The 10 Toughest Client Objections to Overcome

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits I make it clear to prospects that they shouldn’t hire me if they want an endorsement of their current strategy. In fact, I often tell them it will likely be the opposite as I am the most argumentative person on the planet. Going in, they know they are working with “argumentative Al,” and I don’t disappoint.

I make it clear to prospects that they shouldn’t hire me if they want an endorsement of their current strategy. In fact, I often tell them it will likely be the opposite as I am the most argumentative person on the planet. Going in, they know they are working with “argumentative Al,” and I don’t disappoint.

But my rationale is to get clients to take actions to build a more secure future.

Often, my clients push back on the direction I recommend. I point out that this isn’t a negotiation – this is their money that they worked hard to earn and I’m just the advisor.

Here is how I nudge clients (sometimes not so gently) to where they should be on their portfolio:

1. I’m comfortable with my (heavy) stock allocation. It’s as predictable as the rising sun. When stocks have plunged, the client wants very little risk. But during our current raging bull, they think they are very risk tolerant.

I note that dying the richest person in the planet is a lousy goal and explain why recency bias may be driving how they feel about risk. I use a practical version of Danial Kahneman’s prospect theory. Rather than ask how they would feel if they lost half of their net worth, I translate into consequences and ask questions like, “How would you feel if…”:

-

- you couldn’t send your child to that prestigious college they worked so hard to be accepted at?

- you couldn’t buy that dream house on the lake you always wanted in retirement?

- you had to sell your house and downsize?

Typically, this does the trick. But sometimes I tell the client I’m going back on my word to avoid negotiation. Say the client wants 70% equities and I think 60% is more appropriate. I respond, “Let’s start with the 60% I think is appropriate. But, when stocks are down by more than 20%, you can go to the 70% you want.” I’m not timing the market – rather I’m testing the client’s resolve. I let them know that not a single client opted for the higher stock allocation when the bear arrives; the appetite for greater risk is suddenly gone.

2. I want income-oriented investments. I tell them that wanting this is only natural and that I do too. All my clients were programmed to save and it’s only natural that the thought of spending down principal is scary. They want things like dividend stocks, private REITs, and master limited partnerships. But I point out that income is the wrong goal.

I start with the obvious – total return is more important than income – and note that dividend stocks have underperformed compared to growth. I give some examples of people who had to go back to work because they built an income portfolio but lost much of their principal. When they state they want “safe” large-cap dividend stocks I ask, “You mean like Eastman Kodak or GM?” I also give them the more recent example of GE.

Sometimes, I suggest that they can build their own income portfolio by owning much lower cost and diversified total stock index funds and do so in a more tax-efficient manner by understanding stock buybacks.

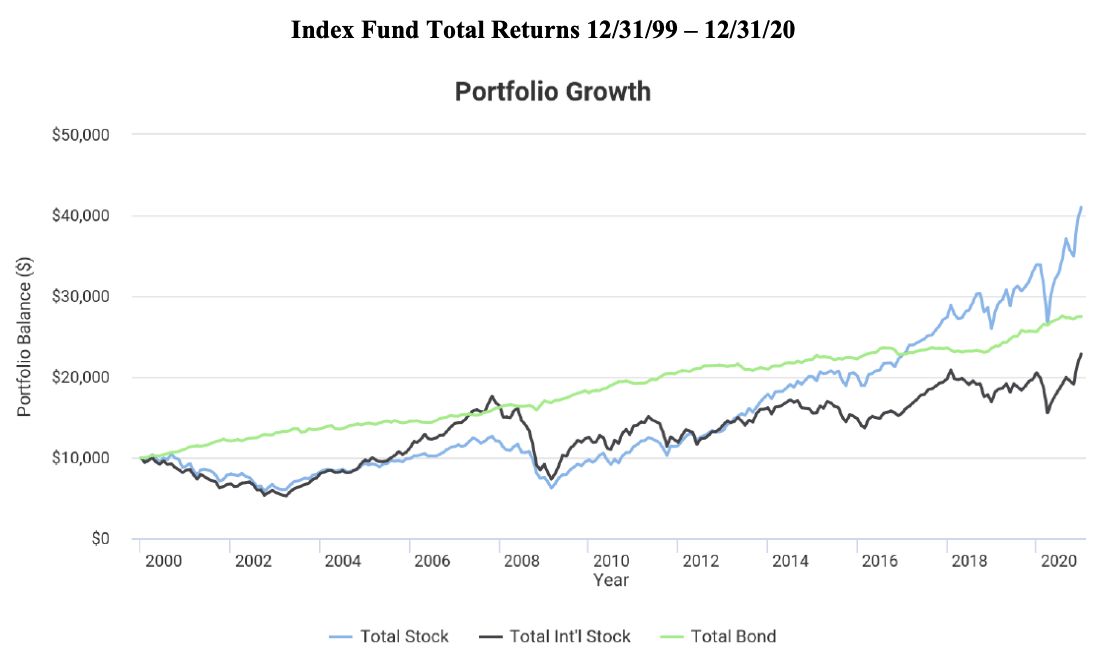

3. I don’t want too much allocated to international stocks. I often hear that many problems exist overseas and it’s not the place to invest. It’s understandable after such under performance as in the graph below. But back in 2007, I heard just the opposite as international soundly bested the U.S.

Capitalism should work everywhere. I don’t only buy stocks in my home state and tell the client not to invest only in their home state. We have plenty of problems in the U.S. and are printing money faster than most other countries. I want diversification. Finally, for those clients from the last concern who want high dividends, I point out that The Vanguard Total International Index Fund ETF (VXUS) is yielding 2.57% vs. the U.S. Stock Index Fund (VTI) yielding 1.21%. And both Fidelity and Vanguard have their fund of funds at 40% international in their stock allocation. I typically recommend a one-third allocation, which is above what John Bogle recommended (typically between zero and 20%).

Capitalism should work everywhere. I don’t only buy stocks in my home state and tell the client not to invest only in their home state. We have plenty of problems in the U.S. and are printing money faster than most other countries. I want diversification. Finally, for those clients from the last concern who want high dividends, I point out that The Vanguard Total International Index Fund ETF (VXUS) is yielding 2.57% vs. the U.S. Stock Index Fund (VTI) yielding 1.21%. And both Fidelity and Vanguard have their fund of funds at 40% international in their stock allocation. I typically recommend a one-third allocation, which is above what John Bogle recommended (typically between zero and 20%).

4. I know this is an expensive fund, but I don’t want to sell and pay the capital gains tax. I don’t like paying taxes either. Tax-efficiency is a key goal in portfolio construction. But I use some math to show the breakeven in expected return and note the increased tax-efficiency going forward. That expensive fund is typically passing through realized gains (1099) and I tell them they will have the worst of both worlds – lower returns and a slow bleed with taxes year after year. I point out that their mutual fund may be in a death spiral, in that investors yank money out of underperforming funds passing through capital gains as they have to sell securities to meet redemptions. That turns into a quick bleed out so it may be better to rip the bandage off.

5. I want alternative investments. Often the client wants investments that zig when the market zags. They want private equity, managed futures, reinsurance-risk funds or other assets such as bitcoin ETFs. I tell them that low correlation is only one of the two criteria – a reasonable expected return is also required.

Not a penny has ever been made in the aggregate futures market before costs. It’s better to be a private-equity general partner than a limited partner as some general partners have told me there is too much money chasing too few deals. And all these alternatives have fees many times that of low-cost strategies.

6. I don’t want bonds because rates are too low. I advise the client to “get real” and state that real after-tax rates have been far lower. I note that in 1981, one could earn 12% on a CD or high-quality bond, but after a third went to taxes the 8% return was about five percentage points behind inflation. The portfolio lost spending power.

Admittedly, this argument is losing some validity with the recent high inflation. Still, the purpose of the portfolio is to support one’s lifestyle. High-quality bonds act both as a shock-absorber when stocks plunge and allow rebalancing to buy more stocks when they are on sale.

7. Okay, but I want high yield bonds so I can at least beat inflation and I want to stay short because interest rates will rise. My instinct is to completely agree, but I know instincts are usually wrong when it comes to investing.

Why shouldn’t the client achieve both goals? For example, the Goldman Sachs High Yield Floating Rate Fund (GSFRX) is yielding 3.26% as of November 30, 2021, and has a duration of 0.26 years. Why would anyone buy something like the Vanguard Total Bond Fund (BND), yielding a paltry 1.59% with a 6.8 year duration? The argument goes, as interest rates continue to rise due to Fed actions, BND will get clobbered while the yield on GSFRX will surge.

I tell clients that credit quality is the most important factor in a bond. GSFRX has an average B credit quality while BND is AA. Investors have short memories, and the word “junk” is one of the few Wall Street terms that properly describe the security. I show the client how junk typically gets hammered when stocks plunge, while higher credit quality typically acts as the shock absorber to allow rebalancing.

Though rates have increased a bit this year, don’t be sure rates will continue to rise. The top economists have a dismal record of calling even the direction of the ten-year Treasury bond correctly. Japan has been printing money for decades and fighting deflation. The bond market is still saying the recent high inflation is transitory as rates are still very low. In due course we will know.

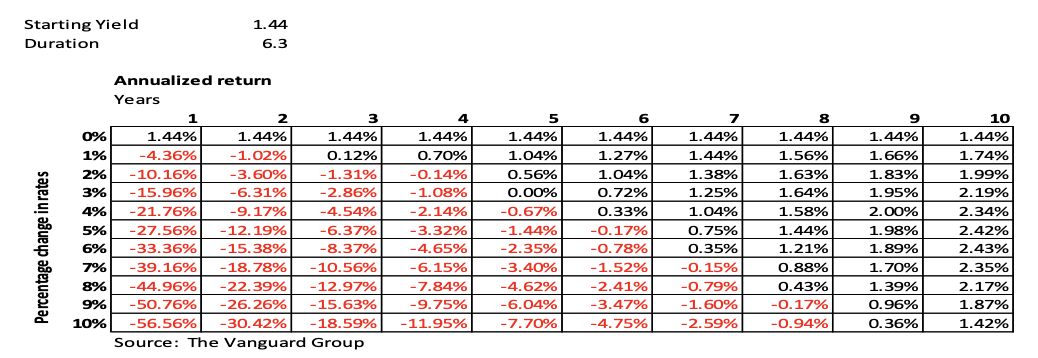

If rates do rise, there is a silver lining: while the value of the bond drops, the yield increases. I show the client the following chart. Using an example of a bond fund with a 1.44% yield and a 6.3-year duration, a two-percentage point increase in rates would cause an estimated 10.16% decline in value over one year. If rates then stabilized, as the underlying bonds matured, new bonds would be purchased yielding 3.44%. By year five, the client is back to breakeven and by year eight, they have earned more than had rates not risen in the first place, causing that 10.16% loss. That helps convince clients to take on a moderate amount of interest rate risk.

8. I don’t want to pay off my mortgage as my overall portfolio should beat my low 3.25% mortgage rate. Very few advisors have the incentive to tell clients to pay off their mortgage. I point out that the mortgage is a negative bond, and it typically doesn’t make sense to lend money out at 1.59% (BND) while borrowing at 3.25%. Furthermore, most people are getting little or no tax-deduction from their mortgage (because they don’t itemize deductions or because much of the interest expense only gets them to the standard deduction) while they are paying taxes on all BND interest. It’s a risk-free and often tax-free 3.25% return.

8. I don’t want to pay off my mortgage as my overall portfolio should beat my low 3.25% mortgage rate. Very few advisors have the incentive to tell clients to pay off their mortgage. I point out that the mortgage is a negative bond, and it typically doesn’t make sense to lend money out at 1.59% (BND) while borrowing at 3.25%. Furthermore, most people are getting little or no tax-deduction from their mortgage (because they don’t itemize deductions or because much of the interest expense only gets them to the standard deduction) while they are paying taxes on all BND interest. It’s a risk-free and often tax-free 3.25% return.

I advise clients that the only reason to borrow money at a higher rate than that for which they lend it out in their taxable account is liquidity – to be able to sleep at night.

9. I don’t want to do a Roth conversion, as paying taxes lowers my net worth. This can be the response when I discuss partial Roth conversions. The purpose, of course, is to get some tax-diversification as we never know what future tax rates will be.

I acknowledge the math that if the client converts $10,000 of a traditional IRA to a Roth and is in the 30% marginal bracket, they pay $3,000 in taxes. But then I note that the traditional IRA is only 70% owned by the client and all they are doing is buying out the state and federal governments’ share.

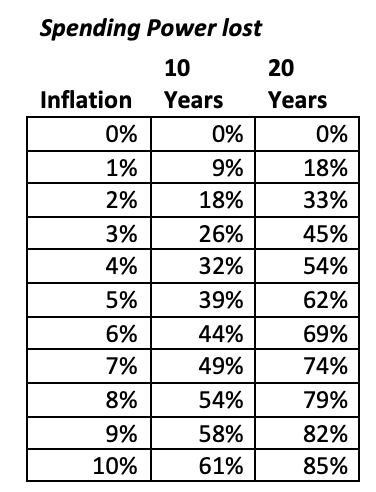

10. I need $500,000 cash to feel safe and it’s okay earning nothing. Though we generally think of cash as a riskless asset, I tell clients the story of the frog in boiling water. They say (and I’ve never checked to see if it was true) that if you put a frog in boiling water, it jumps right out. But if you put the frog in pot of comfortable room temperature water and slowly heat it up, it doesn’t notice the change in environment and boils to death. Cash can be cozy yet, over time, destroys spending power.

I show them this chart on how much spending power they will lose over time:

I then show them online FDIC-insured savings accounts earning 0.5% to 1.0% where the cash is working harder, as well as Treasury-issued “I” bonds. If they say the rate is too low, I help them reframe the decision. I ask something like, “Can I buy a half hour of your time for $2,500?” I get a “yes” and they understand that I’m noting they can earn this much more if they at least have the cash working as hard as a short-term bond.

I’m generally successful with my arguments, but not with every client. When I’m not, I tell them they must stick to the decision. For example, if they want that heavy stock allocation, they must stick with it and buy more to rebalance when stocks tank. Often, consistency is more important than getting things right in the first place.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion dollar companies and has consulted with many others while at McKinsey & Company.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All