Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is the second part of my two-part series, “Guaranteed Income for Life,” in which I examine the benefits of the contingent deferred annuity (CDA), and whether it’s poised to become the next big thing in retirement. In Part 1, “Can Contingent Deferred Annuities Become a $100 Billion Industry?”, I contrasted the need for lifetime income with the hesitance many Americans feel when confronted with the decision of whether to buy one. I also described a solution proposed by Dr. Moshe Milevsky… a solution that sounds a lot like a CDA.

A CDA is structured such that the annuity guaranty of income for life, underwritten by a life insurance company, is held separately from the underlying investments. The CDA is conceptually a combination of product and process, in that the benefits it offers go into effect when the depletion of the covered portfolio occurs while the insured(s) remain alive.

The CDA, rather than starting income immediately or on a preset future date, begins to pay out at an unknown future date, contingent upon the value of the portfolio being fully withdrawn. This is the point at which the insurer begins paying regular income to the purchaser of the guarantee from the insurer’s account rather than from the client’s account. As Milevsky artfully put it, the “life annuity begins when your portfolio dies.”1

Milevsky instructs us that how long an uninsured retirement portfolio (one that is being used to support systematic withdrawals) lasts for any individual retiree will be a function of net investment returns, along with portfolio withdrawal rates. From there, how long a given retiree needs for that portfolio to last is a function of that individual’s realized longevity. Longevity expectations are predictable on average across a large population, which is relevant for insurer product pricing, but longevity risk is idiosyncratic for individuals on their own. An individual can hedge their idiosyncratic longevity risk (as well as systematic risk) by purchasing a single-premium immediate annuity (SPIA) with part of their portfolio, and an insurer can pool the idiosyncratic longevity risk associated with each individual contract into systematic risk across a population of insureds with overall predictable longevity – but in a low-rate environment especially, purchasing this protection can be expensive and unappealing to some investors.

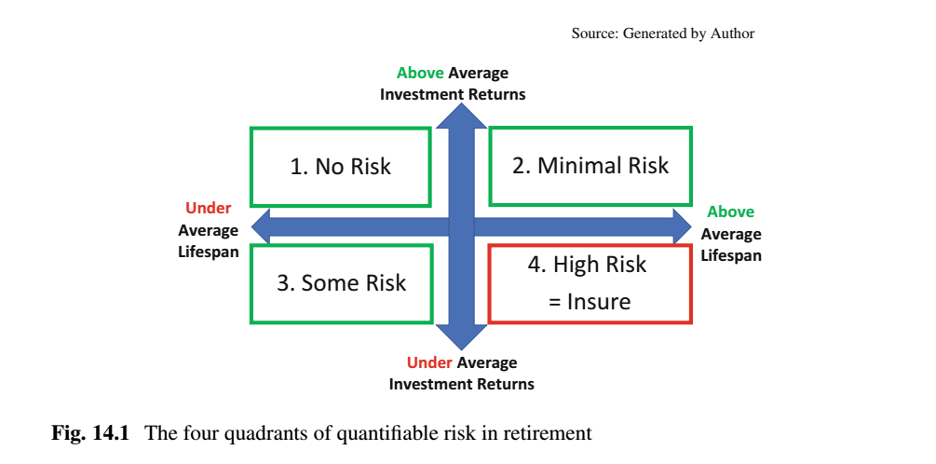

A CDA is a far more efficient way, in terms of committed capital, than SPIAs of insuring against the risk of outliving a portfolio. SPIAs pay out in all quadrants of the diagram below (and most beneficially to purchasers who live to meet the eastern end of the diagram). But for the issuer pricing the CDA, the number of circumstances in which the product pays off is limited to only those scenarios that fall in the southeast quadrant of the diagram below. Another way of saying this is: Relative to the cost of a SPIA, it is much less expensive to buy an option to receive lifetime income upon portfolio depletion when the retiree lives longer than the portfolio, because this outcome does not occur in the majority of scenarios; it occurs only when both the portfolio performs worse than expected and the retiree lives longer than average.2

Mortality-contingent products like SPIAs and CDAs are most valuable to those retirees with either a high subjective survival probability – meaning, people who expect to live longer than the average person of the same age and gender (due to biological, geographic, financial, and other factors that materially impact life expectancy), and/or high aversion to the risk of running out of retirement income. Insurers that issue longevity-protection products know that their purchasers are often healthier than the population average. They price their products accordingly (meaning, they assume purchasers will live longer than average, so they price their products at a higher price point, expecting to be making income payments past the average population expectation). Prices set with the expectation of high purchaser longevity lead to more expensive products, which leads to a smaller and smaller proportion of retirees who can expect to earn a positive IRR on the product purchase, and thus begets a recursive problem in pricing the average consumer out of the market for longevity guarantees.

With CDAs, however, as opposed to SPIAs, the consumer’s up-front commitment is modest – an annual fee that will be similar in magnitude to an advisory fee. This low commitment allows the client to make not a one-time but rather ongoing decisions to continue paying for an income guarantee, or to terminate the guarantee if it no longer proves valuable to them.

CDAs allow the client to retain control of the allocation of their assets, including equity exposure, and allows them to avoid the higher fees often associated with deferred-income annuities (DIAs) with secondary guarantees. Because the up-front capital commitment of a CDA is so much less than for a SPIA, the purchaser’s perceived subjective survival probability does not need to be much greater than average to pay off or allow for their exit from the product and process. This in turn allows the insurer to offer more affordable pricing to protect against ruin risk. This relative affordability for CDA as compared to SPIAs is particularly pronounced in the current low-rate environment.

A CDA results in insurer payouts when (1) portfolio outcomes underperform the insurer’s expectations at the same time as (2) the insured lives longer than average. It can be viewed as providing higher utility per premium dollar spent than does a SPIA. Whereas SPIAs pay out at their promised rate and schedule3 irrespective of interest rate movements since contract purchase or of the market performance in an investor’s retirement portfolio, (meaning, SPIA purchasers will receive the SPIA’s income without regard for how their other retirement investments have performed), a CDA constitutes a lean form of protection that makes payments only in those economic states in which the purchaser’s experience of income utility is highest (which is when the portfolio needed to cover retirement expenses has been depleted).

At the time of his writing, Milevsky noted that RCLA/CDA was not yet available for retail purchase, but that if it were – or perhaps better said as, once it is made available for purchase – he predicted RCLA had the potential to grow to a $100 billion industry.

And in the past year, Midland National Life Insurance Company partnered with RetireOne to bring a commission-free advisory CDA to market called “Constance.” It appears others will follow suit. With such a sizeable sales number hinted at by Milevsky, one imagines this product’s ultimate adoption to be a fait accompli that becomes more a question of when, not if, it gains material traction in the market.

That time is now.

Michelle Richter is a principal at Fiduciary Insurance Services, LLC, and executive director of the Institutional Retirement Income Council, Inc.

1Moshe Arye Milevsky. Retirement Income Recipes in R: From Ruin Probabilities to Intelligent Drawdowns (Use R!) (p. 287). Springer International Publishing. Kindle Edition.

2Image source: Moshe Arye Milevsky. Retirement Income Recipes in R: From Ruin Probabilities to Intelligent Drawdowns.

3Subject to the claims paying ability of the insurer

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.