Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In the world of investing, diversification is regarded as the only true free lunch. Market efficiency, an even more crucial free lunch, is routinely overlooked. But market efficiency is foundational in wealth management. It is not just the cornerstone of modern portfolio theory. It carries such far-reaching practical implications and significant ramifications if it fails.

Since market efficiency is the primary driver of the rise of passive investing and the demise of active management, the structure of wealth management investment offerings is at stake.

The efficient market hypothesis (EMH) postulates an idealized information efficiency of market prices. However, information efficiency is conditioned on the stability of investments. Markets generate consensus prices today, based on unknown cash flows in the near and distant future. While some of these forecasted cash flows are fact-based, others rely on faith and trust.

Market pricing is efficient and stable when it comes to factual (eigen) cash flows. When it comes to faith-based (fuzzy) cash flows, the market price mechanism becomes inefficient and unstable, and is only somewhat efficient for assets where eigen cash flows are mixed with fuzziness.

Market ability to transform subjectivity into objectivity

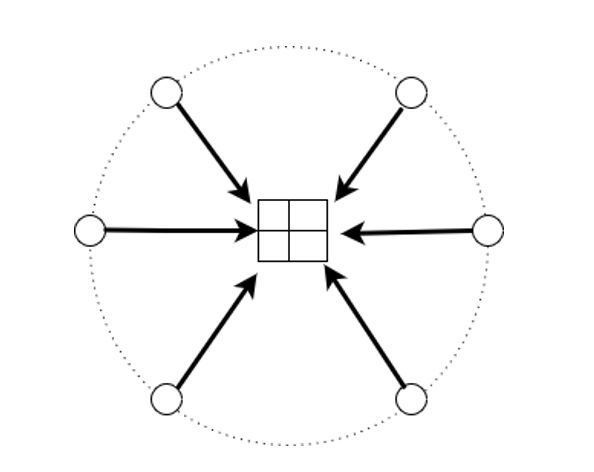

By considering all investors' pricing assessments, the market's invisible hand establishes a fair price. Investors participate in the market depending on their viewpoints, resulting in supply and demand equilibrium that balances markets. This is a two-step method that runs in a continuous loop. In the first step, individual investors form their subjective ideas on the reasonable price.

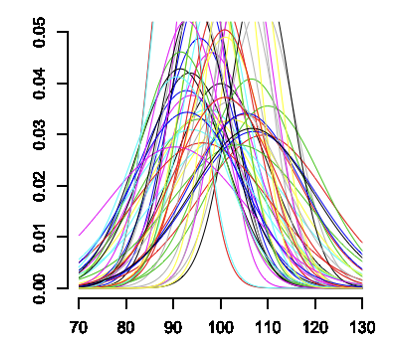

Exhibit 1 Subjective individual investor views as distributions of their fair asset price

Each investor’s individual view (each color) is represented by a Gaussian distribution. The market combines these to an aggregate Gaussian distribution (dashed black), which represents both observable market prices (the mean of the market Gaussian distribution) and its volatility (the standard deviation of the Gaussian distribution).

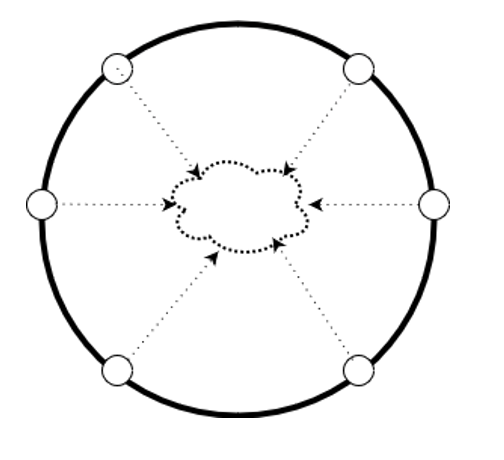

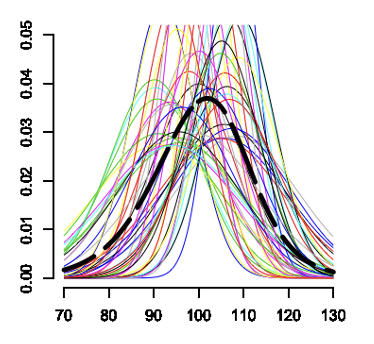

Exhibit 2 Subjective investor views (color) convert into an objective market price distribution (dashed black) in efficient markets

In this dynamic process, transparency and low market friction are critical components. Investors gain a valuable resource when the process operates smoothly because they may outsource the due diligence of their pricing to the market.

Another reason why market efficiency is so important is that it saves money. For investment communication, accountability, and governance, price objectivity is critical. The market's subjective-to-objective (S2O) process allows agents to act on behalf of principals, pension funds to properly report, and governance to be implemented.

Given the importance of market efficiency, it is worth considering when this process succeeds and when it fails.

When does market efficiency fail?

The market S2O process begins with investors ability to develop a view. When is this possible? When does it become difficult, and when does it become impossible? The investment universe has a wide range of predictability.

On one end of investment spectrum, e.g., U.S. Treasury bonds, investors face defined cash flows until the bonds mature. Not only are the cash flows stable, but they are also tangible and well understood. Investors may calculate the precise yield to maturity they can expect at the time of purchase, and that is exactly what they will get as long as the government does not default. Let us call factual, tangible, and consistent cash flows Eigen cash flows.

Exhibit 3 US Treasuries are defined sovereign Eigen cash flows

On the other end of the spectrum, contrast Eigen cash flows to the expected cash flows from a listed biotech startup corporation.

Exhibit 4 Biotech start-up as an example of Fuzzy cash flows

The majority of these cash flows are speculative, and if they exist at all, they will take years to materialize. The company will, as expected, go through a long period of needing financing while burning cash. As a result, there is a significant possibility the business will collapse. Let us name these investments, as well as the intangible cash flows they generate, Fuzzy.

Most listed assets, of course, represent a mix of eigen and fuzzy cash flows, and lie somewhere between those two extremes. For example, defensive stocks have a higher proportion of Eigen cash flows than high-growth stocks, whose future growth prospects may become fuzzy.

How can investors establish a view on fuzzy assets? They cannot. The investor’s view can only be very subjective and unstable. The market pricing mechanism becomes unreliable due to the underlying unstable subjectivity. The S2O process fails.

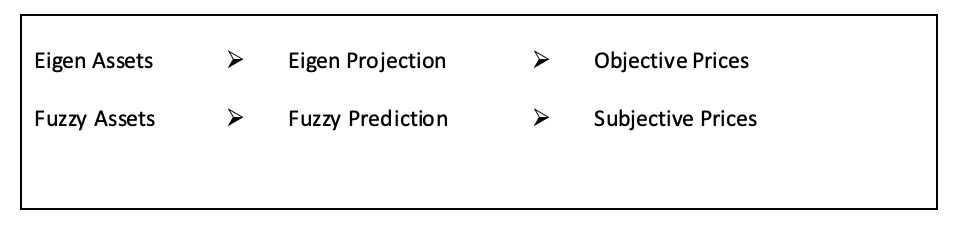

Eigen-projection versus fuzzy-prediction

Naturally, the methods used by investors to forecast eigen and fuzzy cash are vastly different. The modeling procedure for eigen cash flows focuses on the factors that affect cash flow variations and the appropriate discount factor. When the presence of cash flows is in doubt, the modeling becomes unreliable, as in the case of fuzzy assets. To put it another way, these two investor forecasting operations should be clearly distinguished.

Investors in Eigen assets can make projection forecasts utilizing models based on cash flow stability and predictability. Furthermore, investor models estimate similar price ranges due to the stability and visibility of the cash flows. As a result, Eigen assets are less susceptible to individual investor subjectivity.

Investors in fuzzy assets can generate only a predictive forecast because there is no solid basis for projecting. It is no wonder that fuzzy assets are irreducibly subjective when you consider the lack of visibility and stability.

Exhibit 5 Market participants can project eigen assets but only predict fuzzy assets

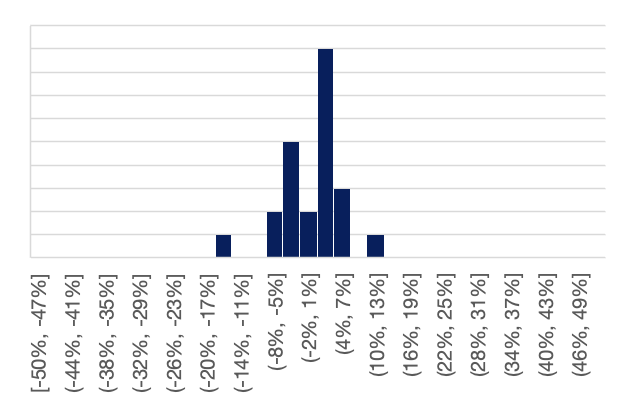

Exhibit 6 Example of Eigen-Projections

Full year 2021 S&P 500 EPS Wall Street Strategists forecasts

% Dispersion around mean ($172)

22 forecasts as of 20.1.2021 (source Bloomberg)

Investor interdependence

When it comes to the pricing of fuzzy and Eigen assets, what is the link and interdependence between investors? For Eigen assets, the objectivity of cash flows reduces investor interdependence.

Exhibit 7 Eigen assets: investors can ignore each other when pricing Eigen assets, sentiment has less impact on Eigen assets

In the case of fuzzy assets, the degree of interconnectedness is exceedingly high. Given the broad absence of factual investor confidence, perception and sentiment are vital game-theoretical inputs for all fuzzy investors.

Exhibit 8 Fuzzy assets: investors cannot ignore each other when pricing fuzzy assets. They are strongly entangled, sentiment can overwhelm fuzzy assets

Conclusion

The contrast between eigen and fuzzy assets explains market and investor behavior. The distinction made here focused on market efficiency. However, the methodological differentiation is beneficial to wealth management.

Because of their stability, eigen assets are the primary choice for strategic asset allocation (SAA). Fuzzy assets, strictly speaking, should not be included in the SAA. Tactical asset allocation should logically concentrate on these assets.

The market fuzzy-inefficiency presents opportunities for active management. In other words, the active-passive debate could be both unfruitful and misleading. Active management is not dead; it has just been suffering from chronic misallocation to the wrong part of markets.

Sassan Zaker joined Julius Baer Asset Management as head alternative products. For the last 10 years, he has been an investment manager for UHNW individuals. The article reflects his personal investment views.

Full year 2021 S&P 500 EPS Wall Street Strategists forecasts

Full year 2021 S&P 500 EPS Wall Street Strategists forecasts