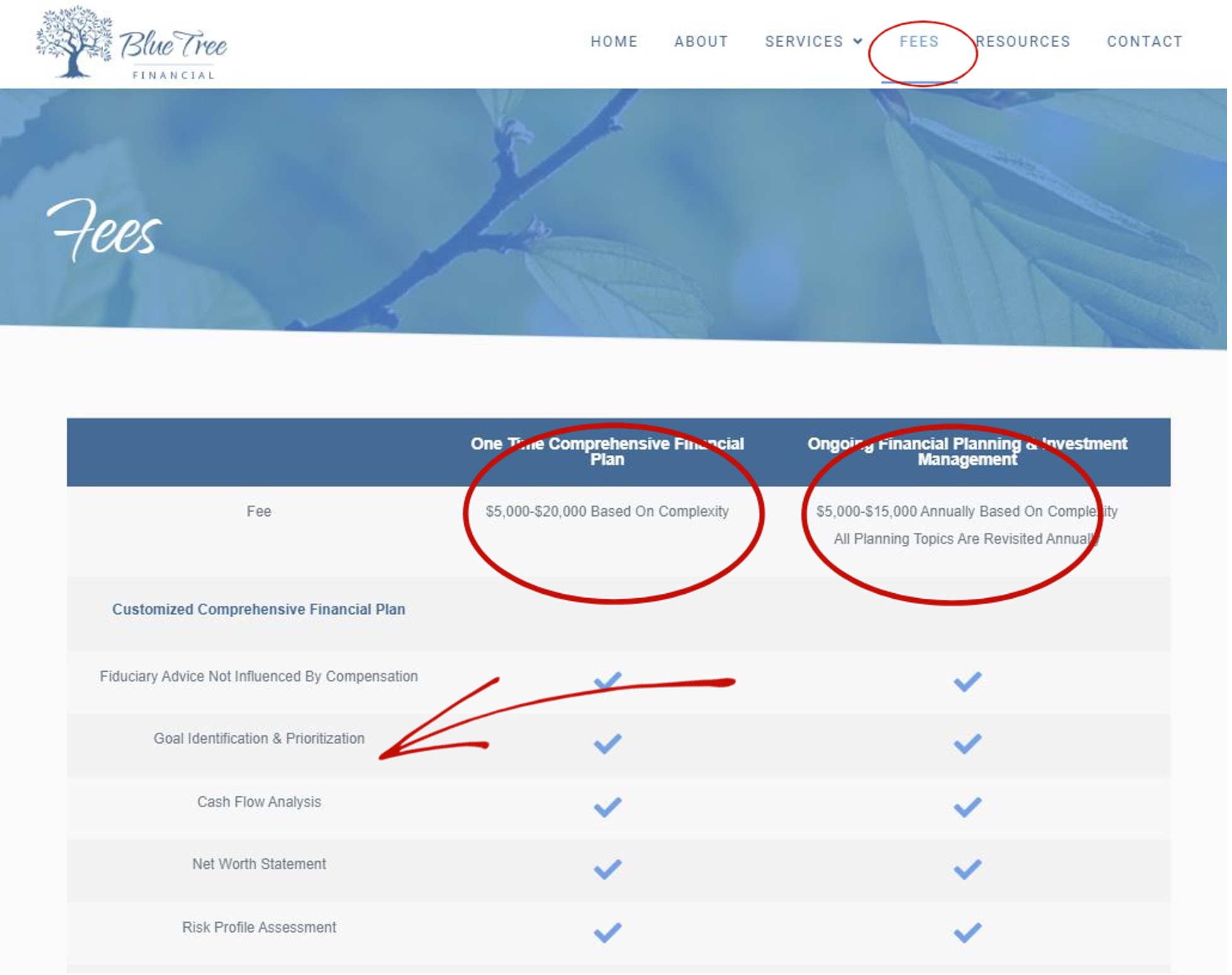

- Planning should be charged by time and resources required, not by assets.

- Fee should be disclosed clearly upfront on the website with clear detail of what the service entails.

- Invoices should be presented with detail on associated deliverables.

- Use particular care when using words such as “retainer” or “subscription” when describing your fees, because it makes you sound like you are getting paid on auto-renew for doing nothing.

- Fees should be cited as a specific dollar amount, not a wide range (which advisors call “complexity because come on, we all know that the people with higher assets generally get charged higher planning fees).

- If you are bundling financial planning fees with other services, justify the pro-rata value of the service with documented evidence. In other words, the planning should be assigned a monetary value even if it is paid for as part of a bundle.

3. Spell out the deliverables

Everyone assumes that financial planning is a report, a product rather than a process. And let’s be real; nobody likes reports. It sounds too much like “report card.” 😫

Let’s:

- Describe services using language that reflects quantifiable services and deliverables.

- Avoid vague marketing terms, e.g. “comprehensive financial plan” (my favorite) or “holistic.”

- Document the provision of these services so that they can be verified easily.

- Specify the contract period clearly; clarify if the service is ongoing planning vs a one-time financial plan.

- Record keep properly using a CRM or other software.

- Provide clients with a bulleted update on a quarterly basis of all the financial planning “touches,” the ongoing work that was done to carry out the plan.

Here are some highly transparent examples of planners who spell it out.

Clear presentation of services/deliverables:

I absolutely love the table format. Kelly Berenbaum clearly spells it out: what is delivered and with what frequency. Not too much fluff here.

Saying, “I provide financial planning” is like a doctor saying, “I provide healthcare.”

Talk about the problems that you solve, and how you solve them. Lodestar Financial Planning does a great job, they specifically write out the questions their planning services will answer.

Ongoing “touches” document:

Check out this “touches” document from Chris Randall of Axis Capital Management. This transparently keeps the client up to date with what was done and what will be done. Thanks, bro!

Or again from Lodestar Financial Planning, a month-by-month service calendar:

How’s that for a financial planning makeover?

Sara’s upshot

The age of transparency is upon us, an unprecedented movement defined by the values of clarity, modesty, logic, fairness, and advocacy for the client.

Anyone who wants to join the future of the industry, come to our meetup on December 14th – you can sign up here.

Sara Grillo, CFA, is a marketing consultant who helps investment management, financial planning, and RIA firms fight the tendency to scatter meaningless clichés on their prospects and bore them as a result. Prior to launching her own firm, she was a financial advisor.

Sources

Colorado Department of Regulatory Agencies. Division of Securities. March 2022. Ongoing Financial Planning Guide. https://drive.google.com/file/d/1uoEh8yZUPr6LovQyMQhmeW1Ufp_lgUVW/view

U.S. Securities and Exchange Commission. How to Submit Comments. https://www.sec.gov/regulatory-actions/how-to-submit-comments

Forbes Breaking News. (15 Nov, 2022). Sherrod Brown Leads Senate Banking Committee Hearing On Oversight Of Financial Regulators. YouTube. [Video]. https://www.youtube.com/watch?v=pxg_SjmsEww

Conversations with Scott Salaske, Chris Randall, Skip Fleming, Kelley Berenbaum, and Knut Rostad

Disclaimers

Nothing in this article constitutes legal or compliance advice. For legal advice specific to your situation, consult an attorney.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All