In Volatile Markets, Patience is Your Friend

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The financial markets have been volatile since the beginning of the year. After three great years, the stock market has been down significantly in 2022. Interest rates have risen causing bond prices to fall too. That’s a double whammy we haven’t seen too often.

In the face of this bad news, what, if anything, should you do to adjust your long-term portfolio management strategy? If you developed a sound strategy in the first place, and built a solid portfolio to implement it, your best bet is to do nothing. Here’s why.

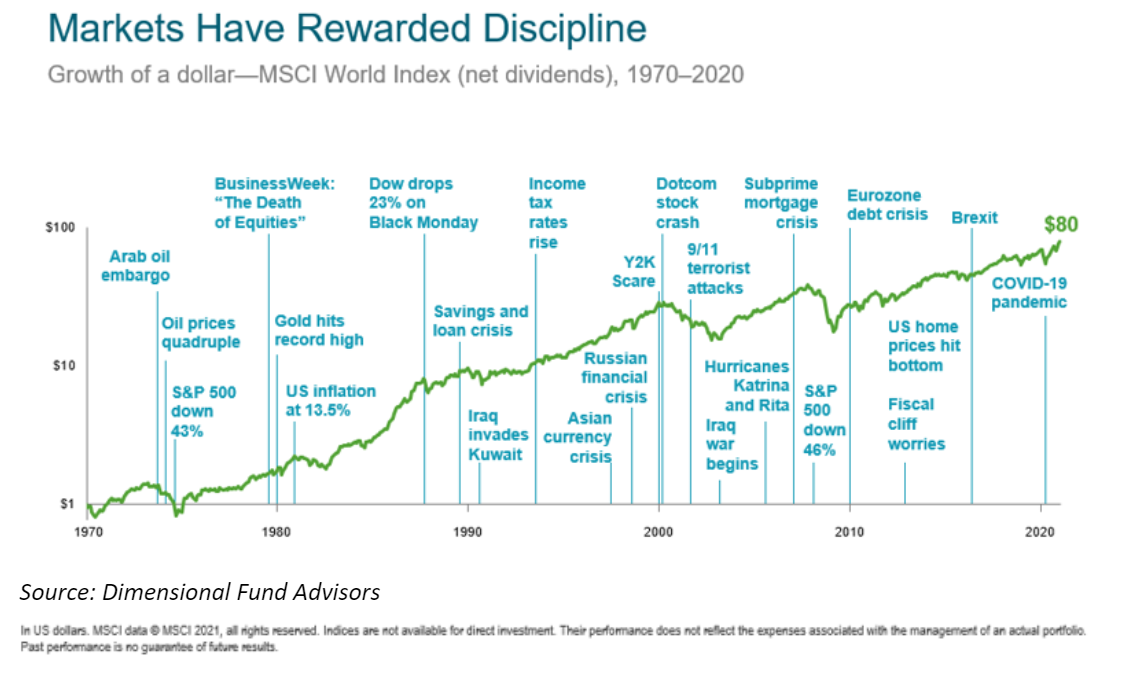

The stock market

There are always grim headlines about turmoil in the financial markets, threats to world peace, or disasters of one kind or another. As you can see below, the stock market has historically risen over time despite the headlines.

Unfortunately, the ride up is not a smooth one.

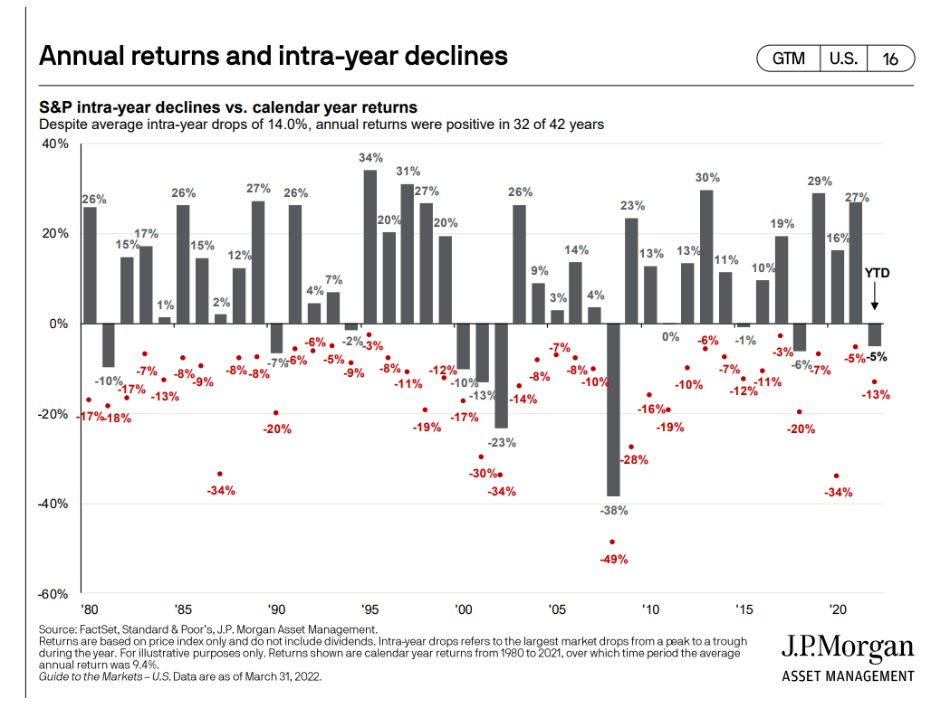

Since 1980, the S&P 500 index has had positive returns in 32 of the past 42 years. But the red dots in the graphic below show that in most years, even the positive ones, there has been a significant decline at some point. The average decline is about 14%, which is not too far off the decline we have seen so far in 2022.

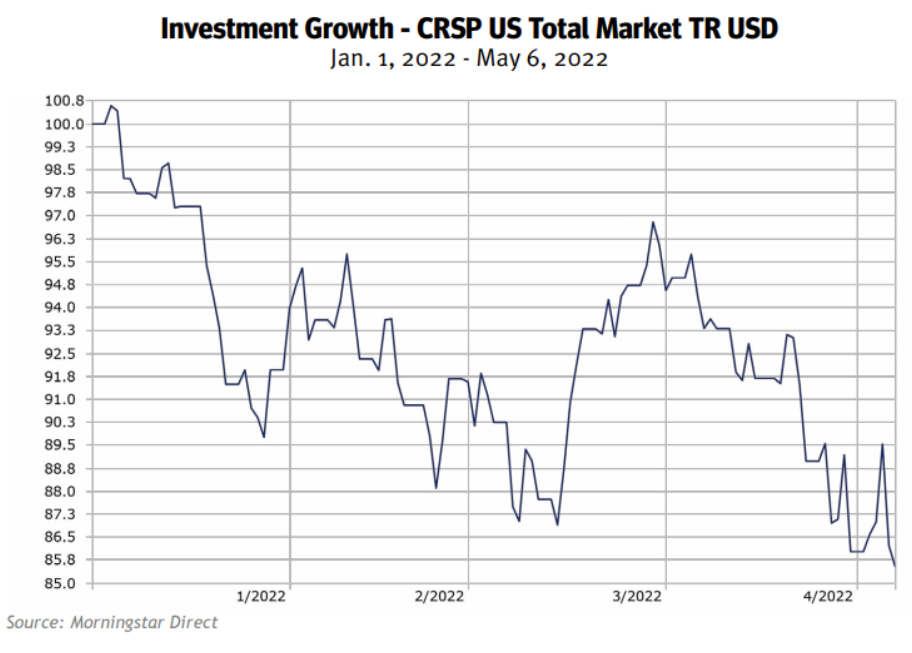

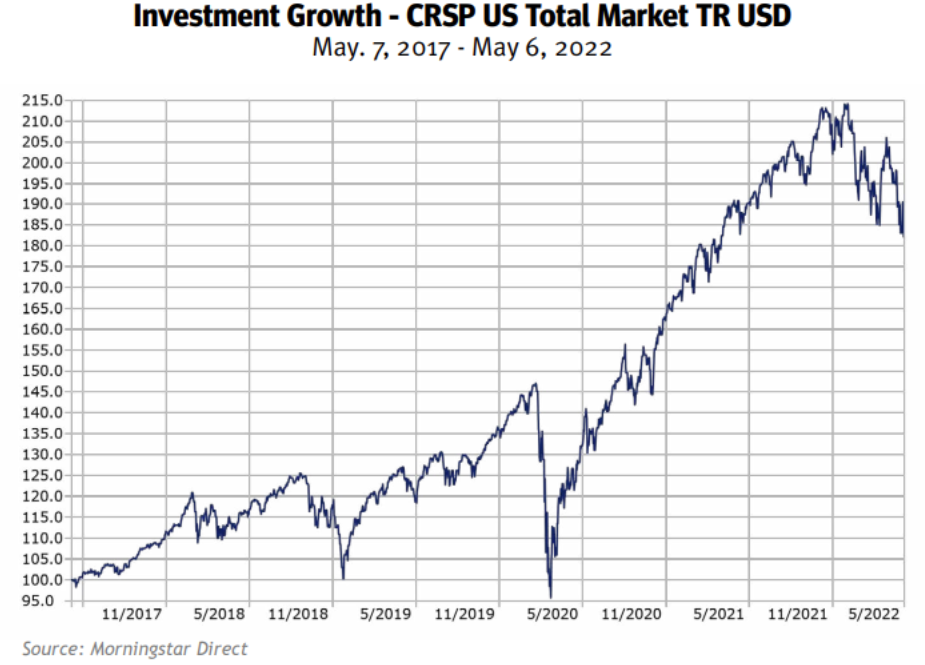

Let’s put this year’s stock market decline in perspective. As you can see below, the market was down for the year almost 15% as of May 6, 2022. That doesn’t feel good to anybody.

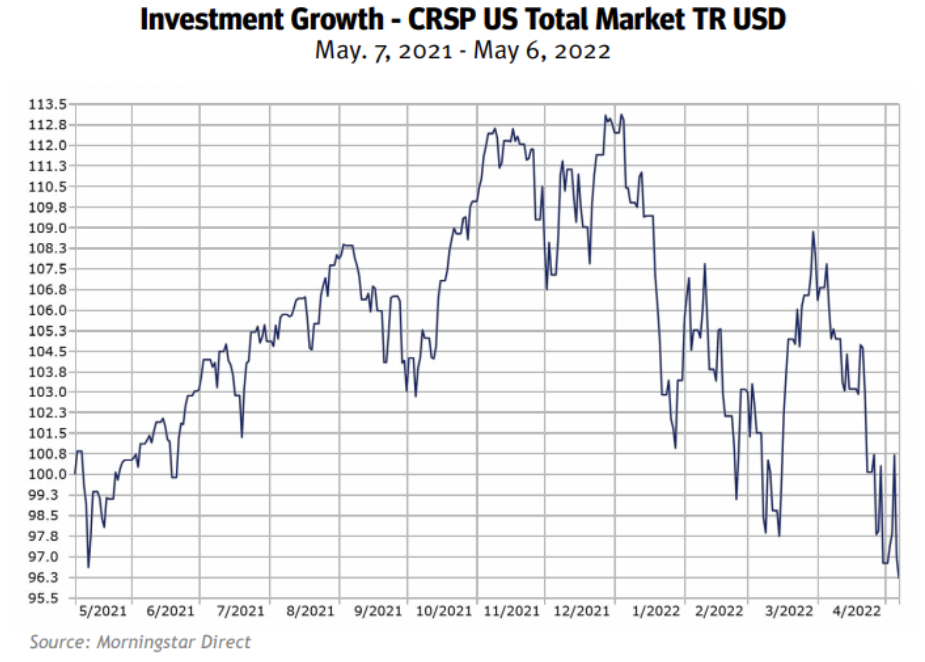

But looking back over the past 12 months, we are not too far off where we were a year ago. Not great, but not terrible.

Now let’s look back over the last five years. You can see that even with the recent declines and the Bear market we experienced in 2020, we are still far ahead of where we were 5 years ago.

This shows the value of patience in the market.

The stock market’s recent behavior is well within historic expectations. There is no reason to expect its behavior to depart from historical patterns going forward. There will be ups and downs as we move forward, but the market should rise over the long-term.

When it does, investors will benefit again from the strong returns the stock markets have historically provided.

The bond market

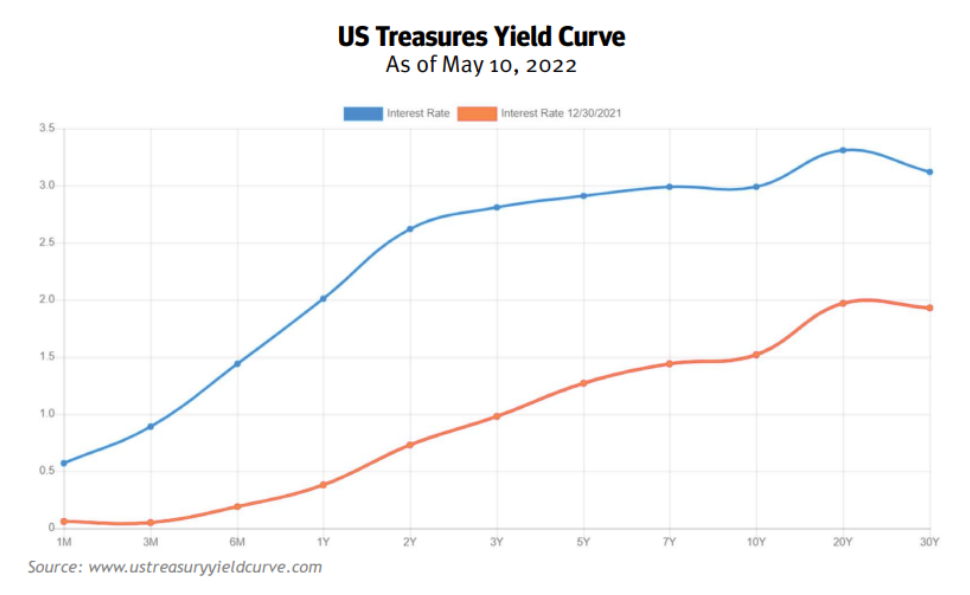

Interest rates have been rising. The red line is where interest rates were at the end of last year and the blue line shows where they were as of May 10th.

There are several logical reasons for this rise in rates. They include inflation, COVID-related supply chain issues, the war in Ukraine, and the Fed’s efforts to tame inflation.

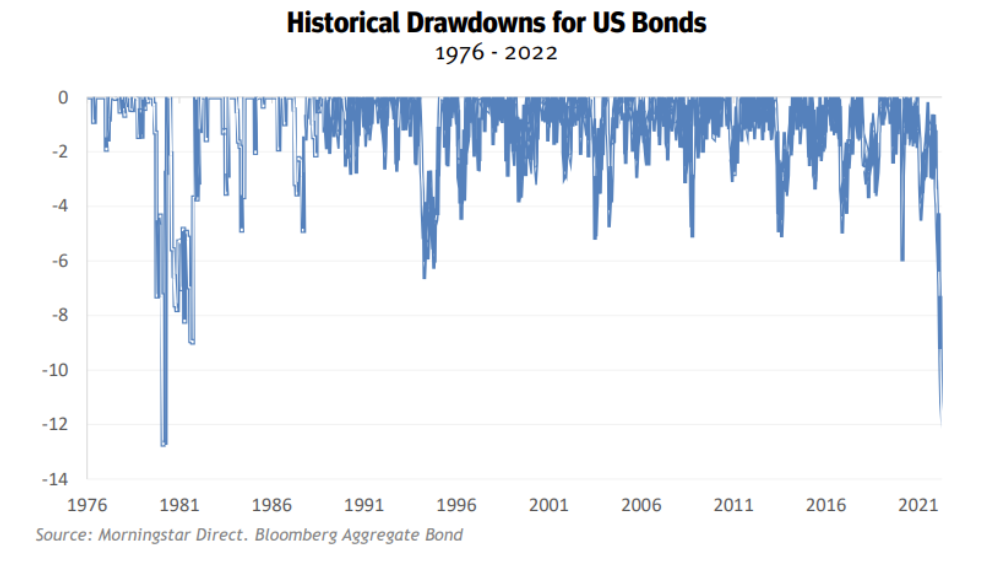

When interest rates rise, bond prices fall. Below you can see the recent decline in bond prices and compare it to other periods when bond prices have declined since 1976.

The decline is significant. Since 1976, bond prices have fallen more on only one occasion.

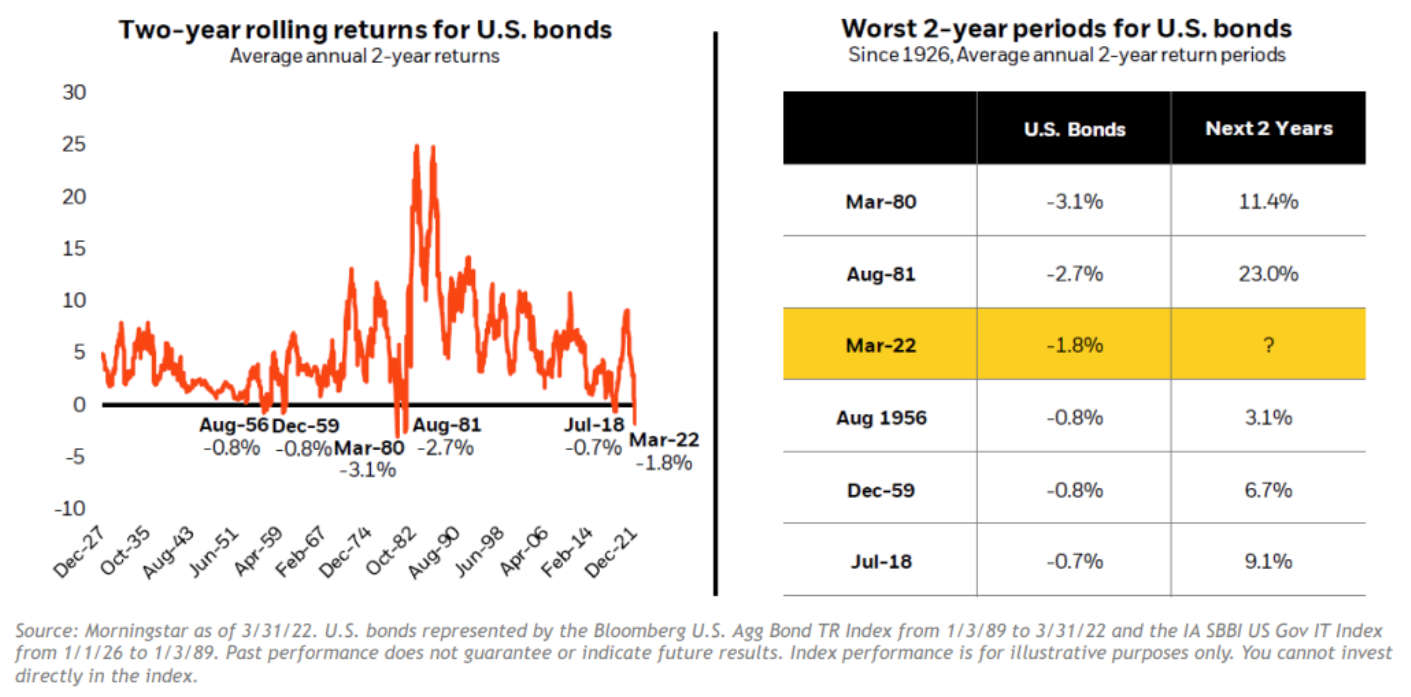

What should investors do about that? When the bond market reaches historical lows. Does it make sense to get out of bonds or stay invested and wait for the turn-around?

The historical data shows that rising interest rates and falling bond prices have little predictive value. That is, the fact that rates are rising, and bond prices are falling in one period tells you next to nothing about how bonds will perform in future time periods.

Bad news today can turn into good news tomorrow.

In fact, this is what we have seen historically when bond prices have fallen significantly.

The graphic below, courtesy of BlackRock, shows what happened in other periods where bond performance has been particularly bad. It shows that when bonds have had their worst two-year performance, the subsequent two years have produced very good returns.

If this pattern holds, we could see a similar pattern emerge; that would be good news.

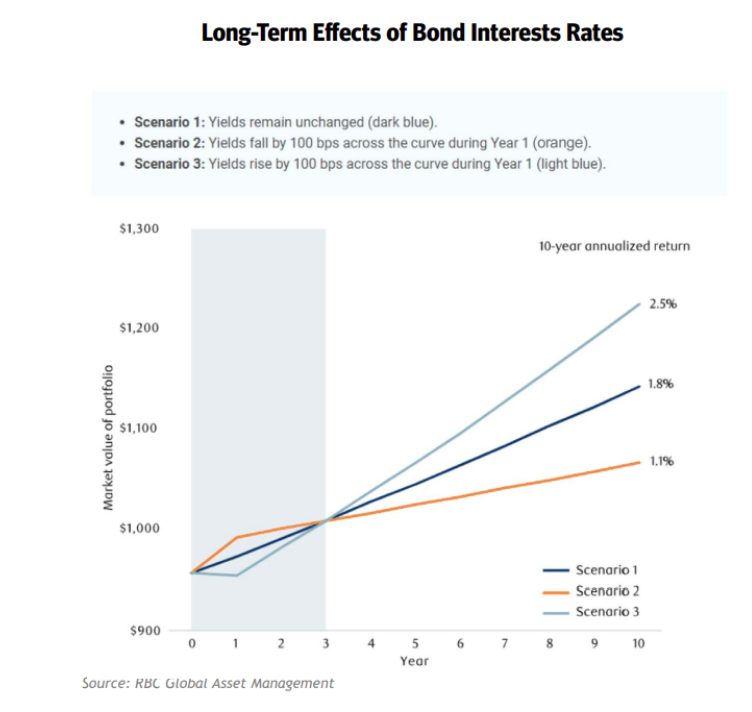

The graphic below shows the long-term effect on investors when interest rates go up, stay the same, or go down.

The yellow line shows what happens when interest rates go down. You see that in the short-term bond prices go up, which feels good at the time. But in subsequent years, because interest rates are lower, the long-term return to investors is also lower.

The dark blue line shows what happens when interest rates stay the same. You just continue to get the current interest rate on your bonds.

The light blue line shows what happens when interest rates rise – that’s the situation we are in today. Initially bond prices fall, as we’ve seen recently. But after a while you get the benefit of those higher interest rates in your portfolio and your long-term return is higher.

There are two other reasons why it makes sense to continue holding bonds in your portfolio. The first is capital preservation. Bonds are much less volatile than stocks. The second is diversification. Holding bonds is a very good way to offset the volatility of stocks.

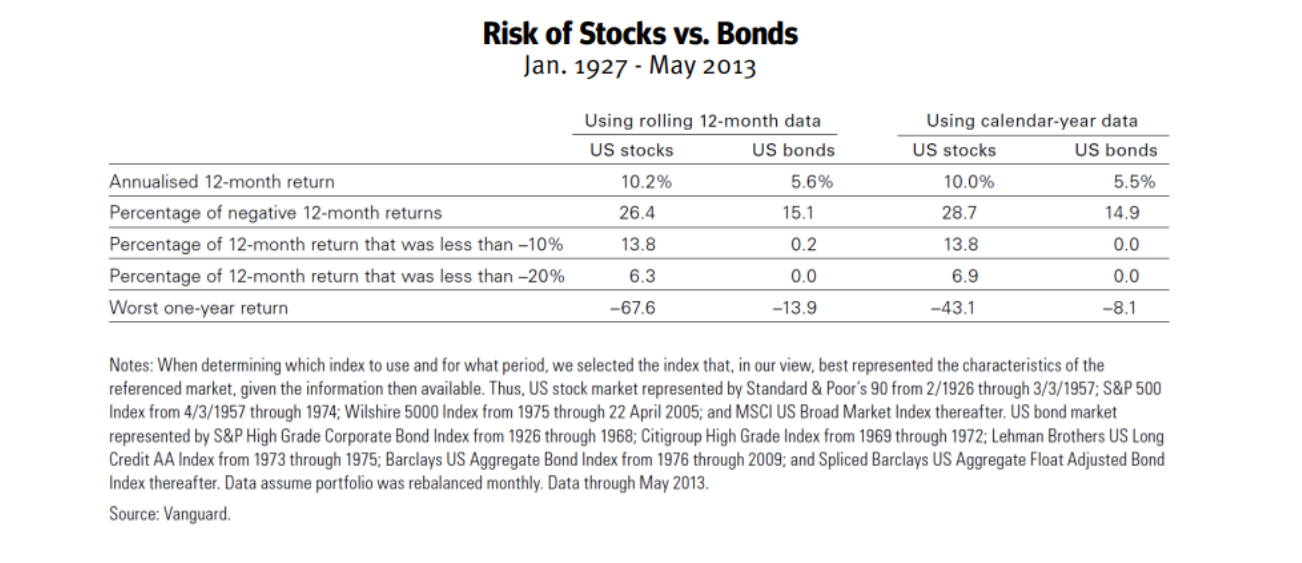

The graphic below helps illustrate this point.

You can see that between 1927 and 2013 stocks returned about twice as much as bonds on an annualized basis. But you also see that stocks had negative returns in about a quarter of those time periods and bonds had negative returns about half as often as stocks. Often bonds provided positive returns to the portfolio while stocks were struggling.

On the third and fourth lines you see that stocks experienced losses of 10% and even 20% with some frequency, while bonds rarely, if ever, did. You also see that when stocks had their worst years, their value declined dramatically. The worst years for bonds were mild by comparison.

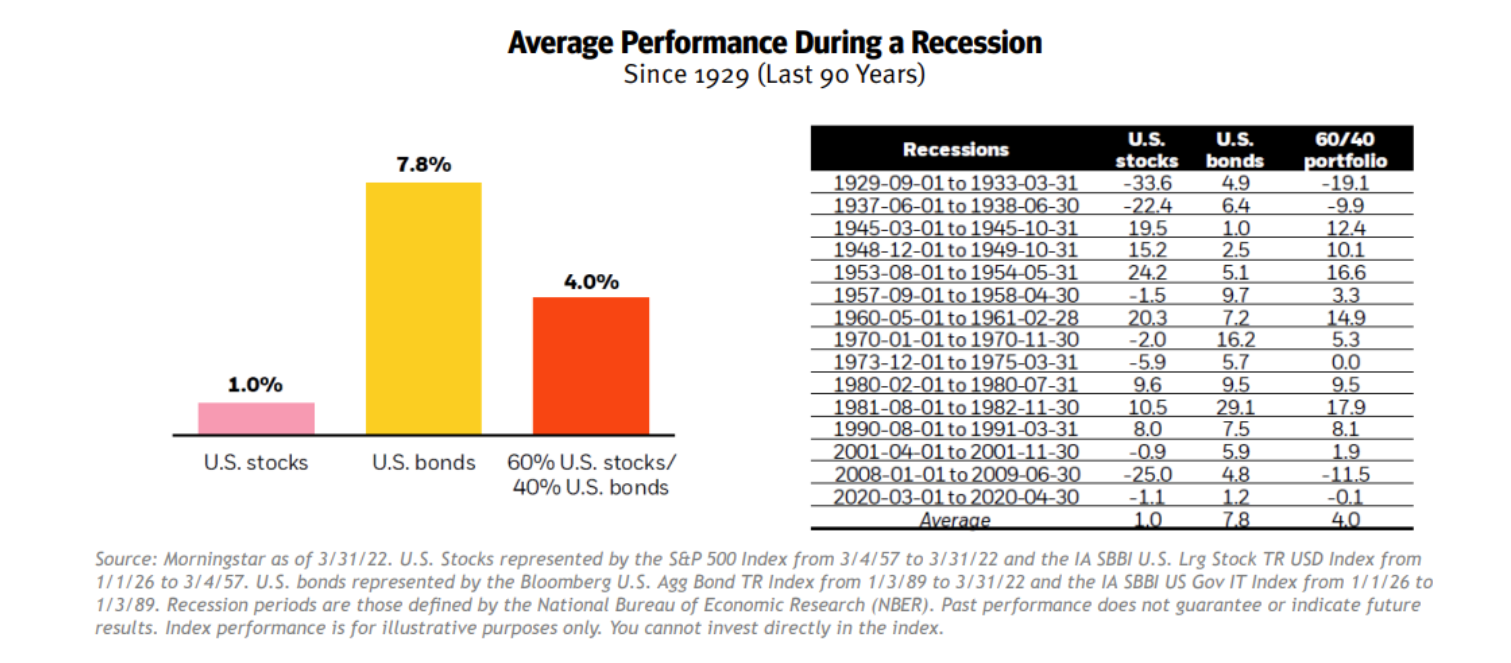

The graphic below, again from BlackRock, also shows the value of combining stocks and bonds to protect the portfolio’s value during difficult periods.

On the right you see all the recessions we’ve had in the U.S. since 1929. You can also see the returns of stocks and bonds during those periods, as well as the returns of a portfolio consisting of 60% stocks and 40% bonds.

Stocks frequently experienced negative returns during recessionary periods. Bonds never did. By combining stocks and bonds in the 60/40 portfolio you reduced the number and the magnitude of the negative returns.

On the left of the slide of the graphic, you’ll see that stocks did poorly during recessionary periods, returning only 1% annually on average. Bonds, on the other hand- did well, returning 7.8% annually. By combining stocks and bonds in the 60/40 portfolio the bonds were able to lift the performance of the portfolio to a respectable 4% during these recessionary periods.

Resist the temptation to time the markets

Many people are tempted during difficult times in the markets to cash in their chips and head to the sidelines until things look brighter. Or they may want to reduce exposure to particular asset classes that aren’t doing well and then jump back in when performance improves.

Market timing doesn’t work. Despite what your emotions tell you, it is impossible to know ahead of time if you are heading into a bad period, and it is impossible to know ahead of time when things have finally turned around.

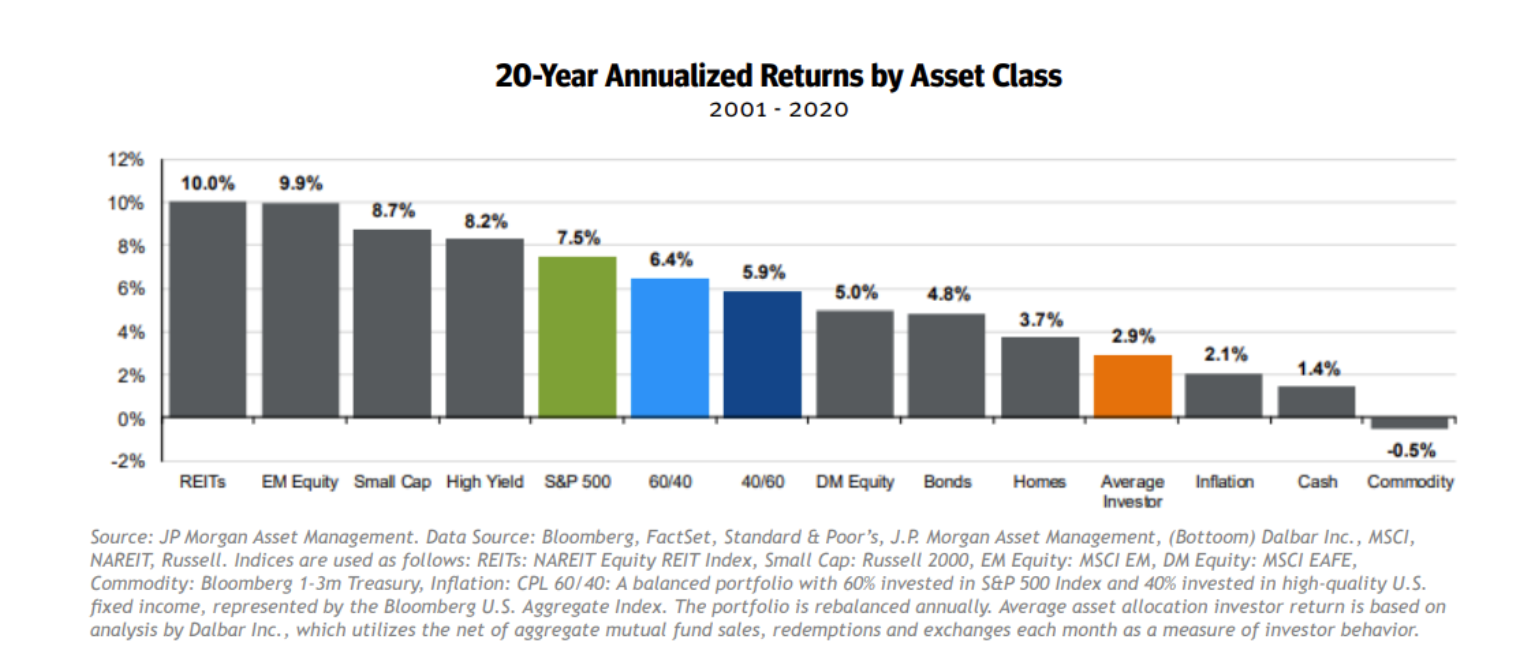

The graphic below shows just how damaging trying to time the markets can be to an investor’s performance. It shows the returns of various asset classes from 2001 through 2020. It also shows the return for the average investor during this period in the orange bar.

The average investor generated only 2.9% annually during a period when almost every asset class, including stocks and bonds, did much better. How could this be? It’s because investors try to time the market and they almost always get it wrong.

You don’t have to predict the future to be a successful investor. Look at the two blue bars representing the 60/40 portfolio and the 40/60 portfolio. If you had invested in one of those portfolios and just stayed put, you would have done over twice as well as the average investor.

Successful investors have patience and discipline. They learn to sit tight during difficult periods and wait for the better times that always come.

Scott MacKillop, Patrick Krulik, CFA, and Geoff Selzer, CFA are members of the investment committee of First Ascent Asset Management. First Ascent provides outsourced portfolio management services to financial advisors and their clients on a flat-fee basis.

Read more articles by Scott MacKillop, Patrick Krulik and Geoff Selzer

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All