Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Two of the biggest risks retirees face are from longevity and the market. It is the job of their financial advisor to help mitigate those risks through strategies such as diversification. It has long been considered an advisor’s fiduciary responsibility to engage in the practices of asset allocation and portfolio diversification, first introduced by Harry Markowitz in his 1952 essay “Modern Portfolio Theory.”

However, a new study, which I co-authored, proves that a withdrawal strategy utilizing a reverse mortgage reduces market risk and increases portfolio growth. The study, published in the Journal of Financial Planning, reported that this strategy benefit mass-affluent investors.

The study focuses on 20 million retirees in the United States who are part of the baby boomer generation and have their primary source of retirement income from 401(k) accounts or other securities portfolios with values in the range of $500,000 and $1.5 million, and who own their home and have little or no mortgage debt against it.

The study (To Reduce the Risk of Retirement Portfolio Exhaustion: Include Home Equity as a Non-Correlated Asset in the Portfolio) reported that volatility is a risk for retirees:

For clients who are in mid-career and are building wealth (i.e., not distributing from their portfolios), short-term volatility generally does not present a significant risk. By contrast, for clients who are retired and are distributing primarily from a securities portfolio for their normal living expenses, short term volatility is risk.

The impact of a bad market year reduces the size of a retiree’s portfolio and their income, assuming they are not increasing their withdrawal rate to compensate, which would exacerbate the problem.

The risk is the retiree’s exposure to volatility and the impact on their cashflow (portfolio income). Given that cashflow equals retirement lifestyle, this is the real reason a wealth management client has a risk tolerance in the first place. We tend to look at risk purely as a client’s tolerance for investment losses, but, ultimately, it is the potential impact those losses have on the retirement lifestyle that they are really concerned about.

A 2010 Allianz study famously stated, “61% of the respondents said they were more scared of outliving their assets than they were of dying.” Fortunately, a withdrawal strategy with a reverse mortgage as a buffer asset can both reduce the risk of running out of money in retirement and increase gains.

A reverse mortgage as a buffer asset

How does this withdrawal strategy work? At the end of each year, determine if the client’s portfolio increased or decreased. If the portfolio is up, take the next annual draw from the portfolio. However, following a down year, skip the annual draw from the portfolio and draw instead from a buffer asset. The idea is to leave as much as possible in the portfolio to benefit from the eventual rebound. In the case of required minimum distributions (RMDs), establish another account to deposit the RMD with the same investment mix. There can be some minor tax consequences, but you accomplish the goal of staying invested to benefit from the market rebound.

The buffer asset is the cheapest alternative income source available to the client. Some clients have alternative income streams from real estate investments or royalty income from published works. Still, for a majority of the mass affluent, the easiest source is tapping into their home equity via a reverse mortgage. Since the proceeds of a reverse mortgage are not taxable, it is likely the cheapest alternative income source for most clients. Another benefit is there is no required monthly repayment, making it a cashflow positive financial tool. This represents a paradigm shift – no longer is all debt bad in retirement.

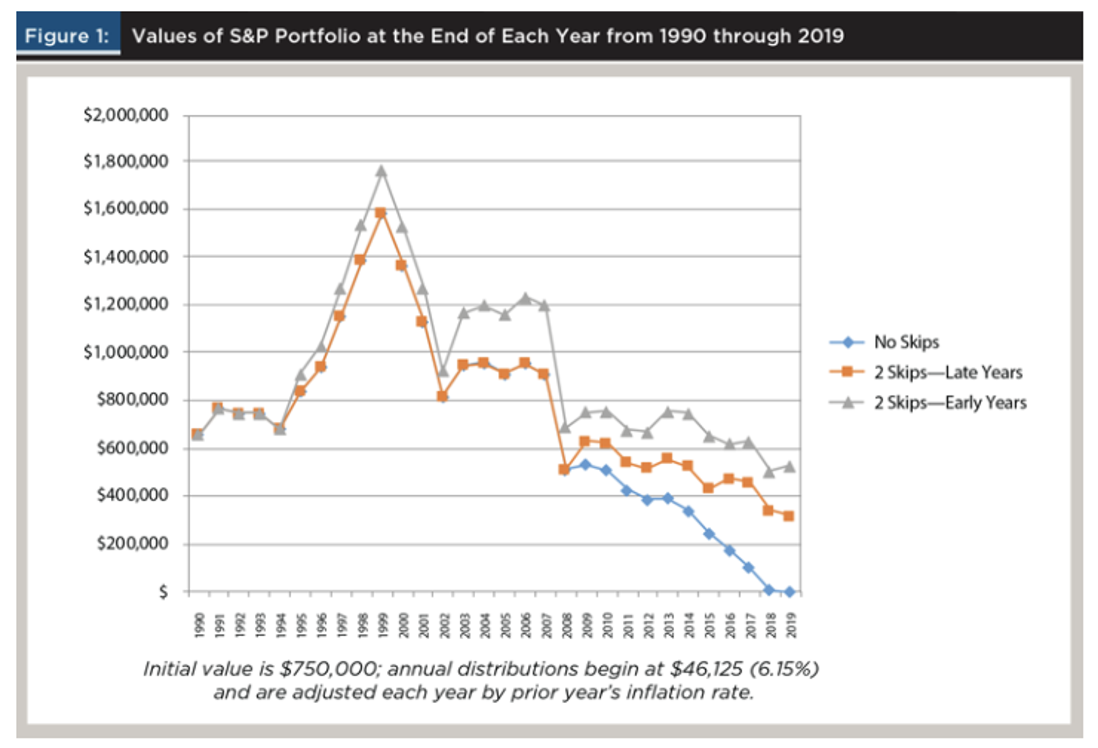

Below is a graph from the study, which demonstrates the power of skipping just two draws in retirement. The blue line shows what happens with no skips, and the portfolio is exhausted prior to life expectancy. The red line shows two draws skipped late in retirement and demonstrates a substantial improvement. The green line is two draws taken early in retirement and has the best outcome. The typical client will experience four down-market years in retirement.

Reverse mortgages are designed with the mass affluent in mind and most misconceptions are a reaction to products that no longer exist.

When it comes to extending the life and growth of a portfolio of securities, this strategy has nearly a 95% success rate, which was determined after 10,000 Monte Carlo simulations in a prior study. The impact on portfolio growth can best be summarized by directly quoting the study:

Thus, using as the growth rate an estimate of the current rate of interest applicable to a reverse mortgage, it is reasonable to estimate that the retiree who takes advantage of the “distribution-skipping” strategy explored in this example would have cash flow throughout a 30-year retirement and a legacy substantially greater than a retiree who does not take advantage of such a strategy.

The risk reduction identified in this new study is one of the most significant findings since the introduction of modern portfolio theory in 1952. This coordinated withdrawal strategy reduces the retiree’s exposure to volatile markets by nearly 10 times. The study states that this change in risk is very significant and has fiduciary implications for advisors and their firms. Factor in the trend of a more positive correlation between stocks and bonds, versus the historical negative correlation (See Bloomberg 7/9/21), and the need to offset retirement plan risk becomes even greater.

The study also revealed that debt can be beneficial to retirees when used in this way. There is not often a breakthrough in the financial planning world, and this peer-reviewed study has unveiled that it has happened.

Phil Walker is the vice president of Strategic Partnerships for the Retirement Strategies Division of reverse mortgage lender Finance of America Reverse LLC, and the lead author of the aforementioned study, along with co-authors Barry Sacks J.D., Ph.D., and Stephen Sacks, Ph.D. The views expressed in this article are those of the author alone and do not necessarily reflect the views and opinions of his employer. This article is intended for financial professional use only, and is not intended to provide tax advice. For tax advice, consult a tax professional. Additional resources for financial professionals are available at www.HomeEquityU.com.

Read more articles by Phil Walker

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives. Reverse mortgages are designed with the mass affluent in mind and most misconceptions are a reaction to products that no longer exist.

Reverse mortgages are designed with the mass affluent in mind and most misconceptions are a reaction to products that no longer exist.