A robust research literature has developed around tax planning opportunities for retirement to manage “nonlinearities” in the tax code. Those nonlinearities include the Social Security “tax torpedo,” the stacking of preferential income sources (qualified dividends, long-term capital gains) on top of ordinary income, the triggering of Medicare premium surcharges when income exceeds certain thresholds, and the net investment income tax. Another matter that has been less explored but which can have large impacts on the marginal tax rates faced by individuals who obtain health insurance coverage through the Affordable Care Act (ACA) exchanges is the reduction of the tax credits (or subsidies) for health insurance coverage as incomes increase.

A robust research literature has developed around tax planning opportunities for retirement to manage “nonlinearities” in the tax code. Those nonlinearities include the Social Security “tax torpedo,” the stacking of preferential income sources (qualified dividends, long-term capital gains) on top of ordinary income, the triggering of Medicare premium surcharges when income exceeds certain thresholds, and the net investment income tax. Another matter that has been less explored but which can have large impacts on the marginal tax rates faced by individuals who obtain health insurance coverage through the Affordable Care Act (ACA) exchanges is the reduction of the tax credits (or subsidies) for health insurance coverage as incomes increase.

Generating taxable income can lead to thousands of dollars of lost subsidies to help cover the cost of health insurance. Early retirees who are not yet eligible for Medicare (most individuals will achieve Medicare eligibility in the month they reach age 65) and who buy health insurance through healthcare.gov or the state insurance exchanges, will want to consider the impact of lost health insurance subsidies as part of their marginal tax rate on any tax planning strategies such as Roth conversions or capital gains harvesting.

I will consider the situation under the current rules extended by the Inflation Reduction Act. These rules continue enhanced subsidies through the end of 2025 that were first introduced in 2021. Unless a further extension happens, the law will revert to less generous subsidies in 2026. As part of that reversion, the “subsidy cliff” will return, as there can be a steep drop in subsidies by thousands of dollars as soon as income exceeds 400% of the federal poverty level for the household by just $1. This will create a different problem for retirees who might have an opportunity to stay below the 400% threshold. But it also means that for tax planning purposes, there is no additional marginal tax from lost subsidies once individuals are above that threshold. For early retirees who may again face the subsidy cliff before reaching Medicare eligibility, this might be an additional short-term opportunity to do more strategic tax planning before 2026. This article focuses on the system in place through 2025, which does not include that subsidy cliff.

The health insurance subsidy available is based on a percentage of income one is deemed to be able to afford for healthcare and on the premium of the benchmark health insurance plan in the county where one lives. This benchmark plan is the second-to-least expensive Silver plan available in the county, and its premium varies quite a bit across the country. The plan premium is also based on the ages and tobacco-use status of those who will be covered by the insurance. Health plans are available as Bronze, Silver, Gold, and Platinum, with premiums generally increasing and out-of-pocket costs decreasing as one progresses through the list. Policymakers wish to ensure that a Silver plan remains affordable, though individuals may choose any plan they wish.

For a case study, I consider a couple both at age 60 who do not use tobacco products. The available subsidy can be determined either by going directly to healthcare.gov and determining the premium for the second-to-lowest priced Silver plan, or by using a tool such as the Kaiser Family Foundation’s Health Insurance Marketplace Calculator that aggregates this information.

In 2023, the average premium across the United States for the benchmark plan for the 60-year-old couple is $1,937.50 per month, or $23,250 per year. The potential subsidy matches this number. General descriptions about ACA premiums may describe smaller premium numbers, but that’s because the discussion assumes much younger individuals seeking coverage. Those approaching traditional retirement ages will face higher premiums, and therefore higher potential subsidies for coverage.

The subsidy is the premium of the benchmark insurance plan less the percentage of modified adjusted gross income (MAGI) one is deemed able to pay. The ACA-specific definition of MAGI takes the AGI and adds other items back in, such as untaxed foreign earnings, tax-exempt interest, and the non-taxable portion of any Social Security benefits. The percentage of ACA MAGI one is expected to contribute is further based on the federal poverty level (FPL) in the previous year for the household seeking coverage, which in turn depends on the number of people in the household. For our two-person case study, I assumed the overall household size is also two. For coverage in 2023, the FPL in 2022 for the two-person household is $18,310 in all states but Alaska and Hawaii.

I then looked at the ratio of the AGI MAGI to the FPL. Depending on the state, households where that ratio is less than 100% or 138% will receive health insurance through Medicaid. If not eligible for Medicaid, those with incomes under 150% of the FPL can receive the full subsidy amount for their insurance coverage. In our example, 150% of the FPL is $27,465. Between 150% and 300% of the FPL (300% is $54,930), the subsidy is reduced by the expected contribution of the household which grows linearly from 0% to 6% of income in this range. Then, between 300% and 400% of the FPL (400% is $73,240), the subsidy is reduced by the expected contribution of the household that grow linearly from 6% to 8.5% of income in this range. Above 400% of the FPL, households are expected to contribute 8.5% of their income toward the cost of their health insurance, reducing the subsidy accordingly. With a high cost for the benchmark plan, this can extend the income levels for which subsidies are available to rather high levels.

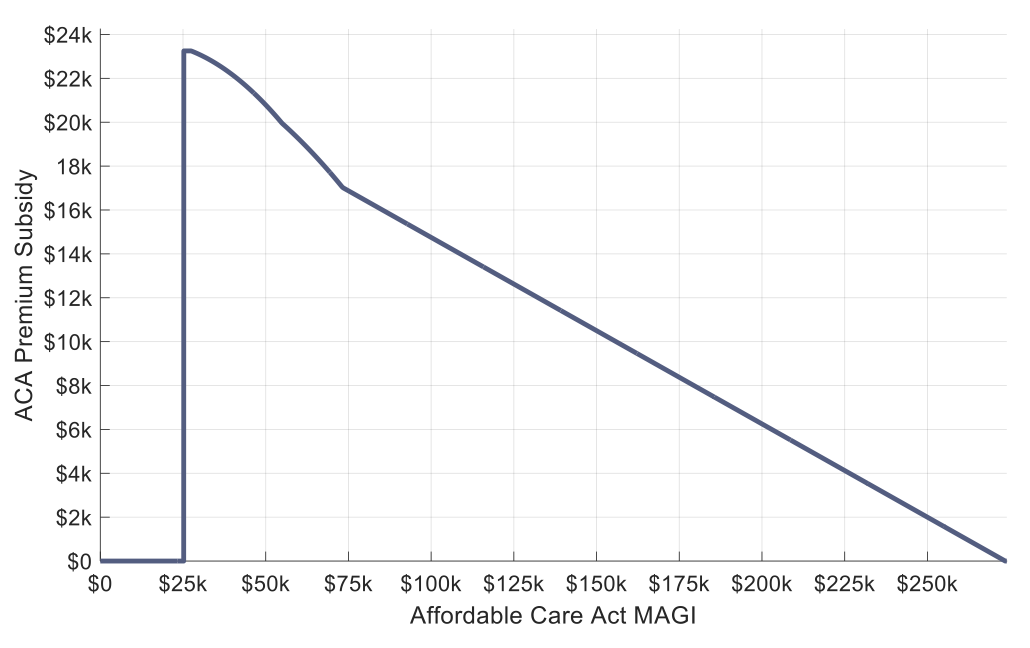

Exhibit 1 illustrates this information for the case of the 60-year couple assuming they live in a county where the cost of the benchmark plan happens to match the US national average of $1,937.50 per month or $23,250 per year. Looking closely, I’ve assumed this is a state where Medicaid-coverage ends and subsidies begin at 138% of the FPL. The annual subsidy jumps to $23,250 here and stays flat until income reaches 150% of the FPL. It then gradually declines, with kinks at both the 300% and 400% of FPL levels. Subsidies continue until the ACA MAGI reaches $273,529. If one looks closely, the reductions are not linear between 150% and 400%, as the subsidy reduction accelerates when more income leads to more subsidy dollars being lost in absolute terms as the percentage of income one is expected to contribute grows.

Exhibit 1

Annual ACA Premium Subsidies for 60-Year-Old Couple with Average Benchmark Plan Premium

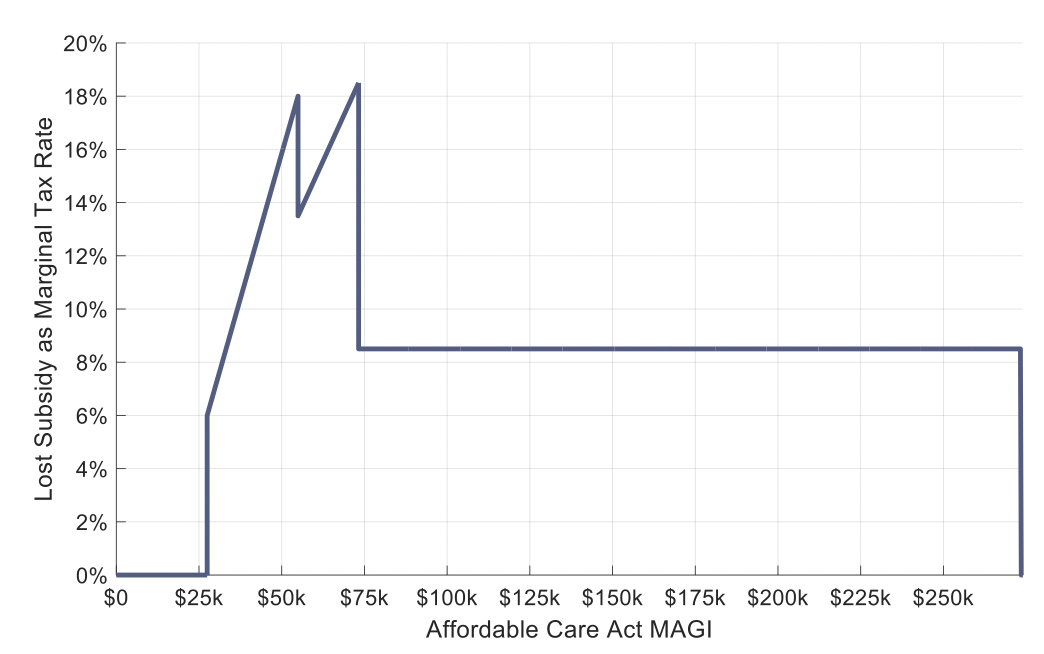

This point can be seen more clearly in Exhibit 2, which shows the “marginal tax rate” of additional income solely in terms of its impact on subsidy reductions. Often these types of nonlinearities in the tax code receive cute names like the Social Security “tax torpedo,” and I would call this the “Batman tax” as based on the shape of the marginal tax rates. The subsidy is maximized and then subsidy losses begin at 150% of the FPL ($27,465). The marginal tax rate here is 6% (i.e., $1 of income will reduce the health care subsidy by 6 cents). This marginal tax rate accelerates until reaching 18% at 300% of the FPL ($54,930). Then the rate of expected contribution slows, kicking the marginal tax rate down to a bit under 14%. At this 300% level we begin a phase in which the expected contribution increases by 2.5% per 100% increase in the FPL, instead of by 4% per 100% increase in the FPL. But by 400% of the FPL ($73,240), these higher income levels to which the growing percentages are applied cause the marginal tax rate to reach its highest level of 18.5%. In this case, $1 of income is reducing the subsidy by 18.5 cents. Beyond 400% of the FPL the marginal tax rate remains at 8.5% until eventually falling to 0% when incomes reach the level that the subsidy is no longer available.

Exhibit 2

Implied Marginal Tax Rates from Lost ACA Premium Subsidies for 60-Year Old Couple with Average Benchmark Plan Premium

For the period through 2025, there is no income cap on the subsidy, as instead the provision is that no one is required to pay more than 8.5% of their ACA MAGI for the benchmark plan. Therefore, the higher the cost of the benchmark plan, the higher the income can be before the subsidy ends. I do not know which county in the US experiences the highest costs, but I think of Greenwich, CT as a posh place and so tried it for an example. The benchmark plan for this couple is $34,391 per year, which means that subsidies are available for incomes up to $404,600. As an aside, once individuals reach age 63, they need to consider the impacts of income on Medicare premiums for two years later. A married couple filing jointly at this $404,600 income level will also find that their Medicare premiums will be more than $5,000 greater per person in two years, creating another marginal tax on top of the lost 8.5% of subsidy per dollar of income. Those aged 63 and 64 who get health insurance through the ACA are hit by a double whammy as their incomes impact both the cost of current year health insurance as well as the Medicare premiums they will pay in two years!

Planning implications

Losing subsidies for health insurance coverage is another nonlinearity in the tax code that can impact tax planning decisions related to generating taxable income when the tax impact is the lowest. When relevant, these health insurance subsidies are another factor to include into the tax planning conversation around generating additional taxable income through Roth conversions or realizing capital gains.

For those impacted by the lost subsidies, and especially if the 400% of FPL subsidy cliff returns in 2026, it may be possible to reduce the ACA MAGI with tax-deductible contributions to employer plans, IRAs, or HSAs. Only above-the-line deductions like this will help.

Also, advisors often advocate delaying Social Security benefits. For those who obtain health coverage through the Affordable Care Act, this may provide an additional strong incentive to delay Social Security benefits. As the ACA MAGI adds in 100% of the benefits received to its calculation, an additional downside to claiming early could be a significant reduction to the eligible premium subsidy.

The bottom line

HealthInsurance.org crunched the numbers from the 2022 open enrollment period to determine that in early 2022 there were 14.5 million people enrolled in ACA plans, and that 89% of them were receiving some level of premium subsidies. Because premiums and, therefore, subsidies, increase with age, this is an important consideration in the tax planning conversation for clients. This article has quantified how these subsidies work, and how the “marginal tax rate” on lost subsidies is as high as 18.5%. The marginal tax rate is also 8.5% on income in excess of 400% of the FPL, and when the cost of the benchmark plan is high, the marginal tax of lost subsidies can continue to apply at high income levels, potentially impacting the tax planning decisions that clients make.

Wade D. Pfau, Ph.D., CFA, RICP®, is the program director of the Retirement Income Certified Professional® designation and a Professor of Retirement Income at The American College of Financial Services in King of Prussia, PA, as well as a co-director of the college’s Center for Retirement Income. As well, he is a Principal and Director for McLean Asset Management and RISA, LLC. He also serves as a Research Fellow with the Alliance for Lifetime Income and Retirement Income Institute. Wade’s latest book is Retirement Planning Guidebook: Navigating the Important Decisions for Retirement Success.

A robust research literature has developed around tax planning opportunities for retirement to manage “nonlinearities” in the tax code. Those nonlinearities include the Social Security “tax torpedo,” the stacking of preferential income sources (qualified dividends, long-term capital gains) on top of ordinary income, the triggering of Medicare premium surcharges when income exceeds certain thresholds, and the net investment income tax. Another matter that has been less explored but which can have large impacts on the marginal tax rates faced by individuals who obtain health insurance coverage through the Affordable Care Act (ACA) exchanges is the reduction of the tax credits (or subsidies) for health insurance coverage as incomes increase.

A robust research literature has developed around tax planning opportunities for retirement to manage “nonlinearities” in the tax code. Those nonlinearities include the Social Security “tax torpedo,” the stacking of preferential income sources (qualified dividends, long-term capital gains) on top of ordinary income, the triggering of Medicare premium surcharges when income exceeds certain thresholds, and the net investment income tax. Another matter that has been less explored but which can have large impacts on the marginal tax rates faced by individuals who obtain health insurance coverage through the Affordable Care Act (ACA) exchanges is the reduction of the tax credits (or subsidies) for health insurance coverage as incomes increase.