Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Don’t trust analysis from managers that shows they have outperformed an appropriately selected, passive benchmark. That is true for mutual funds, and new research shows it is equally accurate when it comes to endowments and pension funds.

My October 22, 2021, article for Advisor Perspectives, “How Mutual Funds Mislead Investors,” provided the evidence demonstrating that mutual funds routinely select benchmarks that provide them with the greatest degree of performance, even to the extent of switching benchmarks if a different one will boost their performance. Kevin Mullally and Andrea Rossi, authors of the July 2021 study, “Benchmark Backdating in Mutual Funds,” on which the article was based, analyzed whether fund sponsors took advantage of this flexibility to mislead investors. Their data sample covered actively managed funds over the 13-year period 2006-2018. Their findings led them to conclude that “the information some funds present to investors about their relative performance does not appear to be reliable.” Sadly, demonstrating their naivete, investors rewarded funds for backdating their past performance – funds that changed their benchmarks received positive abnormal flows in the next five years.

Unfortunately, mutual funds are not the only institutions that mislead investors via their choice of benchmark. Just like mutual funds, public pension plans and endowments are allowed to use benchmarks of their own choosing, typically referred to as custom or strategic benchmarks. This freedom allows them to exhibit significant benchmark bias – they do not have to choose a passive benchmark (such as an index or index fund) that best presents the exposures and risk characteristics of their actual investments. Instead, they can choose benchmarks that are more easily outperformed.

Richard Ennis, author of the October 2022 paper “Lies, Damn Lies and Performance Benchmarks: An Injunction for Trustees,” demonstrated that “most institutional investors, such as public pension funds and endowments, report their performance using biased benchmarks. The benchmarks are biased downwardly, meaning their returns tend to be less than a fair one for the market exposures and risk exhibited by the institutions’ portfolios.”

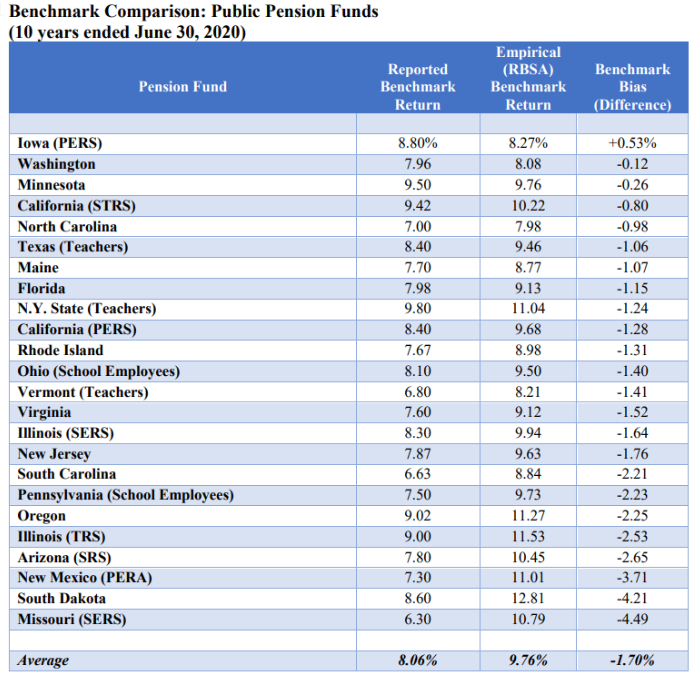

Benchmark bias of public pension plans

Using returns-based style analysis, Ennis found that while the 24 public pension plans he studied reported outperforming their custom benchmarks by an average of 0.4 percentage points per year for the decade, 19 of the 24 exhibited bias of greater than 1 percentage point, and one exhibited benchmark bias of nearly 4.5 percentage points. The average bias was 1.7 percentage points per year. This bias enabled a sizable majority to report outperforming their chosen benchmarks when, in fact, most underperformed an appropriate passive-management benchmark by a wide margin. Ennis noted: “Benchmark bias is significant and pervasive.”

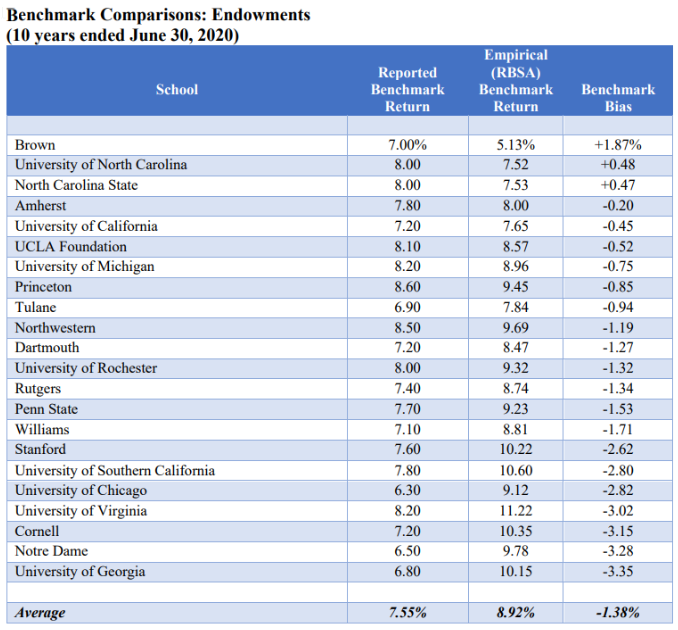

Benchmark bias of endowments

Performing the same risk-based analysis for 22 large endowments, Ennis found that, like the pension funds, they gave the false impression that they performed favorably relative to passive management when, in fact, they underperformed by significant margins.

- The 22 endowments reported outperforming their custom benchmarks by an average 0.1 percentage point per year.

- The average benchmark bias of the endowments was 1.4 percentage points.

- Only three funds did not exhibit benchmark bias.

- 13 of the 22 exhibited bias of more than 1 percentage point per year.

- One fund exhibited benchmark bias of nearly 3.4 percentage points per year.

Ennis’s findings led him to conclude: “Benchmark bias masks serious agency problems in the management of institutional funds. For example, fund staff and consultants have strong incentives to justify complex, costly multi-asset-class portfolios, for which they themselves are the benchmarkers. Trustees may feel they have no choice but to accept the benchmarking and reporting by staff and consultants, but this only perpetuates the problem.” He advised: “At the very least, investment trustees should step up and take control of benchmarking and performance reporting. For they are the ones charged with watching the watchmen.”

Investor takeaways

Gaming performance via choice of benchmarks is one of the biggest problems facing both individual investors and institutional investors. The research, including the annual S&P Indices Versus Active Scorecards (SPIVA), makes clear that active management is a loser’s game – while it is possible to win, the odds of doing so are so poor it is not prudent to try. Sadly, the SEC allows significant freedom in selecting benchmarks, and most individuals do not have sufficient knowledge to identify the problem. One would think that the more sophisticated institutions such as public pension plans and endowments would address the issue. Unfortunately, the evidence demonstrates that they are not doing so. Clearly, the trustees of the public pension plans and endowments need to do a better job of holding their employees, the funds they hire, and the consultants they engage to a higher standard. As Ennis said, “They are the ones charged with watching the watchmen.”

Larry Swedroe is the head of financial and economic research at Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. Information may be based on third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. LSR-22-408

Read more articles by Larry Swedroe

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.