Technology has made it possible for us to walk on the moon once again, yet academic research has failed to find a way to identify outperforming mutual funds. But a new study shows that may be possible.

Technology has made it possible for us to walk on the moon once again, yet academic research has failed to find a way to identify outperforming mutual funds. But a new study shows that may be possible.

An overwhelming body of academic research demonstrates that the past performance of actively managed mutual funds does not provide useful information as to future risk-adjusted performance, and (as the annual SPIVA Persistence Scorecards regularly report) there is less persistence of outperformance than randomly expected. Thus, while active management underperforms in aggregate, and the majority of active funds underperform every year (the percentage that underperform increases with the time horizon studied), if an investor were able to identify the few future winners by utilizing some metric, active management could be the winning strategy.

Given the potential rewards, it’s not surprising that numerous attempts have been made to find that holy grail – the metric that will identify future outperformers. Believers in active management were offered hope with the 2009 study by Martijn Cremers and Antti Petajisto, “How Active Is Your Fund Manager: A New Measure That Predicts Performance.” The authors concluded: “Active share (a measure of how much a fund’s holdings deviate from its benchmark index) predicts fund performance: funds with the highest active share significantly outperform their benchmarks, both before and after expenses, and they exhibit strong performance persistence.” Unfortunately, later research, including the 2016 studies “Deactivating Active Share” and “Estimating Time-Varying Factor Exposures,” the 2017 study “Defining Activeness: Active Share, Risk Share & Factor Share,” the 2021 study “Is Active Share Unattractive?,” and the 2022 studies “Fund Concentration: A Magnifier of Manager Skill” and “Active Share and the Predictability of the Performance of Separate Accounts,” all demonstrated that it is extremely difficult to make the case that active share – either as a standalone metric or in combination with other metrics such as past performance – has any predictive value in terms of future risk-adjusted outperformance of actively managed mutual funds.

The search goes on.

Risk-adjusted performance

Academic studies of actively managed mutual funds tend to focus on risk-adjusted performance, not on risk alone. When risk is directly considered, it is typically measured as volatility or beta (a measure of risk/volatility relative to the risk of the overall market). However, volatility is not the only measure of risk used by practitioners. Another frequently used metric, maximum drawdown (a measure of the largest decline in a fund’s value from peak to trough), which focuses on downside risk, is simple to understand and is reported by Morningstar as part of their risk analysis.

New research

Timothy Riley and Qing Yan contribute to the literature on the predictability of mutual fund performance with their June 2022 study, “Maximum Drawdown as Predictor of Mutual Fund Performance and Flows,” in which they examined whether maximum drawdown (MDD) contains useful information for investors – does it provide information on future fund performance? Their main benchmark for risk-adjusted performance was the Carhart four-factor model (beta, size, value and momentum). Their data sample was from the CRSP Survivor-Bias-Free U.S. Mutual Fund Database of actively managed funds and covered the period 1999-2019. They used daily returns to determine MDD.

Since a significant part of a drawdown is determined by a fund’s style rather than a fund manager’s skill, to remove the style component, they subtracted from each individual unadjusted value the mean unadjusted value across all funds with the same style during the same time period. They then used this style-adjusted maximum drawdown for their MDD. When considering past performance, they used the previous 24 months. Portfolios were rebalanced monthly. Following is a summary of their findings:

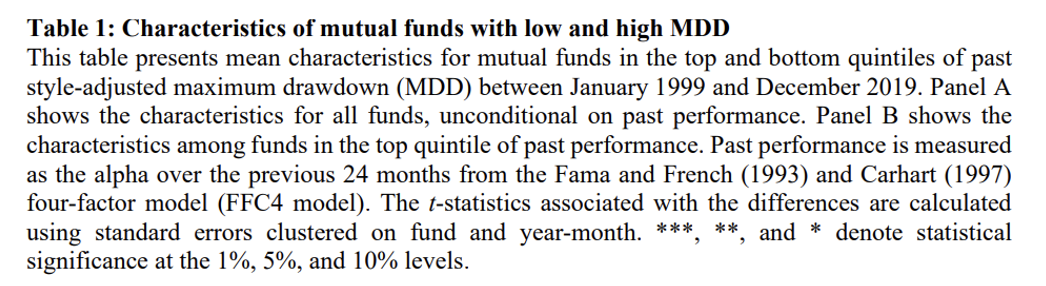

- Low MDD funds, on average, had higher returns, higher alphas, lower volatilities, lower turnover and lower expense ratios.

- MDD was persistent – a portfolio formed using funds in the lowest past MDD quintile had a subsequent average maximum drawdown of 14.6% versus 20.3% for the portfolio formed using the funds in the highest past MDD quintile. In addition, all else equal, a 10% increase in past MDD was associated with a 3.8% increase (t-stat = 6.64) in future MDD.

- Low MDD funds significantly outperformed high MDD funds regardless of past performance.

- Using 12-month periods, an equal-weighted portfolio of funds in the lowest quintile of past MDD outperformed an equal-weighted portfolio of funds in the highest quintile of past MDD by 4.00% per year (t-stat = 3.05, significant at the 1% confidence level).

- While top quintile performers continued to outperform bottom quintile performers by 1.33% per year (t-stat = 1.71), past performance even among the top quintile performers showed no evidence of future positive alphas. However, an equal-weighted portfolio of funds in the lowest quintile of past MDD among those in the highest quintile of past performance had a positive alpha of 2.40% per year (t-stat = 2.87).

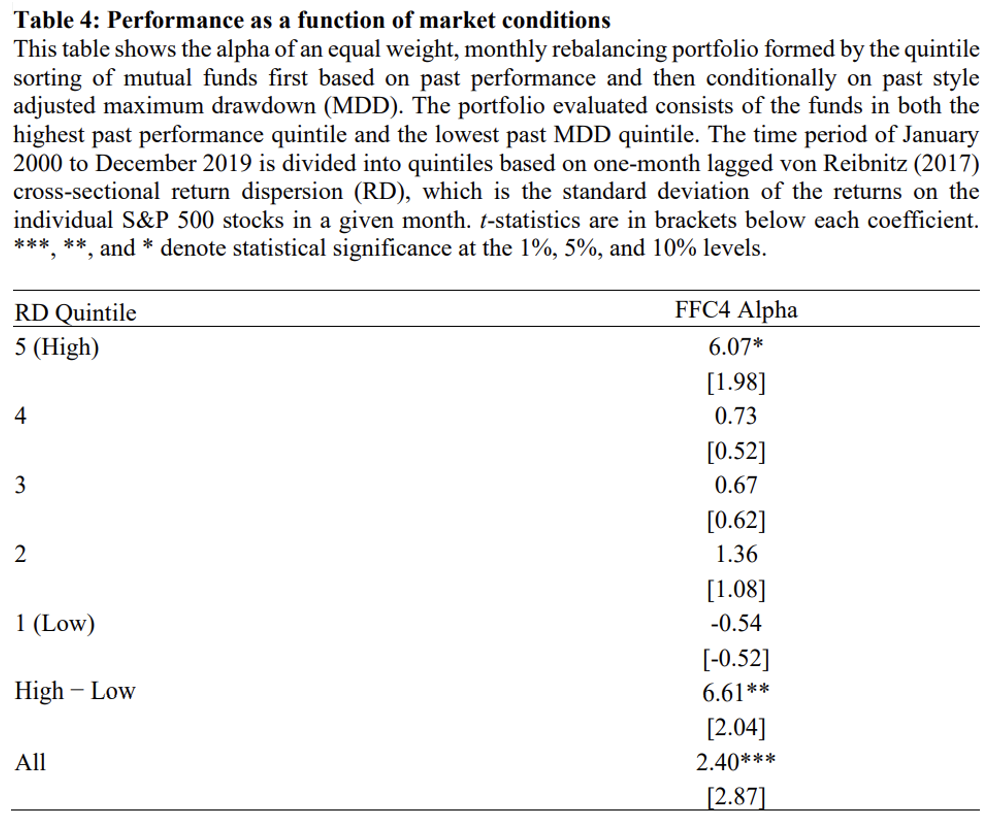

- When the cross-sectional dispersion of returns was high (there is an increased opportunity to generate alpha), an equal-weighted portfolio of funds in the lowest quintile of past MDD among those in the highest quintile of past performance had an alpha of 6.07% per year (t-stat = 1.98). In all other time periods, the alpha of that same portfolio was statistically indistinguishable from zero – manager skill was most valuable when most needed, during turbulent markets, though in all other periods skill could not be observed.

- Managers with low MDD tended to select stocks better than managers with high MDD but showed no difference in market timing – the skill of low MDD fund managers was driven by those managers’ ability to select individual stocks rather than their ability to time the overall market.

- Defining drawdown gap as the difference between the realized maximum drawdown and the hypothetical maximum drawdown based on observed holdings, there was a significant positive relation between drawdown gap and actual subsequent fund MDD – fund managers with a past record of making successful drawdown-reducing trades tended to have lower MDD in the future.

- While downside beta also predicted future fund performance, MDD provided unique information.

- The results from alternative rebalancing frequencies were similar to those using monthly rebalancing, although they did weaken with less-frequent rebalancing.

- Unsurprisingly, on average, there was a strong negative relation between MDD and net investor flows: a 10% increase in MDD was associated with an annualized net outflow of 4.7% (t-stat = -6.73).

Their findings led Riley and Yan to conclude: “We find that a fund’s past maximum drawdown has unique predictive power with respect to subsequent performance and that investors give considerable weight to a fund’s past maximum drawdown when allocating capital.”

Before drawing your own conclusions, there are a few issues to consider. In order to minimize the risks of data mining, in “Your Complete Guide to Factor-Based Investing,” Andrew Berkin and I laid out the requirements that should be met before investing based on a factor. Among the criteria is that the findings should be robust to various definitions. For example, the value factor has provided a premium whether using price-to-book, price-to-earnings, price-to-cash flow and various other metrics, and momentum has provided a premium across various formation and holding periods. In the case of MDD, Riley and Yan reported in an internet appendix the sensitivity of the results to different MDD time horizons. In tests of robustness, they found that the results were stronger using six-month MDD and weaker using 18-month MDD. They also noted that Morningstar’s website provides MDD for three, five and 10 years, and extending the horizon to three, five or 10 years further weakened the results. For example, at three- and five-year horizons, the low MDD, high prior alpha funds did not generate statistically significant alphas (0.54 with t-stat = 0.84, and 0.63 with t-stat = 1.13, respectively), and at the 10-year horizon the alpha was -0.81, though it was not statistically significant (t-stat = -1.27).

Another issue relates to the use of the Carhart four-factor model and as a test of robustness the seven-factor model of Martijn Cremers, Antti Petajisto and Eric Zitzewitz (authors of the 2013 study “Should Benchmark Indices Have Alpha? Revisiting Performance Evaluation”) rather than the Fama-French five- (beta, size, value, investment and profitability) or six-factor (adding momentum) models or the q4- (beta, size, investment and profitability) or q5-factor (adding expected growth) models that incorporate the newer factors of investment and profitability. I asked Riley about that, and he graciously responded that my query led them to test using the Fama and French profitability and investment factors. They found that the alpha of the high performance, low MDD portfolio was 1.36% per year (t-stat = 1.68) and that there was a large loading on the profitability factor (0.17 coefficient, t-stat = 4.98). That’s a decrease in alpha of about 1 percentage point per year from what they reported, a meaningful decrease driven by accounting for profitability exposure. While accounting for additional factors does decrease the alpha, it was still economically large, if not quite statistically significant. And alphas somewhat understate the benefits because they ignore the costs of passive equivalents.

I also asked about the use of two-year horizons for their measure of past performance, which seemed quite short. Riley responded: “In our primary results, we sorted on relatively short run performance (just two years). In terms of predictive power, there’s a trade-off between recency and length, and I’ve consistently found that the trade-off is best balanced by shorter run performance than I would have initially guessed. Five years seems like a good balance, but in practice, one or two years is consistently more predictive (especially if daily returns are available). A possible explanation for that balancing point could come from the Berk and Green (2004) model operating, but not operating instantaneously. If information about skill is slowly ‘priced in’ to funds, then what happened three years ago may be useless for predicting, but what happened six months ago may not be.”

Investor takeaways

Riley and Yan confirmed that past performance as a standalone metric does not have predictive value for mutual fund performance. However, their evidence does provide hope that they may have identified a metric that can identify future mutual fund outperformers. Caution is warranted, as previous findings of predictability (e.g., active share) have not held up out of sample. Those findings may have been the results of data-mining exercises that come with the degree of freedom researchers have in their search for that holy grail of predictability of performance. There is some good news for investors who would consider using their adjusted-MDD measure – low MDD funds do tend to have lower expense ratios and lower turnover, lowering the hurdles to outperform.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data which may become outdated or otherwise superseded without notice. Thid party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. LSR-22-351

Read more articles by Larry Swedroe

Technology has made it possible for us to walk on the moon once again, yet academic research has failed to find a way to identify outperforming mutual funds. But a new study shows that may be possible.

Technology has made it possible for us to walk on the moon once again, yet academic research has failed to find a way to identify outperforming mutual funds. But a new study shows that may be possible.