Your Portfolio Hinges on a Bet on Inflation

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The markets are betting that inflation will soon subside, allowing the Fed to pivot. But if inflation proves persistent, the Fed will have much more work to do, to the detriment of asset prices.

There are two schools of thought on the issue of transitory versus persistent inflation.

One school thinks high rising prices will arrest the inflation surge, thus proving inflation transitory this time.

On the other side of the argument, the BIS warns that inflation can remain persistent.

Both views may be correct. The current surge in inflation may be transitory, but we may be entering a long period where inflation remains moderately above that of the last 20 years.

This article compares the two viewpoints to help appreciate how inflation might behave in the coming months and years. Given the Fed's enormous impact on markets and its extremely hawkish stance due to inflation, a well-reasoned inflation forecast is imperative for investors.

Transitory inflation

Many economists believe higher prices result in demand destruction, which normalizes supply/demand price curves and arrests sharp increases in prices over the coming months.

Walmart and other retailers help support this idea. Per Walmart's press release on 7/25/2022:

The increasing levels of food and fuel inflation are affecting how customers spend, and while we've made good progress clearing hardline categories, apparel in Walmart U.S. is requiring more markdown dollars.

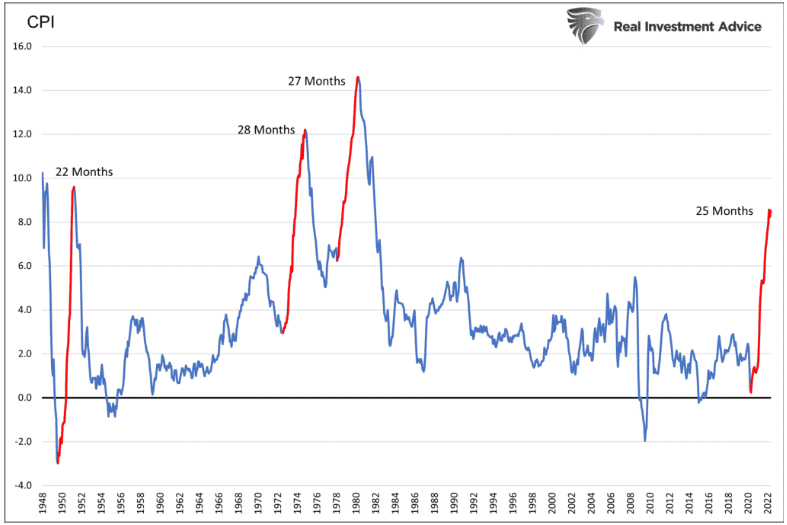

The graph below shows that prior spikes of high inflation were transitory. In those instances, high inflation rates lasted for up to two and half years but fell just as quickly as they rose.

Persistent inflation

The Bank for International Settlements (BIS) recently published Inflation: a look under the hood. In the article, it argued that high inflation regimes, as we may be entering, can be persistent, not transitory. In a high-inflation regime, inflation can be volatile and not persistently very high. Essentially the average inflation rate over the regime is elevated from that of a low-inflation regime.

If the BIS is correct, inflation may fall sharply in the next three to six months, but average inflation rates over the next decade or more may linger well above the Fed's preferred 2% objective.

Today's bout of inflation

Economist Milton Friedman once stated, "inflation is always and everywhere a monetary phenomenon." Basically, the more money, the more inflation and vice versa.

While I largely subscribe to his theory, the current bout of inflation is due to monetary machinations, as he posits, but also the result of supply problems.

Understanding how money is created is vital to understanding inflation. Contrary to popular opinion, the Fed does not print money. All money is lent into existence. The Fed adds or subtracts reserves at banks. Excess reserves allow banks to lend money and thus print money.

In 2020 and 2021, the federal government borrowed over $6 trillion. By doing so, it significantly increased the money supply. However, new money is inflationary only if the money is spent. Printing a zillion dollars and burying it in a hole will not affect prices.

Unlike the traditional spending habits of the government, during the pandemic, it borrowed and wrote checks to individuals and companies. The economy was essentially mainlining money versus a slower drip that often accompanies government borrowing and spending.

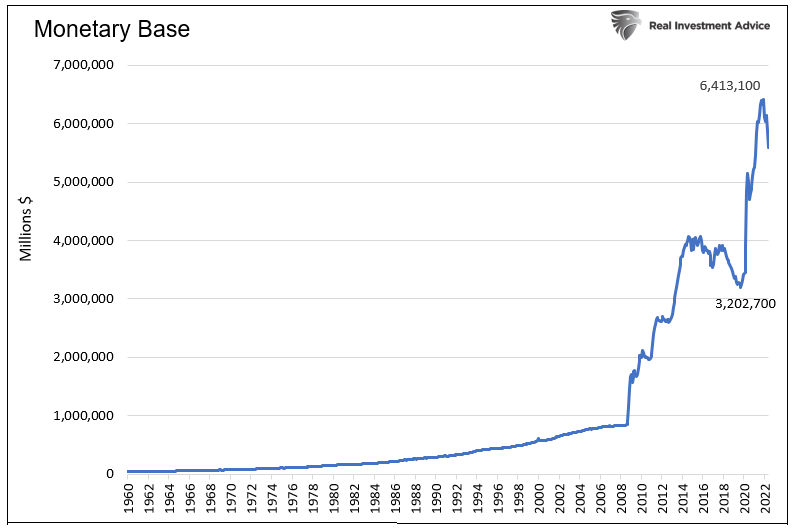

The graph below shows the monetary base rose by over $3 trillion in less than two years. That compares to a similar $3 trillion growth over seven years after the financial crisis.

At the same time money was coursing through the economy, the supply of goods and services came to a halt. Global supply lines around the world were hampered. The basic laws of supply and demand took hold, and prices surged higher.

At the same time money was coursing through the economy, the supply of goods and services came to a halt. Global supply lines around the world were hampered. The basic laws of supply and demand took hold, and prices surged higher.

The transitory view

As the graph above shows, the monetary base is starting to decline. In fact, it has declined 8.6% over the last year. Fiscal deficits have normalized, albeit at high levels. More importantly, the direct flow of money from the government to the economy has concluded. Lastly, consider the supply lines here and abroad are healing, allowing the supply of goods and services to normalize.

Assuming the current political stalemate prevents large doses of fiscal stimulus and supply line problems continue to ease, prices should fall.

Further supporting the view, wages are not keeping up with inflation, which puts consumers in a financial bind. Many people struggle with no choice but to reduce their spending or rely on credit and savings to prop it up. Personal savings have fallen to 12-year lows, and credit card use is expanding rapidly. The means to consume are dwindling.

The Fed is reducing system liquidity to fight inflation. By doing so, new money creation (bank loans) declines. Ergo, given price supply/demand curves are normalizing quickly, I believe the current bout of inflation is the cure for this bout of inflation. Like prior high inflation, the recent outbreak of transitory inflation is also coming to an end.

BIS self-feeding dynamics

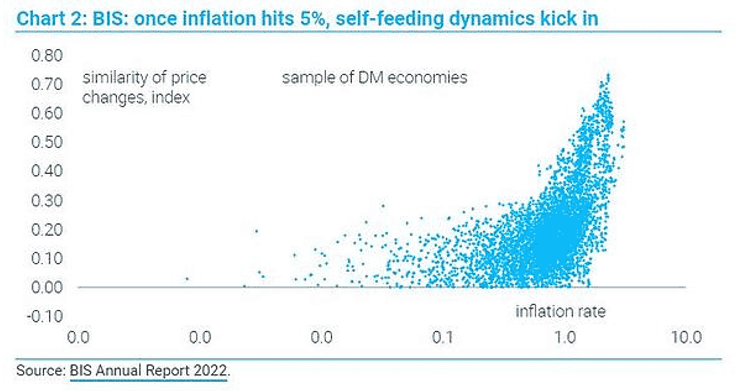

The BIS has a different opinion. It believes that as prices rise above 5% "self-feeding dynamics kick in."

The BIS explains two inflation regimes, which it calls low and high. Low is what we were accustomed to over the last 30+ years. In a low regime, the primary driver of temporary inflation is when the prices of specific goods and services rise or fall out of step with most other prices. Such changes tend to last for short periods and do not affect consumption choices.

The BIS argues that inflation drives consumer and corporate spending decisions in a high-inflation regime. This results in behavioral changes, which cause individual prices of goods and services to become more correlated. Inflation begets inflation and therefore becomes persistent.

To its point, the graph below shows that prices become more correlated with each other as inflation rates rise above 5%.

Price-wage piral

When inflation becomes recognized and is no longer perceived as transitory, personal and business economic decisions change. Per the BIS:

Once the general price level becomes a focus of attention, workers and firms will initially try to make up for the erosion of purchasing power or profit margins that they have already incurred.

This circular dynamic is known as a price-wage spiral. Employees and unions demand higher wages to combat inflation. To meet their demands and maintain profit margins, companies raise prices. Higher prices call for renewed demands for higher wages, and on and on.

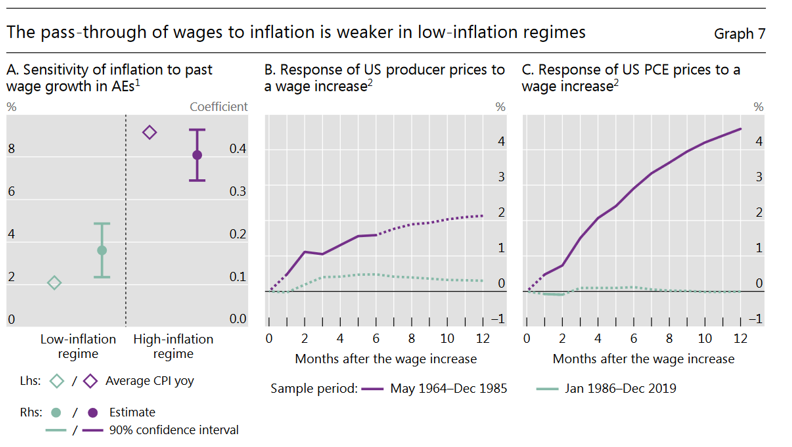

The graphs below show little correlation between wages and inflation in low inflation environments. However, the correlation picks up markedly in the 1964-1985 high-inflationary regime.

Can we compare the 1970s to 2022?

While the BIS report provides food for thought, we must consider the only recent experience with persistent inflation (>5%) was over 40+ years ago.

At the time, there was little federal debt and much less economic reliance on debt and interest rates.

Today's economy is heavily reliant on low interest rates. A two to three percent increase in interest rates will have a much more significant negative effect on the economy than 40 years ago. Because of this dynamic, Fed policy is a much bigger determinant of inflation and economic activity than it ever has been. If true, the Fed should be able to manage inflation better this time around.

Unlike in the 70s and 80s, wages are not keeping up with inflation. De-unionization and outsourcing jobs over the last 40 years are partially responsible. Until very recently, workers had little leverage. If that is changing in today's tight labor market, the odds of a price-wage spiral will increase.

Summary

Stay humble on your inflation stance. No one knows whether inflation will be transitory or persistent. While I think transitory, there are many forces driving prices, and the relationship between many of them is not fully understood or appreciated.

If a price-wage spiral develops, the likelihood of persistent inflation is real. This scenario must scare the Fed. It will force it to reduce employment and kick the legs out of a wage-price spiral.

In the late 1970s, P/Es on stocks were in the single digits, and debt levels were negligible. Today, valuations are nearly four times those levels, and debt as a percentage of GDP is at levels considered unthinkable not that long ago. As I wrote above, Fed monetary policy is much more influential on economic activity because of the enormous reliance on debt and interest rates. Accordingly, its policy actions and direct and indirect effects on liquidity greatly influence asset prices.

The Fed is in the driver's seat, and its reaction to inflation will dictate market returns.

Pay attention; this is not the 1970s!

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com.

Contact him at [email protected].

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All