Guaranteed Lifetime Income Isn’t Free

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Insurance protects against losses – fires, floods or a wrecked car. A client buys insurance to avoid the life-altering consequence of a random loss. In this article, we clarify the costs and the expected payouts from lifetime income insurance through a guaranteed lifetime withdrawal benefit (GLWB). Offering these payouts to retirees who experience low investment returns and a long life isn’t free, although the cost of insurance is often mischaracterized as a fee.

Lifetime income insurance preserves a retiree’s ability to spend a minimum amount each year from a risky investment portfolio. The insurance premium is often characterized as a fee, but the guarantee of lifetime income provides valuable protection to retirees who face the risks of longevity and low portfolio returns. The premium is a transfer from lucky to unlucky retirees and, like any other form of insurance, can improve outcomes for risk-averse retirees.

Imagine a client has saved $500,000 to fund spending in retirement. You tell her she can safely spend about $25,000 each year. She wants to know how confident you are that she won’t run out. You reply that you’re very confident – Monte Carlo simulations show that she has more than a 90% chance of success.

What if the client asked you to instead guarantee that no matter how long she lived, no matter what happened in the markets, she could continue to receive $25,000 each year from a $500,000 portfolio?

You’d hesitate.

You understand that some clients will live a long time – a healthy 65-year-old woman has a 9% chance of living to 100 according to Society of Actuaries annuity mortality tables (which are appropriate for people with enough money to use an advisor). A 20% drop in a diversified portfolio the first year would reduce the client’s savings from $500,000 to $400,000, minus the first-year $25,000 withdrawal.

How confident are you that a 66-year-old healthy woman can withdraw $25,000 each year from a $375,000 portfolio if she lives to age 95? Are you still willing to guarantee that income?

No advisor would agree to bear this risk – at least not without some added compensation to fund the less-fortunate clients who run out of savings. How much would you (or your parent firm) charge a client to offer this guarantee? In a group of 1,000 retirees, how many will deplete a $500,000 portfolio while they are still alive if $25,000 is withdrawn each year?

Lifetime income insurance on a risky portfolio allows a retiree to transfer longevity risk to an insurer, as well as the risk that investments will significantly underperform expectations. A poor sequence-of-investment return forces a retiree to either accept a greater possibility that she will run out later in life, or that she will need to spend less than she’d hoped. A lifetime income guarantee allows a retiree to spend freely up to the guaranteed spending amount without fear that circumstances beyond her control will force her to cut back.

Will a client pay for this guarantee? Some retirees will accept the risk of having to cut back. Others won’t. Those who would buy income insurance are willing to accept less expected wealth to protect against an extreme negative lifestyle outcome. This is the essence of insurance. It is not supposed to be wealth maximizing on average, nor should an advisor want an insurer to promise more in claims than they expect to collect in premiums.

In other words, insurance isn’t free. It’s surprisingly common to see fee-compensated advisors compare the cost of managing an unprotected investment portfolio to the cost of a portfolio that includes lifetime income insurance. This comparison is wrong if these advisors are not willing to accept responsibility for insuring a minimum lifetime income.

One reason that lifetime income guarantees are dismissed is that it isn’t easy to imagine what an insurance claim looks like. In this analysis, we simulate variable investment returns and random lifespans to illustrate the cost to an insurer of lifetime income protection and how much an insurer will collect in premiums over time.

Understanding the cost of lifetime income insurance

Insurance claims on a lifetime-income guarantee are paid when the retiree’s investment balance runs out. The insurer then continues to make income payments for the life of the retiree out of its own general account rather than from the retiree’s savings. This GLWB represents a lifetime liability to an insurer when an investors account balance falls to zero.

Many retirees will not require a claim because they won’t outlive their savings. A $25,000 annual income can be easily withdrawn from a $500,000 investment portfolio because investments either perform well or because retirement doesn’t last that long. Some of those retirees could have funded their $25,000 income goal for far less than $500,000. The retirees who do not run out of savings subsidize those that do.

The initial $500,000 investment will not be enough to fund the $25,000 income goal for a few retirees who are lucky to live a long life. They may need $600,000, $700,000, or more to withdraw the guaranteed minimum income that would have been provided by a GLWB over their lifespan.

In the following analysis, we assume a contract-value insurance premium of 1.5% and step-ups in the income base. The premium is levied on the liquidation value of the policy, which will fall over time as income and insurance premiums are withdrawn.

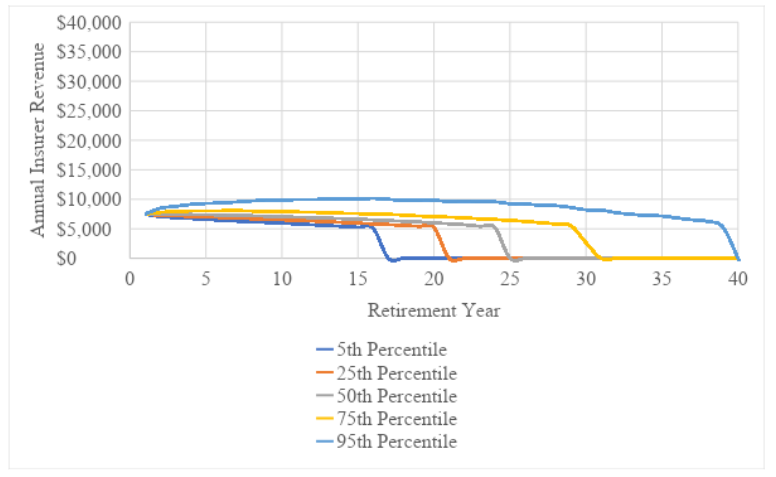

The figure below shows the insurance premiums generated from the GLWB policy by year of retirement at various distributions in simulated retirements. Fortunate retirees at the 5th percentile will only pay the insurance premiums for about 15 years before depleting their contract value and relying on the insurer to continue making income payment. The median retiree will make premium payments for about 25 years, which is roughly the median longevity.

Annual Insurance Premiums Collected on a GLWB Policy

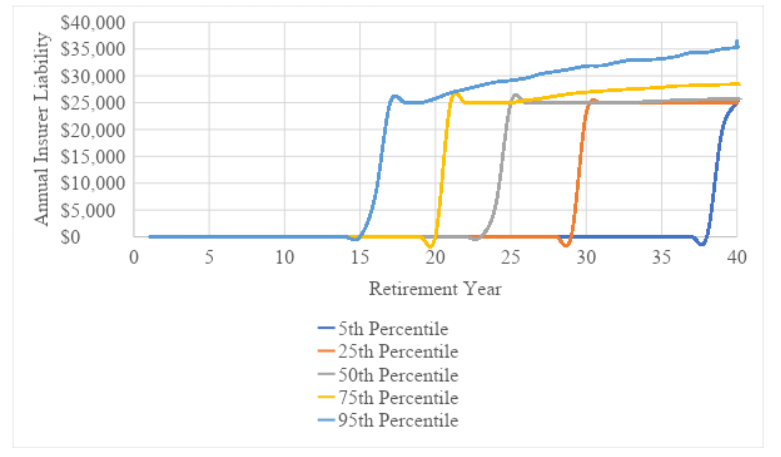

Premiums that are collected by the insurer are then used to pay retirement income claims when the retiree’s investment account falls to zero. The value of those income claims is shown in next figure. In the simulations, when the cost of producing the same amount of income as a variable annuity exceeds $500,000, the insurance company subsidizes the retiree’s income. This subsidy represents the return of a portion of the cost of providing lifetime income through the GLWB rider.

Premiums that are collected by the insurer are then used to pay retirement income claims when the retiree’s investment account falls to zero. The value of those income claims is shown in next figure. In the simulations, when the cost of producing the same amount of income as a variable annuity exceeds $500,000, the insurance company subsidizes the retiree’s income. This subsidy represents the return of a portion of the cost of providing lifetime income through the GLWB rider.

The distribution of claim amounts among hypothetical retirees is going to vary depending on realized longevity. The insurer will pay significant income claims to retirees at the 5th percentile of outcomes upon depletion of their contract value after 15 years. At the 25th percentile (75th percentile of claims), the insurance company will need to withdraw money from reserves to pay claims after just 20 years. At the median longevity, the insurance company will have just begun to make income payments and more fortunate retirees will not receive insurance claims until late in retirement when they have only a small probability of still being alive.

Income Paid by Insurer from GLWB Guarantee to Retiree

These examples illustrate how GLWBs allow retirees to transfer the risk of a poor sequence-of-investment returns and a long life to an insurance company. Insurers collect far less in premiums from retirees who experience lower investment returns than they pay out in the form of claims. Fortunate retirees pay the premium for the peace of mind of knowing that they can continue to spend a guaranteed minimum amount in retirement.

The subsidy from those who experience higher investment returns to those retirees with lower investment return is comparable to any other form of insurance. Risk sharing allows all retirees to live their desired lifestyle free of the ever-present possibility that the cost of funding an income goal will be far higher than they had expected.

Our analysis also illustrates the flaw in comparing variable annuity outcomes to unprotected investment outcomes at the expected longevity. Investors with enough wealth to buy a lifetime income will live significantly longer than the average American. The median longevity of a healthy 65-year-old woman is about 25 years (to age 90). The terminal wealth of this average woman will be reduced by the cost of the insurance premium if she lives to the average longevity – her investment IRR will be lower than for an unprotected retiree.

After reaching her average longevity, the value of insurance claims will rise, and longer-lived women will receive an IRR on investments that is higher than an unprotected retiree. Lifetime income insurance shifts portfolio return from those with a cheaper retirement (short and/or high investment returns) to those with an expensive retirement (long and/or low investment returns).

Is the cost of insurance fair? Milevsky and Salisbury estimated that the cost of providing the lifetime income guarantee is between 0.7% and 1.6% depending on assumptions about time horizons and investments volatility (the insurer also assumes the risk that volatility will rise in the future). This means lifetime income insurance costs less (based on compensation to the insurer for the cost of doing business) than similar financial insurance products such as long-term care insurance. When priced fairly, the decision to insure should be based on the risk preferences and the financial circumstances of the client (i.e., are they at risk of not meeting a lifestyle goal if markets tank?).

Conclusion

When most advisors think about lifetime-income insurance, they imagine commission-compensated variable annuity products sold by insurance agents with high surrender charges and expensive investment options.

However, annuities exist that allow an AUM-based advisor to draw an annual fee instead of a front-loaded commission. There are also VAs with low-cost investment options, and one can buy lifetime income insurance as an add-on to an investment portfolio managed by a financial advisor (a contingent-deferred annuity).

Like mutual funds, the GLWB category shouldn’t be dismissed because of a few uncompetitive products or distasteful sales practices. And, like mutual funds, commission compensation can be cheaper for long-term investors who don’t need ongoing services. Retirees may even prefer high surrender charges if they allow the insurer to offer a more generous lifetime income guarantee (like mutual fund redemption fees).

Financial advisors should view lifetime-income insurance like any form of insurance that protects against a loss. Cutting back on lifestyle to avoid running out of money is every bit as significant a loss as wrecking a car or experiencing a flood. In many cases, particularly for risk-averse retirees and the mass affluent whose resources are limited, buying lifetime income insurance allows them to live better by spending freely early in retirement even if markets are falling. Like any form of insurance, the decision to trade expected wealth for peace of mind can be in a client’s best interest.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an Adjunct Professor of Wealth Management at The American College of Financial Services and a Research Fellow for the Retirement Income Institute.

Michael Finke, PhD, CFP®, is a professor of wealth management, WMCP® program director, and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All