Business Cycles, Sector Tilts, and Investment Policy

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Sector tilting during cycle phases is one way to improve your risk-adjusted performance.

Introduction

The ebb and flow of economic activity is called the business cycle. A cycle consists of expansions occurring at about the same time in many economic activities, followed by general slowdowns, recessions and recoveries, which merge into the expansion phase of the next cycle.

During each of these business cycle phases, certain market sectors and the industries that feed into them outperform the market averages, while others underperform. Investment policy is a tool for taking advantage of this disparity in performance by tilting portfolio allocations in a way that lines up with where we are in the cycle.

Changing your sector tilt as the economy and the market transition from one phase to the next can boost your returns and increase your Sharpe and Sortino ratios, if done judiciously.

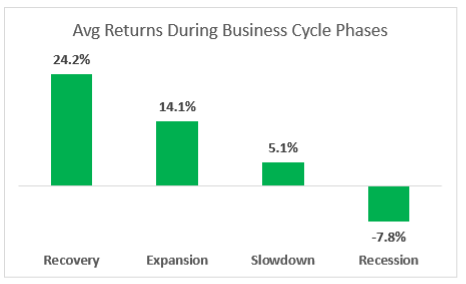

Chart 1. Equity returns during business cycle phases

Table 1. Period returns for all sectors by cycle phase

Phases of the business cycle

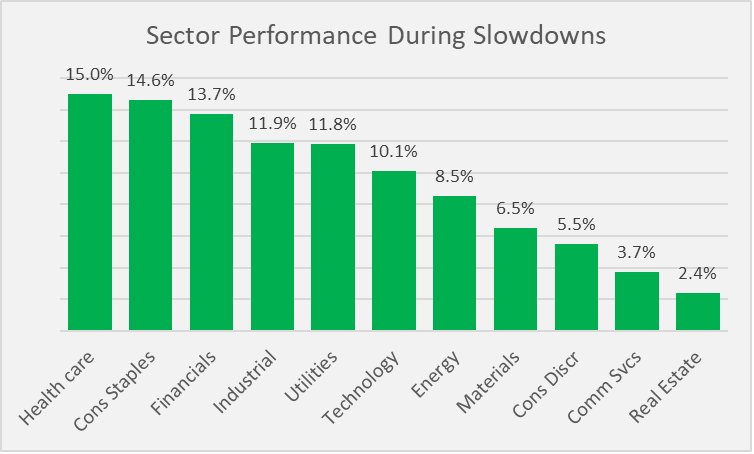

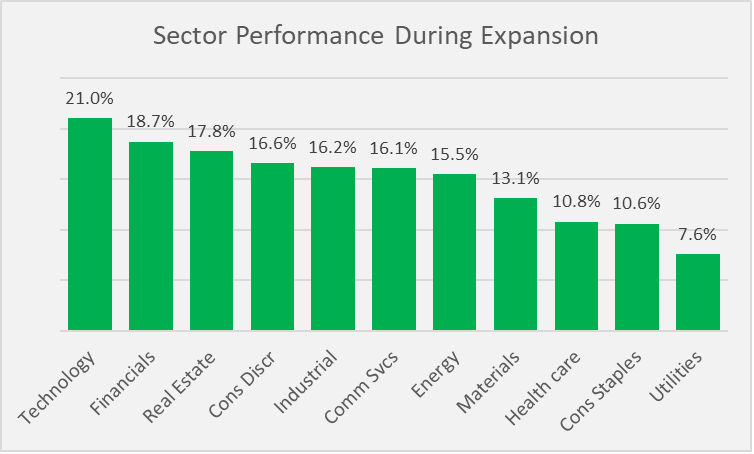

During the slowdown phase, like the one we’re in now, the three best sectors in terms of outperformance are consumer staples, healthcare, and industrials. Staples have a period return of 14.6% (the total price gain over the duration of the slowdown period). Healthcare generates a 15% period return, and industrials gain 11.9%.

Chart 2. Sector performance during slowdowns

Slowdowns last about 10 months on average. Growth slows while moving from above-trend to below-trend. Slowdowns lead to the next phase – recession.

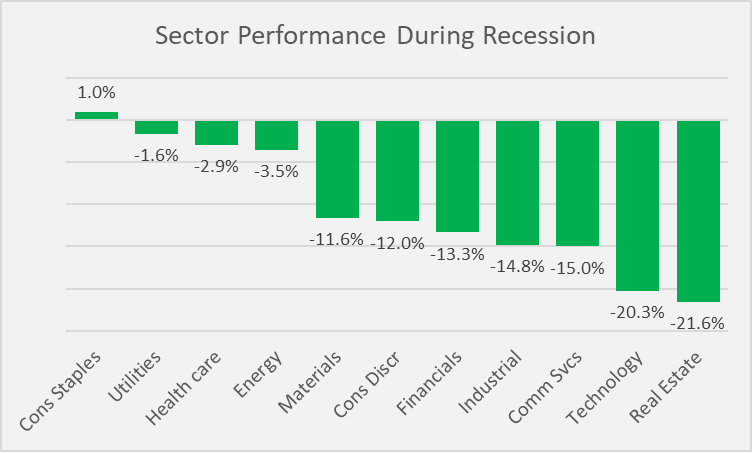

In a recession, consumer staples hold up the best, gaining 1% while healthcare loses 2.9% and utilities lose 1.9% over the period. An investor who follows the business cycle and knows something about sector flows as part of his investment policy would drop exposure to industrials, since they lose 14.8% for the period.

Chart 3. Sector performance during recessions

Recessions last about 17 months on average. The damage done during recessions is persistent, pervasive, and pronounced.

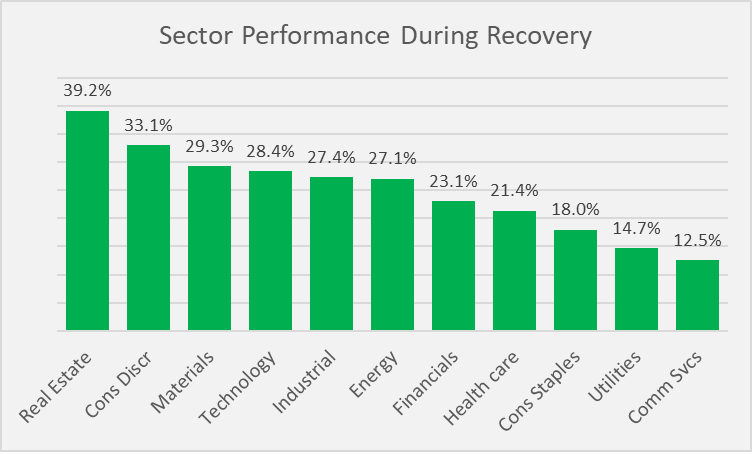

In a recovery, the market has its best performance of any period – up 24.2%. The top performing sectors are consumer discretionary, real estate, and materials. Sectors to avoid include healthcare, consumer staples, and utilities.

Chart 4. Sector performance during recoveries

Recoveries last about nine months on average. After the recession hits bottom, the leading economic index (LEI) begins to show positive improvement, albeit still below long-term trends.

In an expansion, the market gains 14.1% on average for the period. Why is this number so small when the typical expansion lasts about five years? Because of the outsized gains from the earlier recovery phase. A 14.1% gain on top of a 24.2% gain creates a five-year gain of 42%. That works out to an average annual gain of 8.4%. Add in the 5.1% boost from the slowdown phase and you get an annual return of 9.8%.

Chart 5. Sector performance during expansions

Expansions typically last about five years. Economic growth is positive and above long-term trends. Eventually, expansions run their course and devolve into the next phase – slowdowns.

Final thoughts

An investor can realistically expect to add about 2-3 percent annually to their portfolio returns by paying attention to where we are in the business cycle and which sectors to tilt towards, and which to tilt away from. I recommend doing this within the framework of a written and detailed investment policy statement (IPS).

By laying out each step to take as the economy transitions, much of the subjectivity and guesswork will be removed from the process. This, in turn, will lead to greater success.

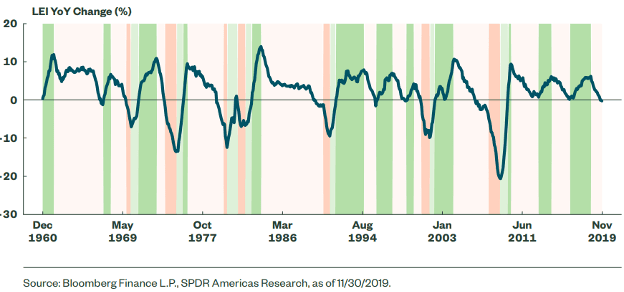

The hard part is correctly identifying the transition points. One can use the Conference Board’s Index of Leading Economic Indicators (LEI), for example. Here’s a chart of LEI dating back to 1960.

Chart 6. LEI back to 1960

Legend

In addition to the LEI, some of the investors I’ve coached also consider things like the unemployment rate, industrial production, and the Chicago Fed National Activity Index (CFNAI). All these indicators give clues about where we are in the cycle.

Implementation can be tricky and cumbersome, which is why I recommend that this type of approach be done with the help of a well-thought-out IPS that includes clear trading rules.

The most popular vehicle for tilting, by far, is the sector ETF. With just two trades, one can increase exposure to one sector and reduce exposure to another. The most active you would need to be is doing six trades – three buys and three sells – to change the tilt of six sectors. I don’t recommend going beyond this level of activity because it becomes counterproductive to do so. The costs associated with excessive trading can be quite high, not to mention the amount of time you would have to spend on rebalancing the sectors.

Investors who use this approach are fortunate to have an economy that moves more like an ocean liner than a speedboat.

Erik Conley is the former head of equity trading at Northern Trust Co. in Chicago. After a 30-year career in trading and portfolio management, he now runs a nonprofit investor education and advocacy organization called ZenInvestor NFP. His website is www.ZenInvestor.org and you can reach him at [email protected].

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All