”Apple” Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The following is a hypothetical and fictional account of how big tech can disrupt the wealth management industry. A back-to-client focus is discussed, reminiscent of how Apple’s Mac OS empowered users and supplanted predecessor operating systems.

Michael, head of venture investments, has requested a meeting with Robert, the board member in charge of the investment sub-committee. Stefan, one of Michael’s young analysts, has also been instructed to prepare a proposal for his new investment idea. Stefan has been cautioned by Michael about Robert’s disdain for time wasting. They are in the boardroom waiting for Robert.

“Remember to be short and precise. My guess is you have 10 minutes to capture Robert’s attention.” Robert arrives on time, gives a friendly nod to the guests, and takes a seat at the opposite table.

What do we have on the table today, Michael?

A novel approach to the wealth management industry, a key adjacency market.

You are referring to another fintech.

Not exactly. Fintechs concentrate on disrupting certain functions within the pipes of the system. This, on the other hand, is about a fresh approach to the entire industry. Stefan is the one who came up with the idea.

Let us hear it, but keep it brief. I am in the middle of two meetings. Stefan, what is the issue you would like us to address?

Stefan sits up straight, clears his throat, and selects his first slide from the computer screen. Robert pays little attention to the slide and instead focuses on Stefan.

The issue is a paradox within the wealth management industry.

Paradox?

The irony of a highly tailored industry gradually becoming pret-a-porter. It started a few decades ago, when WM started adopting the pension fund industry’s methodology or “operating system.”

So?

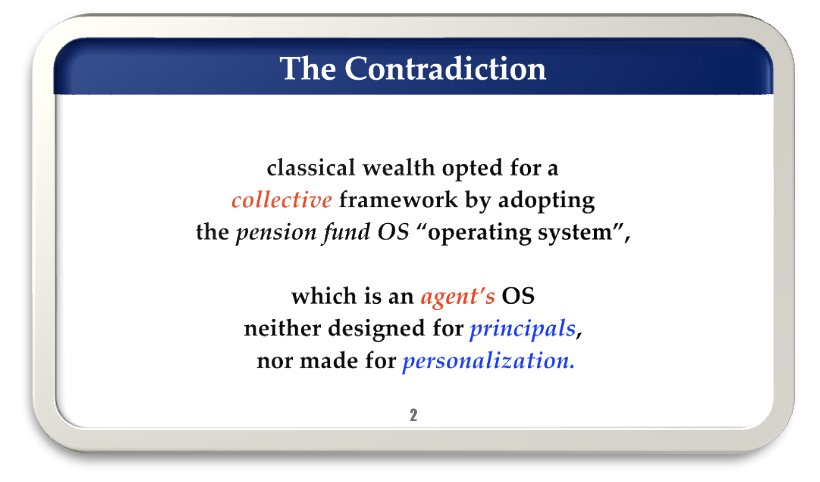

Although this pension fund OS is well-suited for pension fund agents, it is a poor fit for WM principals. It turned out to be a pret-a-porter software framework.

What is the opportunity for us?

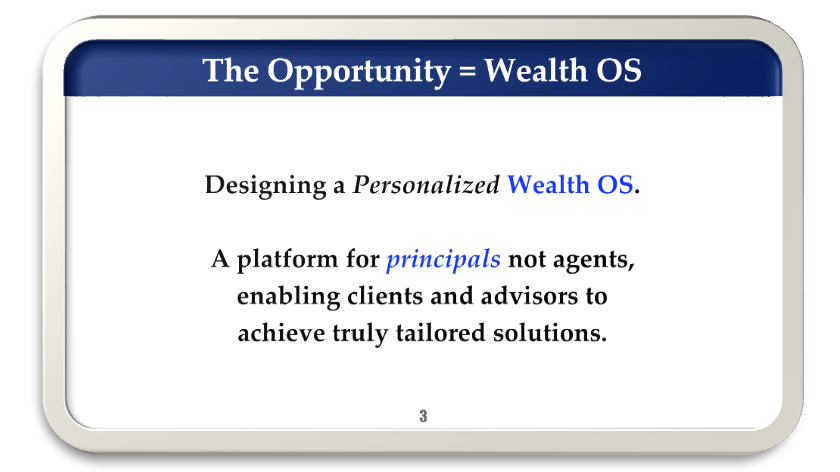

Getting to the bottom of this mismatch. Creating the world’s first personalized wealth management OS. Instead of agents, this OS will be built and tailored for principals.

Ambitious enough! Nevertheless, please assist me in better understanding. Are you suggesting the existing PF OS is the source of the issue? Why? Is it just out of date?

Well, it is over 50 years old, but it still works fine for pension funds.

Yet?

Yet it has evolved into a problem for WM.

Why did WM choose this software to begin with?

Stefan paused for a second, trying his best to be succinct.

It was a well-developed, ready-made OS with regulatory approval, and academic anchoring. WM was growing fast but lacked its own OS. This version was free of charge and ready to go.

Can you explain why precisely it is not a good fit for WM?

There are two major reasons. The first relates to the PF OS origins. It is a system designed for agents, not for principals.

Robert was not sure where this was going.

Are you hinting at a principal-agent problem?

The answer is yes and no. It is really a case of fundamental differences between pension fund and WM principals. Perhaps the design principles need to be different as well.

What do you mean?

Principals of pension funds are captive collective principals. They do not really have much of a choice concerning their investments. Agents makes decisions on their behalf. Agents’ goals influenced the development of the PF OS based on modern portfolio theory. WM principals, on the other hand, are actual individuals.

Robert paused for a moment, and then continued.

What about the second reason?

The second reason is about the unintended consequences of the software. The intended consequence followed modern portfolio theory toward a logic of averaging.

The unintended consequence?

That the software empirically has turned out to be passive at core.

Passive?

Demand from pension funds effectively launched the asset management industry. This industry is in crisis because of the failed promise of active returns. Pension funds are increasingly moving to passive management. We have some notes on this in the appendix.

All right, let me see what we have got so far. Your thesis is that (a) the WM industry has borrowed its OS from pension funds, (b) the PF OS was designed with agents rather than principals in mind, and © the PF OS contains features, which become bugs when applied to WM clients.

Stefan glanced at his watch. They had passed the 10-minute mark. He felt more at ease.

I could not have put it better myself.

Can you elaborate on these feature-bugs for me?

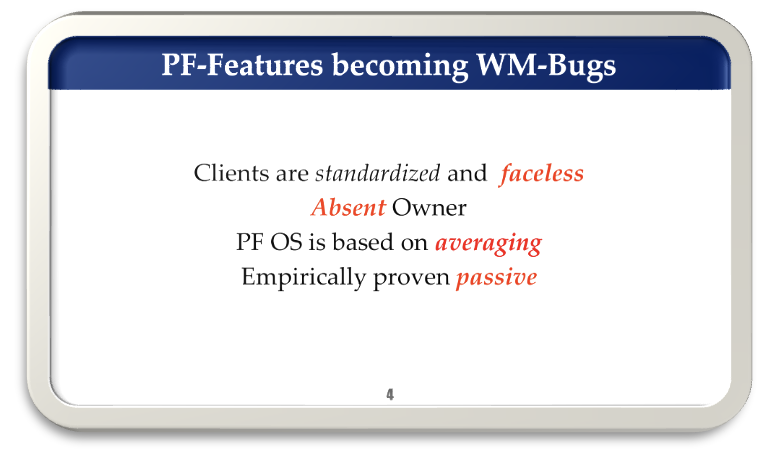

Feature number one is that PF OS uses the rational investor as a standardized and faceless client perspective. This is a good approximation for a pension fund’s collectivity, but it is a bug when it comes to WM client individualism. The absence of the owner is the other feature.

What exactly do you mean when you say the owner is absent?

Money that belongs to many is money owned by none. In the case of WM, you face the owner in person. When it comes to pension funds, you are dealing with agents, with ownership postponed to distant future.

Are there any additional bugs?

The third feature is that the software’s internal algorithm is averaging.

What exactly do you mean?

A combination of simple averages is what the software implementation delivers. It is a four-step process.

-

-

- Averaging of single investments into asset classes;

- Averaging asset classes into average risk profiles;

- Averaging risk profiles for averaged clients, which only works when

- Averaged over long investment horizon.

-

This is one of the reasons behind the software’s negative view of advisors. Advisors are pushed towards benchmarks, and the process is reinforced by regulators, gradually transforming WM into a pret-a-porter industry.

Robert looked at this wristwatch. It was time to move on.

I think I get the message. What about the concrete opportunity? Do you have any idea what the WM OS might look like?

There are some concepts and general directions, but they are still in their infancy.

Good. You have three weeks to come up with a viable proposition. Michael, you are free to use all the resources as you need. In four weeks, we have a board meeting. A draft business case is also required.

Sure, it will be ready.

One last question for Stefan. Many of the board members are techies with limited financial background. Are there any additional arguments to persuade the board to pursue the opportunity?

Stefan paused for a moment before putting his idea on the line.

Well, it is just an intuition, but if you think about it, the WM industry is fundamentally about processing information. Yes, all sorts of different information, but information all the same. Yet, this is not how the industry is organized today.

Sassan Zaker joined Julius Baer Asset Management as head of alternative products. For the last 10 years, he has been an investment manager for UHNW individuals. The article reflects his personal investment views.

Appendix 1

Brief history of the pension fund operating system

With the rise of pension fund assets, a new principal-agent problem was in the making during the second half of the 20th century. How should pension fund trustees (the agents) manage the assets of the employees (the principals)? The original answer was simple enough: delegate the responsibility to investment managers. This model became problematic in the bear market of 1970s. The dispersion of investment manager performance was too high, and the performance of pension funds too random and subjective. To comply with their fiduciary duties, there was a need for objectivity. The financial theory at the time offered the simplest objectivity, suggesting average investing in the stock markets. In the aftermath, the PF software went through the following stages.

- Bear market 1970s, irritatingly wide and random manager dispersion. Enter MPT.

- Investment managers could now receive defined mandates. Enter benchmarking.

- Research indicated market performance (beta) dominates manager’s (alpha). Enter asset allocation.

- Active management (alpha) fails to add value. Enter indexing and passivation.

By 1990s, the PF operating system had already established itself within a well-defined regulatory framework, with a theoretical backing (MPT) and low-cost hardware (indexing and ETFs).

During this period, wealth management was undergoing its own strong growth, and facing similar fiduciary challenges and increasing scrutiny. Compared to the pension funds, there was no systematic structure underlying its processes. Absent its own methodology, wealth management gradually adopted the PF operating system.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All