IRMAA – Who is She and How to Deal with Her

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

If there’s one thing that bugs people with higher income as they head into the Medicare system, it’s the income-related monthly adjusted amount (IRMAA). People at all income levels arrive into Medicare feeling that the system is “free” or “largely subsidized.”

They quickly learn that it is neither.

We’ll tackle IRMAA in this article. I’ll provide you with information to teach you how you might be able to get rid of IRMAA.

What is it? Approximately 7-8% of all Medicare beneficiaries are affected by IRMAA surcharges. This affects millions of people, and you or your clients may be among them.

IRMAA is not the same as a Medicare late-enrollment penalty. People often confuse the IRMAA surcharge with Medicare penalties. IRMAA is a surcharge (or a tax, if you’d prefer to look at it that way). It means that you, as a Medicare beneficiary, are paying a higher fee of your Medicare Part B premium than your neighbor may be. You will be paying that higher portion if you have more income than your neighbor.

Fair or not, that is how it works.

IRMAA is based on your modified adjusted gross income (MAGI) reported to the IRS from two years ago. If the IRS does not have MAGI information for you from two years ago on file, it may send MAGI information from three years ago to SSA to determine your IRMAA. MAGI combines adjusted gross income (AGI) plus tax-exempt interest income. When looking at the 2021 form 1040, you can find your AGI on line 11, and you can find your tax-exempt interest on line 2a (I am not a CPA, so please double check things with yours).

Don’t confuse income with net worth as some do. You may have $10 million in net worth but only $55,000 in income; if so, you will avoid paying IRMAA.

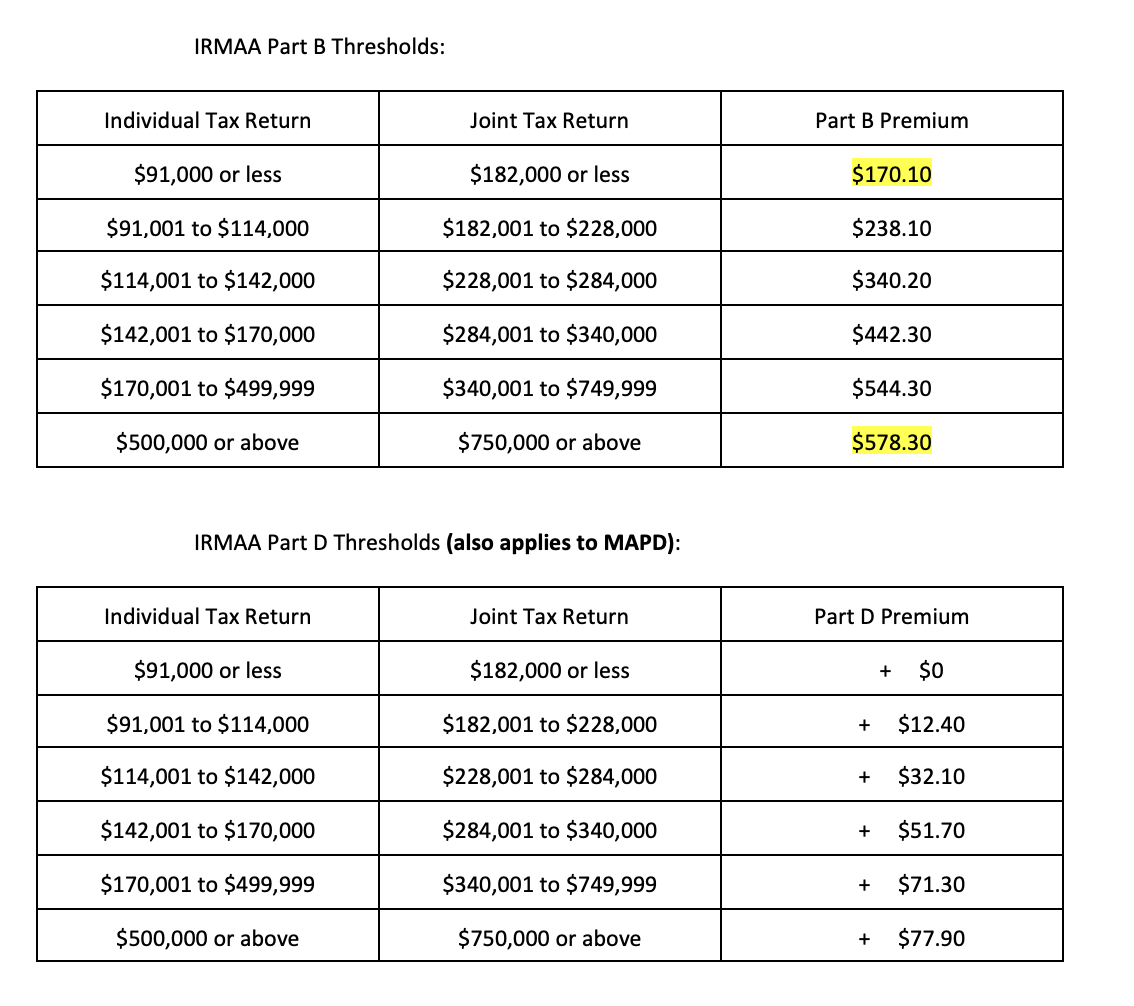

How do you figure out how much extra you will have to pay based on your income? Here are the official IRMAA thresholds for 2022. You’ll see that these are based on your tax filing status (I did not include the married but filing separately amounts, as I don’t see this very often. But contact me if you need that information). Find your MAGI from 2020 in these charts and on the right side you will see what you will be charged for your Medicare Part B premium.

Medicare sets a premium for a beneficiary annually. The people who are paying $170.10 per person per month are paying 25% of that Medicare Part B premium. The people who are paying $578.30 per person per month are paying 85% of that Part B premium. That’s how it works. If your income is higher, you’ll be paying a higher cost share amount (25% versus 85% with various levels in between).

These IRMAA charges are assessed on every person with the higher MAGIs. And, once you set up your Part A and B premiums with the government, you will then typically purchase a Medigap or a Medicare Advantage plan. Do not think that if you choose to enroll into a zero-premium per month Medicare Advantage plan that the IRMAA charges will no longer apply to you. For some reason, many people believe that enrolling into Medicare Advantage is a way to avoid IRMAA surcharges. It is not.

Let’s talk about how you will discover if you are going to be assessed the IRMAA charge. As you enroll into Medicare initially, you’ll receive a letter from the Social Security Administration with the message, “Welcome to Medicare, your premium will be $170.10.” You might think you skated by the IRMAA. A subsequent letter (it could be a few or 10 days later…) will essentially say, “Oh, we looked at your tax returns, and we now are telling you that you’ll pay XXX amount extra due to your high income in 2020.”

Now that you have confirmation that you’ll be assessed an IRMAA charge, I often hear from my clients, “Why do I have to pay more for Medicare if my income won’t be as high as it was two years ago?” Maybe you retired recently, right? Well, luckily there is a solution that I’ll discuss next.

The solution is to file this form, called the SS-44, with the Social Security Administration. You’ll be indicating to its offices that you have a lower income due to a “life-changing event.”

What are life-changing events?

- Work reduction or Work stoppage (MOST COMMON)

- Death of a spouse

- Marriage

- Divorce or Annulment

- Loss of income producing property

- Loss of employer pension

- Receipt of settlement payment from a current or former employer

On the form, select the life-changing event that you qualify for, which in our example of retirement is “work stoppage” and list the date the event occurred.

Next, in step two on the form, fill in the amount your income will be reduced to because of the life-changing event. For example, if your IRMAA is based on 2020 income since you are beginning Medicare in 2022, but your 2022 income is lower since you stopped working during the year, put your estimated 2022 income in this section.

You do not have to wait until filing taxes, since you can legally attest to your income using estimates. Be as accurate as possible, since SSA/Medicare will try to recoup what they were owed if your income ends up being higher.

You can also fill out step 3 on this form if your income for next year will be lower than the current year, or you can just leave step 3 blank.

IMPORTANT: IRMAA appeals happen individually. If you and a spouse are doing this, you will have to duplicate the process for both of you

After completing the rest of the form, the final step before submitting your request is gathering the evidence and documentation to show SSA that your income is lower due to a life-changing event (work stoppage in this case).

Some common examples that I recommend for proof of a work stoppage are:

- A signed letter from your employer showing your employment has ended;

- Copies of pay stubs showing work stoppage; or

- If you cannot provide direct evidence, SSA will accept your signed statement, under penalty of perjury on the form 44, that you partially or fully stopped working.

How do you get that SS-44 form to the Social Security Administration? The best way is in person. The SSA offices have recently, as of April 7, 2022, reopened to the public. You can also send a copy via certified mail (make a copy for yourself) or fax the documents to your local Social Security office. If you fax or send via certified mail, please make a follow-up call to that office to be sure that the documents were received.

Your request will be seen by an actual human being and not just a computer algorithm. Include as much information and evidence that you have available. However, do not overwhelm them with paperwork. If you sold your business and retired? Show a one-page document with proof of the sale. Do not send the 76-page legal documents of that sale.

After you file for a new initial determination, you will either receive a letter stating you have received a new initial determination based on your IRMAA lowering after your change in MAGI. Or you will receive a dismissal letter if your change in MAGI does not result in a change in IRMAA.

While waiting for the official word, realize that this can take some time. If you are being assessed with IRMAA now and have received bills to pay for your Medicare coverage, please pay those bills. Do not withhold the payment for the IRMAA even if you are confident that you’ll be successful in filing your SS-44.

Once you are indeed successful, your IRMAA paid in the past will be refunded to you. These premiums are part of your coverage and not paying them could result in the cancellation of your Medicare coverage (which is not good).

If you don’t file an appeal, you will get the adjusted IRMAA payments, but it will be lagged by two years.

In other words, the appeal means you get the immediate benefit of the life-changing event.

Finally, new IRMAA determinations will be made each year going forward. They will always look back to your MAGI from two years ago. Keep that in mind in case you didn’t know that you could indeed request a redetermination. If you did not know nor do that, things will flatten out if your new income each year is far less than your income a few years back. But you won’t get a refund of those premiums that were paid.

This is why I encourage you to know what those levels are and to work with your financial advisor to keep your MAGI within the proper levels. Think about items like the sale of a business or ROTH IRA conversions – lots of things can affect your MAGI from year to year.

Tune in to our latest Podcast episode where you’ll hear this entire discussion about IRMAA and what to do about it.

Good luck in your appeal!

Joanne Giardini-Russell is a Medicare Nerd & the owner of Giardini Medicare, helping people throughout Michigan and AZ, CA, FL, IL, IN, MI, MD, NC, OH, PA, SC, and TX transition to Medicare successfully. Contact the team at [email protected] or by calling 248-871-7756.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All