The Fed is on a single-minded mission to fight inflation, according to Jim Bianco. To do that, it will crush stock prices and home values.

Bianco spoke virtually on May 6 at the Strategic Investment Conference, hosted by John Mauldin. Bianco is president and macro strategist at his own firm, Bianco Research, L.L.C., which is based in Chicago. Bianco spoke last year as well, when he correctly predicted that inflation would be non-transitory.

The Fed will continue to raise rates until inflation “really moderates,” he said. That means it needs to get back to the Fed’s target of 2% inflation. If the Fed stops raising rates short of reaching its target inflation, Bianco said it risks losing its credibility “for a generation.”

Indeed, it will be “really hard” to get to its 2% target, according to Bianco, and the Fed may have to increase the aggressiveness of its policies.

He spoke the day after the Dow had declined by more than 1,000 points.

“The Fed will create more indigestion than we have already seen,” he said.

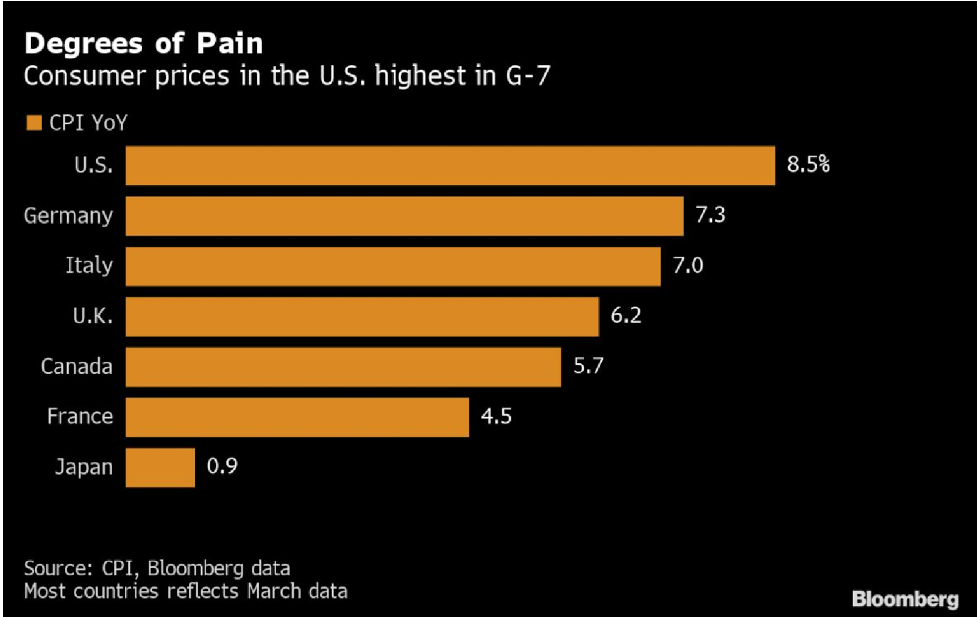

To understand why inflation is so high, Bianco showed that the U.S. has the highest rate in the developed world:

That is because, since 2019, the U.S. has pursued more stimulative policies than any other major economy. As a result, U.S. real disposable personal income is well above the OECD median.

Our extraordinary inflation is not due to the supply chain or the war in Ukraine, he said, which affects all other economies. It is zero interest rates, quantitative easing, and fiscal stimulus, all of which were done on a larger scale in the U.S. than elsewhere in the developed world.

Without fiscal stimulus, inflation in the U.S. would be 3% less than the 8.5% headline rate reported for March, according to a San Francisco Fed study that Bianco cited.

The U.S. GDP is approximately $20 trillion, he said. But in the last two years, the gains in the stock market were 70% to 90% of GDP (depending on the start date for that two-year period).

Those stimulative measures fueled a boom in housing and equity prices.

According to Zillow, as of March, the median home value was $338,000, and it increased over the prior 12 months by $58,000 or 20.9%. The median income in the U.S. is approximately $50,000. For homeowners, your house made you more money than your job did.

That has never happened, Bianco said, even during the peak housing boom year of 2006.

According to Redfin, the percentage of homes selling for more than their list price was 15%-20% before the pandemic. Now it is 55%.

“If 55% of homes are going above list,” he said, “real estate brokers don’t understand the market.”

The pain from rate hikes

Fed policies are designed to benefit the largest numbers of Americans.

Approximately 40% of Americans have less than $1,000 in savings and own no assets, such as a home. Those people are at “their breaking point,” Bianco said, because of inflation.

Only 3.5% of Americans are unemployed, he said, and that number rises to 6% if you add in spouses and families.

The Fed was “pleased” with the 1,000-point decline in the market, Bianco said, because it signaled that its policies will succeed in combating inflation.

But investors and economists are “having a terrible time getting their heads around this idea,” he said. Survey data shows that they are expecting fewer rate hikes than what is predicted by the futures market, which expects nine more 25 basis point hikes this year.

They don’t get the fact that inflation is the most important thing in the economy, Bianco said.

The strong jobs number (payrolls rose by 428,000 on the day he spoke) gives the Fed the signal to “hike like crazy,” Bianco said. Inflation is a far greater problem than unemployment.

Without inflation, he said the Fed would abandon its tightening. “But with it, they are just getting warmed up.”

About a third of Wall Street economists still think inflation is transitory, he said. They believe the Fed doesn’t have to do anything – just raise rates a few times – and the economy will achieve a soft landing. Two or three months ago, half of them believed that.

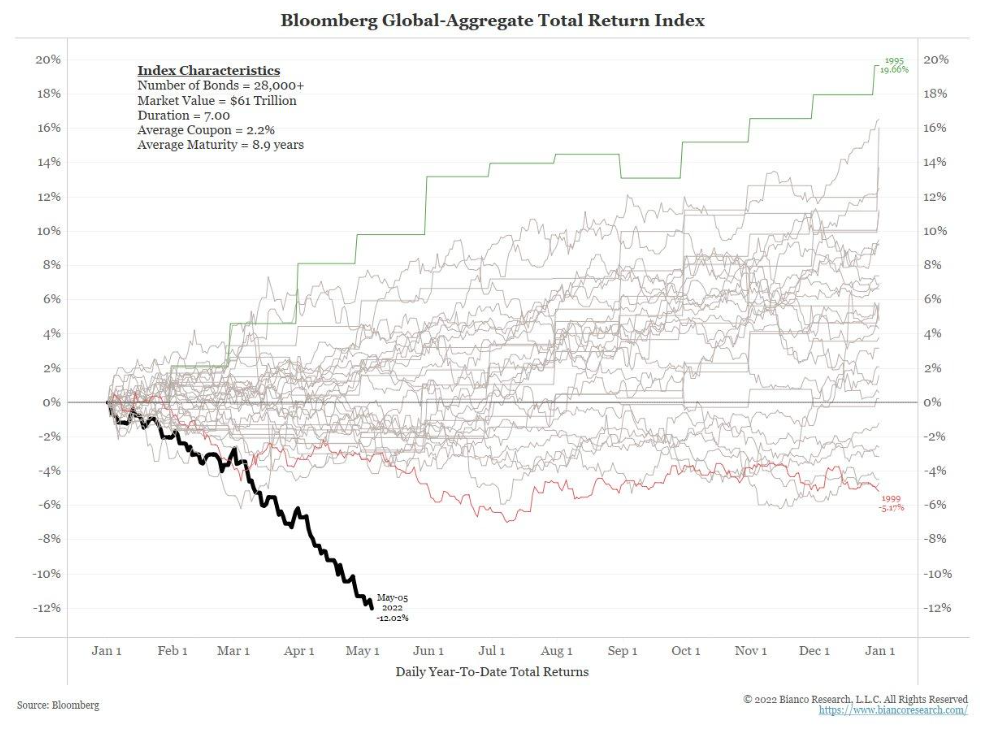

The precarious bond market

The bond market has declined by a historic amount:

The total return of the aggregate bond index (AGG) year-to-date is shown in the dark black line. The other lines show the total returns for the AGG for each of the prior 30 years.

Prior to 2022, the worst year was 1999, when the AGG had a total return of -5%. Its best year was 1995, when it rose 19%.

This year it is down 12%. April was the worst month ever for the bond market.

“We have seen nothing like this,” he said. “The bond market has never been this bad in terms of total return.”

He likened that decline to the S&P being down 50% to 60%.

There is “tremendous stress” in the bond market, he said. “There is going to be a problem,” but the bond market is too complex to say where it will eventually be.

This stress is because of a Fed error last year, he said, when it chose to use the word “transitory,” instead of dealing with inflation when it was only 3%. The Fed could have raised rates in the second half of 2021.

“Last year was the mistake,” he said. “This year is the consequence.”

Inflation is the number-one problem, Bianco said, and portfolio managers are struggling to understand this and are dismissing it. “Bonds are selling off to adjust to this reality,” he said.

In the last 80 years, every time inflation went down by 4%, there was a recession.

“The only way to get the inflation rate down that much is to keep markets under stress,” Bianco said. “The Fed will raise rates until inflation comes down or something breaks.”

Robert Huebscher is the founder and CEO of Advisor Perspectives.

Read more articles by Robert Huebscher