Equities Trade Dirty Causing Investors to Lose Billions (Part 1)

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Investors – your clients – are paying unnecessary taxes when they purchase stocks, equity mutual funds and other securities.

The accounting treatment used for dividends and capital gains (“distributions”) overvalues income-producing equities by an amount equal to the security's accrued, but unpaid, distributions. This causes investors to pay tens of billions of dollars in taxes they do not owe. This problem is a known risk financial services firms and auditors recognize and is referred to as "buying a dividend."

We all know about “dirty pricing” in the bond markets. When we buy individual bonds offered on the secondary market (OTC) we are quoted two prices: the price of the bond (the “clean price”) and the accrued interest due to the seller of the bond since the previous coupon date. The two prices together are referred to as the “dirty price.” When the next coupon is paid, the amount that represents the accrued interest paid to the seller by the new purchaser of the bond will not be taxed. The reason – it is return of the buyer’s capital. The process of deducting the accrued interest paid to the seller from the total coupon received by the buyer ensures the buyer pays taxes only on the interest that is earned.

When it comes to dividend-paying equities, the very same process occurs, but our securities markets have no mechanism to decipher between clean and dirty pricing. Essentially, if a single corporate issue security, mutual fund or ETF pays a dividend, we are quoted and must pay the dirty price. This is because the price of the equity includes the value of the unpaid distributions. Unfortunately for equity investors, they are unable to deduct the accrued income paid to the seller of the security from the total distribution received, resulting in substantial over taxation of investment income received.

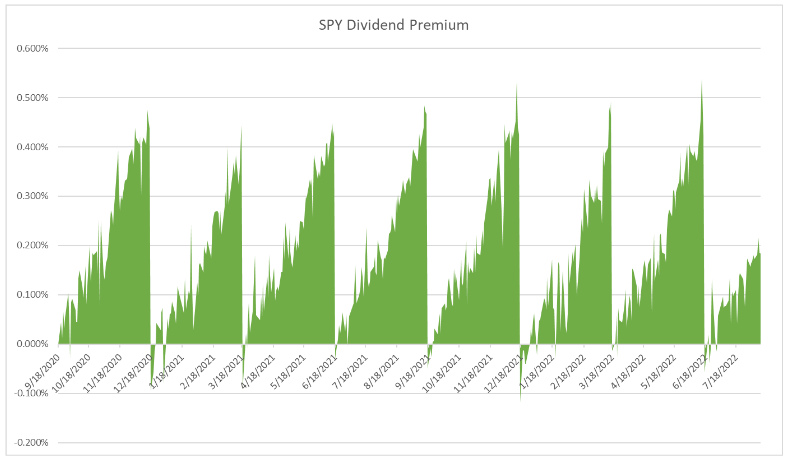

The chart below shows the difference in the percent change of SPY versus the percentage change of the S&P 500 index, anchored from the ex-dividend day. The increase in price you are seeing is the income from the S&P 500 stocks being added to the value of the S&P 500 stocks that comprise SPY. The sharp drops shown in the chart represent SPY paying its accrued dividends to investors. One can see that these drops correspond to SPY’s ex-dividend dates. This chart demonstrates that, just like bonds, equities trade dirty.

Dirty pricing creates an enormous problem for investors who buy or sell dividend-paying equities. Let’s look at trades that took place on June 16, 2022, in State Street’s S&P 500 Index ETF SPY. The closing price of SPY on this date was $366.65. Trading volume was 134 million shares. For our example, we will assume investors who purchased SPY on this day still owned SPY on the ex-dividend date, of June 17. This is important since the owners of record will be the recipients of the quarter’s dividend distribution of $1.5769 per share. This $1.5769 per share was included in the price paid for SPY on June 16. On the following day, the ex-dividend date of June 17, the price of SPY dropped by $1.5769 per share. This must happen because the dividend was finally journaled as a liability and purchasers of SPY on the ex-date were not eligible to receive the last quarter’s dividend.

Dirty pricing creates an enormous problem for investors who buy or sell dividend-paying equities. Let’s look at trades that took place on June 16, 2022, in State Street’s S&P 500 Index ETF SPY. The closing price of SPY on this date was $366.65. Trading volume was 134 million shares. For our example, we will assume investors who purchased SPY on this day still owned SPY on the ex-dividend date, of June 17. This is important since the owners of record will be the recipients of the quarter’s dividend distribution of $1.5769 per share. This $1.5769 per share was included in the price paid for SPY on June 16. On the following day, the ex-dividend date of June 17, the price of SPY dropped by $1.5769 per share. This must happen because the dividend was finally journaled as a liability and purchasers of SPY on the ex-date were not eligible to receive the last quarter’s dividend.

The inefficiencies of this dirty pricing hurts investors in three ways. The purchasers of SPY on June 16 owe taxes on the $1.5769 dividend even though the dividend received is a return of their capital investment. Nowhere in the IRS tax code is return of capital taxable – yet this happens every day to unknowing investors. If you look at the numbers, it is easy to understand the size and scope of this problem. Let’s assume 25% of the SPY trades on June 16 are in taxable accounts. Further, assume the average tax rate of the investors, in those accounts, is 30% (federal and state). (33.5 million shares X $1.5769) X 30% tax rate = $15.84 million in unnecessary taxation. Why? Because all the investors who bought SPY on June 16 also bought the dividend which was subsequently returned to them as a fully taxable distribution. This dividend payment represents a return of investor capital and should not be subject to taxation. This is just one ETF, on one day, of one quarter. Now extrapolate these investor losses from one day and one security, across all dividend-paying equities, every day, every quarter, every year.

The sellers of SPY on June 16 paid taxes on the same dividend that the buyers received. Remember, the $1.5769 dividend was included in the price when the shares were sold. Therefore, SPY was trading at $1.5769 per share higher than the value of the securities that SPY holds. The actual NAV of SPY (the clean price) was $365.07 ($366.65 – $1.5769). Since dividends inflate the price of the security, the sellers will need to pay capital gains tax on the appreciated security value. This is an example of how the same $1.5769 was double taxed. It was taxed once to the buyers in the form of a dividend distribution, and then a second time to the sellers as a capital gain.

Third, if equities were priced like bonds, equity prices would sell at their clean price or $365.07 (without embedded dividends and capital gains in the price), allowing investors to accumulate more shares at the security’s fair value, with the same amount of investment dollars. As it stands, investors are forced to purchase the inflated, dirty price. Dirty equity pricing means investors accumulate fewer shares, earn fewer future dividends, and incur hidden costs in the form of unnecessary taxation.

The same unnecessary taxation and overvaluation occurs with short- and long-term capital gains distributions, which can be substantially higher than dividend distributions. The same dirty pricing occurs with corporate-issue equities and mutual funds since they too do not treat their dividends and capital gains in mutual funds as liabilities until the ex-dividend day.

Consider the following questions:

- Why are our disclosure laws, which have been in effect since 1933, not being enforced to protect investors? If investors and advisors are given adequate and real-time disclosure, they can minimize these risks by making simple changes in their investing behavior.

- How many of your clients would be okay with paying taxes they do not legally owe?

- If the entire market for income-producing securities is overvalued and if investors are paying taxes they should not owe, are we investing client funds in a market that is "fair” and/or “efficient”?

The SEC was made aware of this problem over two years ago, and many industry participants are aware this problem can easily be fixed. But investors, your valued clients, remain unaware they are potentially losing money with each trade they make. As fiduciaries, we need to speak up and make our concerns known to security issuers, our brokers and custodians and other market participants. The good news is that we can stop this unnecessary taxation happening to our clients. By working together to raise awareness as an advisor community, a fix can be implemented, and our investors can be protected while enjoying higher portfolio returns.

To learn more about this market structure problem and the solutions to fix it, visit my company’s website. FairShares.

This article is the first article in a three-part series. The purpose of these articles is to describe a serious market structure issue that adversely impacts investor returns and buying power. In subsequent articles, I will explain how advisors can estimate client risk before committing capital and will review trading strategies advisors can use to mitigate these risks. Please make sure you subscribe to Advisor Perspectives to ensure you receive the next articles in this series.

This article is meant to describe a flaw in the securities market structure. The content should not be relied upon as legal or financial advice. This content does not constitute an offer or sale of securities or any other mechanism for purchasing securities. No party may rely on this content as legal advice or financial advice and all parties reviewing this content are advised to rely solely on their own legal and financial advisers for any specific issues.

David C. Boydell has been a financial advisor for 29 years. He is a co-founder of FairShares, Inc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All