Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Social Security benefit formula is short-changing a select group of retirees, and the losses are apt to exceed $25,000 over a lifetime. There is no effort to fix the flaw, so the concern is on-going.

In response, financial advisors need to revisit claiming strategies for past and present clients.

The benefits formula of Social Security overly penalizes certain retirees who worked some part of their career earning a pension in lieu of participating in Social Security system.

Retirees who are subject to the Government Pension Offset (GPO) provision who claimed spousal or survivor benefits before full retirement are likely getting a lot less than what they should. The impact on lifetime benefits is substantial and varies by client.

There is no effort in motion to address this problem, and responses to address the losses are apt to come up well short of an entire cleanup.

In 2019, the Office of the Inspector General completed an audit of Social Security, concluding that the agency action had cost one segment of seniors more than $25,000 on average as a result of incomplete or inaccurate advice provided by the agency. Specifically, the agency had failed to explain the full cost of early retirement adjustments to seniors subject to the GPO.

While reading the audit can help an advisor understand the issue, the report appears to understate the losses and the populations affected. If your client is subject to the GPO, they need to understand that claiming spousal or widow(er) benefits can be a very expensive mistake.

In general, the solution to neutralize the quirk for your client is to withdraw their application for widow-benefits and re-file their claim as of their full retirement age. According to the audit report, “Widow(er)s have the option to withdraw their application for widow(er)’s benefits and reapply for benefits up to FRA to increase their monthly benefit amount as long as they repay any benefits they received.”

This response seems simple enough. The advisor needs to pay attention to the scope of the audit, which seems too small. The estimate of losses also appears to be too small.

The focus of the audit was seniors (1) who claimed widow(er) benefits before full retirement age; and (2) whose benefit was entirely offset by the GPO. I see no reason that seniors with spousal benefits would be unaffected. Moreover, there is no reason to exclude people who are subject to a partial GPO offset.

For a bit of background, the GPO affects people who earned an employer pension in lieu of participating in the Social Security system. For the most part, these are state and local employees whose employment is exempt from Social Security.

The purpose of the GPO adjustment is to provide those seniors roughly the same level of spousal benefit that they would have received had they worked in a job covered by Social Security. (You can read about it here.)

While the concept is fair and sensible, the execution of that objective is horribly flawed. Specifically, the calculation of the GPO offset assumes that the retiree waits until full-retirement age (FRA) to claim benefits. The offset wipes out a much larger portion of a spousal/widow(er) benefit than it should when a retiree claims benefits before full-retirement age.

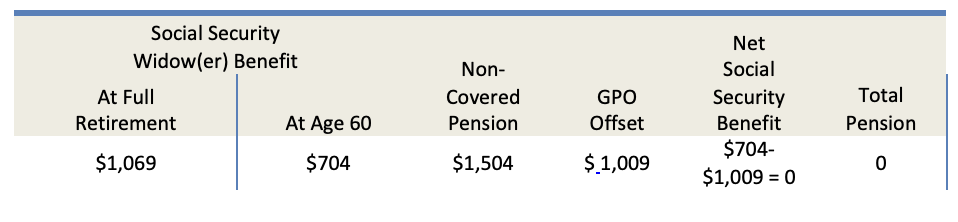

In a worst-case scenario, the full offset is applied to someone who only collects 71.5% of their entitled benefit (see the penalty schedule). To illustrate, the audit provided an example of a woman who lost $26,624 over her projected lifetime as a result of claiming benefits at the age of 60.

To illustrate1:

Essentially, by claiming benefits before FRA, the woman ensured that she might never collect benefits.

The cost of this design flaw will be higher than what the OIG estimated because inflation has risen sharply since 2019.

Since SSA provides for annual increases in Social Security benefits based on a cost-of-living adjustment, 15 widow(er)s who are subject to GPO may become eligible for benefits at FRA even if they were not eligible when they applied for reduced benefits. – OIG audit

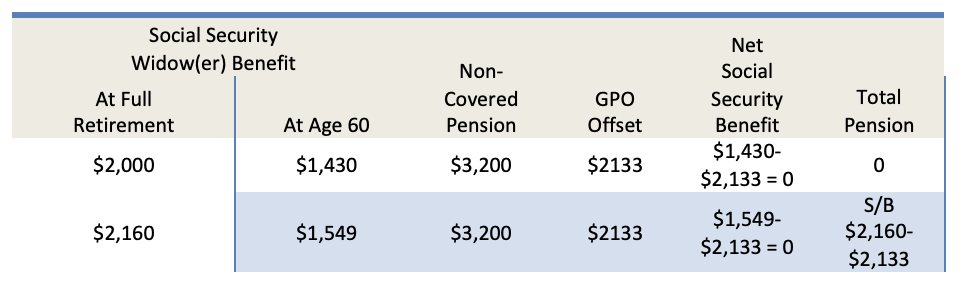

See here:

The audit puts the responsibility of the claiming decision upon the client – and thereby on the advisor. The Social Security Administration need only provide the advantages and disadvantages of filing an application. Essentially, the claimant is responsible for the cost of an informed filing decision.

If you have a client subject to the GPO who claimed benefits prior to FRA, they are likely entitled to more money.

Disclaimer: Calls to the media line of the Office of the Inspector General to get clarity on the scope of the problem were not returned.

Brenton Smith writes on the issue of Social Security reform with work appearing in Barron's, Forbes, MarketWatch, TheHill, USAToday, and more. He can be reached at [email protected].

1This example is from the audit, to see example case, visit here on the SSA.gov website.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.