Ayn Rand’s followers dreamed of decentralized finance as the ultimate realization of their techno-anarchist utopia: freedom from both governments and large custodial organizations. But somewhere along the way, they got stuck on George Orwell’s Animal Farm where some animals are more equal than others.

Much of what passes as DeFi today is just “decentralization theater,” as Fabian Schar, a University of Basel professor of blockchain, describes it. In theory, this hot new crypto corner wasn’t envisioned to be controlled by big-bulge intermediaries. The self-executing computer code deciding how digital assets would be lent or invested was supposed to be impervious to manipulation. Developers weren’t expected to have special rights.

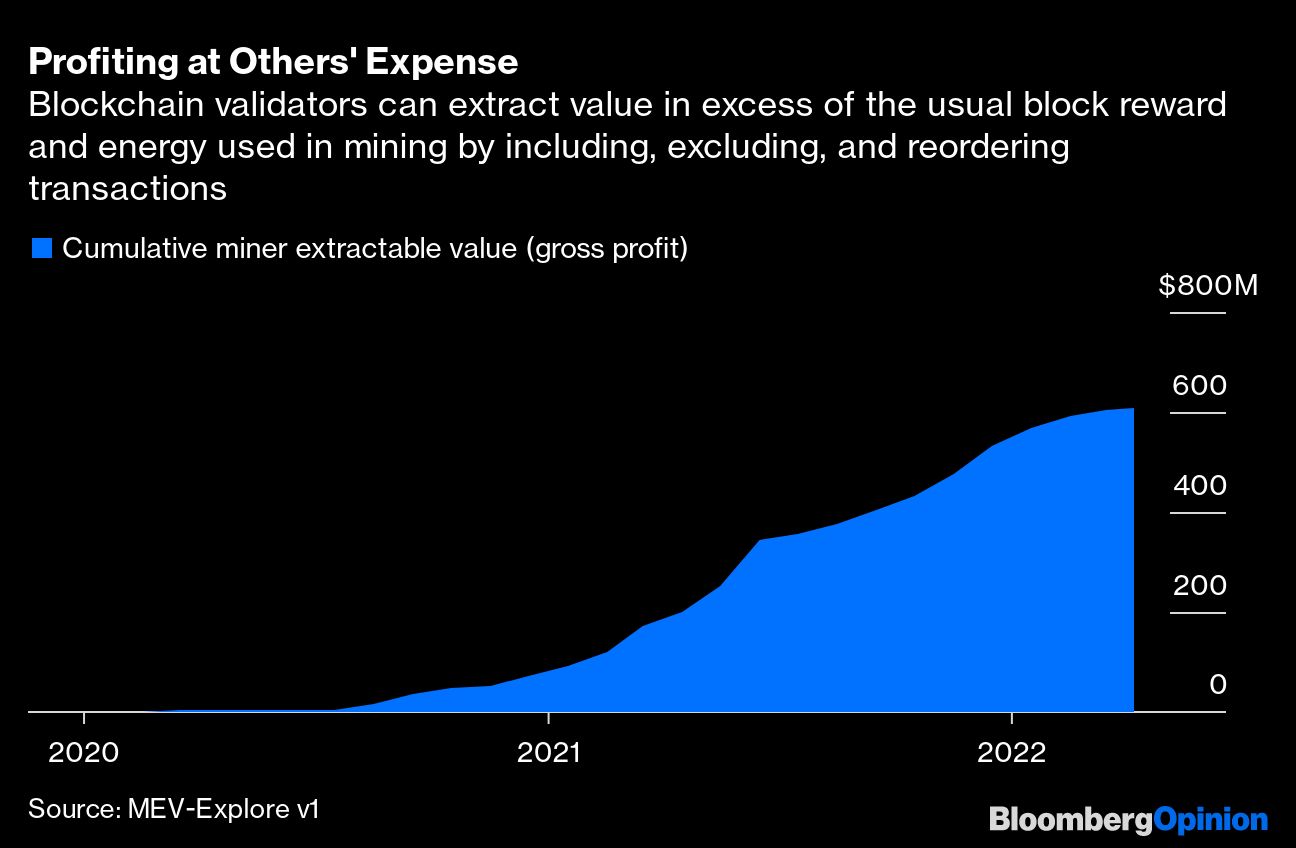

The reality has turned out to be different: From backdoors to kill switches, discretionary power is concentrated in a few players. You even have to pay for protection from “sandwich attacks” that place one transaction before and another after yours on the blockchain to steal your profit. The distributed ledger technology was supposed to leave all this Wall Street chicanery behind. But if a big chunk of DeFi has moved far away from its original vision, why not at least make it safe for all users by introducing the biggest centralizing force of conventional finance? The central bank.

Central bank digital currencies, or CBDCs, are in various stages of experimentation, partly as an answer to stablecoins. These private tokens peg their value to an official unit of account (such as the dollar), giving crypto investors a less volatile pathway than Bitcoin or Ether. Stable, however, doesn’t mean safe. To the extent stablecoins invest in risky assets, it’s natural for the Bank for International Settlements — the bank for central banks — to investigate if these tokens are really needed for DeFi liquidity. Letting people buy digital assets with CBDCs, which are direct claims on monetary authorities, will eliminate threats to financial stability from a stablecoin going bust.

“Does Safe DeFi Require CBDCs?” was the topic of a recent conference held in Zurich by the BIS and the Swiss National Bank. In his presentation, Schar answered the question with an emphatic “no.” DeFi relying on central banks would be a paradox. “It’s like asking, ‘Does safe decentralization need centralization?’” he said. But that doesn’t mean that monetary authorities can’t do some good. “Could a CBDC in a DeFi ecosystem be mutually beneficial? That’s a much more interesting question,” Schar said.

To play this part, though, central banks must be prepared to take their digital currency projects in a new direction: public blockchains.

The selling point of DeFi over conventional finance is the so-called composability feature. The computer code — the smart contract — can make an exchange of virtual assets and money part of one composite transaction, which takes place in its entirety or not at all. Counterparty risk goes away. As a result there is little role for regulated financial institutions acting as trustworthy middlemen.

But that’s only true of some protocols that are completely decentralized, transparent, and immutable, with no operators and special privileges, Schar said. In practice, much of DeFi isn’t like that. Assets of USDT, the most widely used stablecoin, are managed by Tether, its British Virgin Islands-based issuer, across a range of traditional options outside the blockchain. For an investor, a digital dollar issued directly by the Federal Reserve would be a much safer option than accepting a stablecoin that keeps its collateral in commercial paper, bank deposits, corporate bonds, secured loans and precious metals.

It’s a Catch-22, though. A CBDC running on a permissioned blockchain — where the central bank controls the access — can’t be included in a composite financial transaction taking place on a permission-less public blockchain such as Bitcoin or Ethereum. At the same time, it isn’t clear if any central bank is prepared to provide fully open access to its ledger, or if doing so is even aligned with the kind of transaction speeds, security and privacy that authorities will want from a network handling sovereign money.

DeFi’s linkages with traditional finance will grow, and not only because banks, brokers and asset managers will come under pressure to allow their Gen Z customers to pay, save, lend, borrow, trade, invest and insure in crypto. To Lex Sokolin, the global fintech co-head at ConsenSys, which analyzes DeFi projects and related risks, the real opportunity — and threat to a central bank’s relevance -- might lie elsewhere. “You have this web3 economy that’s generating actual operating activity that matters, and out of this grows a finance system,” Sokolin said on a panel at the same BIS conference. “How do we build a pathway of fiat money there?”

Left to itself, even the metaverse may not gravitate toward fully decentralized finance protocols. Meta Platforms Inc., the parent company of Facebook, is exploring a centrally controlled virtual currency for users to experience alternate reality, according to the Financial Times. Before Big Tech takes the lead, central banks have to start thinking about hawking their digital currencies in this brave new world — if they can first help DeFi get out of the animal farm.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.