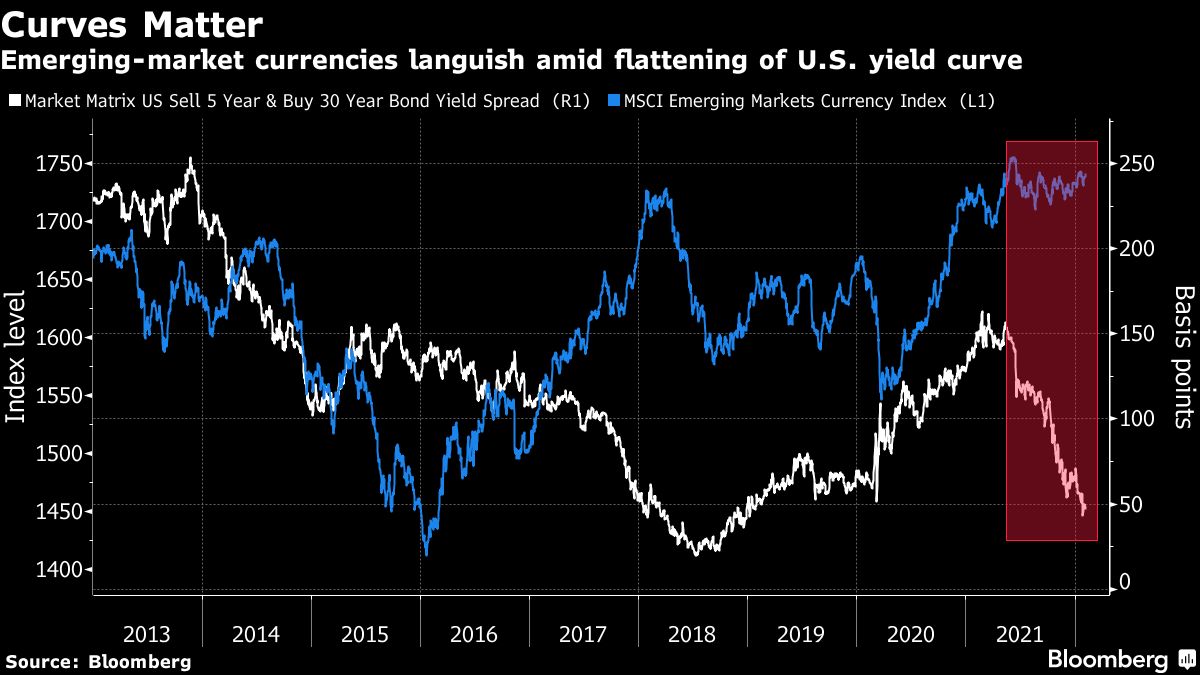

Emerging-market investors are waiting for an important signal from the U.S. bond market before piling into developing currencies: more yield-curve flattening.

Concerns that the Federal Reserve may overshoot with faster interest-rate hikes that could slow the economy have led to a flattening of the U.S. yield curve -- with shorter-dated yields rising at a faster pace. Fidelity International and Nordea Investment are waiting for the curve to turn almost completely flat before ramping up their wagers on emerging-market currencies.

The gap between the five-year and 30-year maturities has already narrowed to less than 50 basis points, its lowest in three years. Investors are betting that shorter-dated yields will get even closer to levels at the long end before the market stabilizes. Any inversion of the curve has historically been seen as a recession signal.

“In order to trigger renewed bullishness on EM FX, we need to see clear signs that the Fed successfully manages a soft landing,” said Witold Bahrke, a Copenhagen-based senior macro strategist at Nordea Investment. “But as the relentless U.S. yield curve flattening is highlighting, the risk of the opposite is still creeping higher.”

The U.S. yield curve is likely to bottom “around peak Fed hawkishness,” Bahrke said. That will probably be followed by a bull-steepening move in which Treasuries will rally, with shorter-dated securities gaining the most, pushing down their yields more than those at the long end, he said.

For now, Bahrke is seeking to resume a short position in emerging-market currencies after taking some profit on his bearish wagers in December. He’s negative on China’s yuan, due to its central bank’s dovish stance while other policy makers hike interest rates.

Traders are being confronted with other risks too, including rising fears that Russia could invade Ukraine, slowing global growth and persistent price pressures. The Russian ruble is one of the world’s worst performers this year.

Still, emerging-market currencies have mostly outperformed their developed peers this year, with the Brazilian real, Hungarian forint and Chilean peso up more than 4% against the dollar. They’ve been backed by central banks that led the charge in rate hikes in 2021, providing a buffer against higher U.S. rates.

“This is not the world of outright risk aversion,” said Emily Weis, a macro strategist at State Street in Boston. “EM FX has been unloved for a while based on price action, suggesting that investors may not be as over their skis in EM risk compared to other areas like tech.”

Seven Hikes?

The light positioning in emerging assets following last year’s selloff provides a “small window of opportunity” for developing currencies, said Ed Al-Hussainy, a senior interest-rate strategist at Columbia Threadneedle Investments in New York.

“The biggest risk is that the Fed accelerates the tightening cycle and we see a broader deterioration in risk assets globally,” he said. “EM FX is very sensitive to risk-off liquidity outflows and will see significant downside in this scenario.”

Strong U.S. data could prompt investors to price in rate hikes of 25 basis points at each of the seven remaining Fed meetings in 2022 and eschew shorter-dated bonds, said Fidelity International’s Paul Greer. At that point, the U.S. yield curve will be “very close to completely flat” between the five- and 30-year maturities, said the London-based money manager.

“For us to get more comfortable with emerging-market currencies, we would need to see some stability in front-end U.S. yields, some further clarity from the Fed on their expected pace of policy tightening this year as well as some improvement on the EM growth outlook,” Greer said, adding that his fund is underweight developing currencies.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Netty Ismail