Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

For life settlements, open-ended funds offer more liquidity than closed-end funds. But they also have lower returns and the management and performance fees are often based on the net asset value of the fund – which can be hard to accurately assess for assets with unlevel cashflows.

As RIAs look to alternative assets to provide portfolio diversification in a high-P/E-ratio and low-bond-yield environment, they are increasingly looking for alternative investments like life settlements that have low correlations to equity market and interest rate risk.

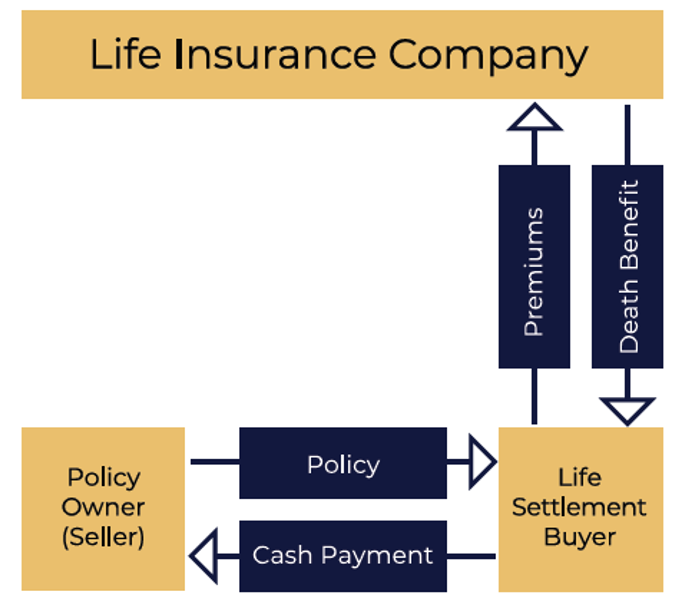

A life settlement is the sale of an in-force life insurance policy by the original policy owner to a third party. In return for providing the seller with a cash payment, the third-party purchaser (investor) owns the life policy, pays all the premiums going forward and eventually receives the entire death benefit at the time of the insured’s passing.

Life settlement transaction

The transaction is a win for the seller and the buyer. The seller receives more for selling the policy to the buyer than they would get if they cancelled the policy. The buyer is a sophisticated investment company that knows that aging insureds on life insurance policies are more likely to be less healthy now than when the policy was purchased. By pooling policies together, the buyer gets an uncorrelated and diversified investment portfolio.

However, most life settlement funds sold to RIAs and family offices are available only through open-ended structures that compromise the underlying cashflows; the cashflows are negative or low in the early years and highly positive in the later years. This irregularity makes it difficult to accurately value the underlying future cash flow stream and results in high bid/ask spreads for the assets. This is particularly true of funds with a small number of policies. The smaller the number of policies in the fund, the more difficult it is to accurately value the future cashflows.The transaction is a win for the seller and the buyer. The seller receives more for selling the policy to the buyer than they would get if they cancelled the policy. The buyer is a sophisticated investment company that knows that aging insureds on life insurance policies are more likely to be less healthy now than when the policy was purchased. By pooling policies together, the buyer gets an uncorrelated and diversified investment portfolio.

There are currently no publicly traded funds that invest exclusively in life settlements. There are a few publicly traded funds that have a small portion of their capital (<10%) to life settlements. The life settlement space is largely ruled by private funds that operate under the Reg D exemption and raise funds exclusively from accredited investors and not public markets. These funds are either open- or closed-ended. The open-ended life settlement fund presents these key problems for investors:

1. A life settlement investment takes a few years to generate positive cashflows

The early-year returns of a new fund are low. Since it takes a few years for a new life settlement portfolio to yield positive cashflows, a fund that continues to purchase new policies every year essentially restarts the low-yield part of the investment process. This hurts investors who want to exit early unless the fund inflates the value of the underlying assets to boost returns.

2. Open-ended funds can hide the low early-year returns mentioned above by booking the policy at the ask price instead of the bid price in order to show high unrealized returns.

As long as the fund keeps buying new policies, it can continue to show high unrealized paper returns by repeating this process while having low actual realized returns.

3. If an investor exits the fund before cashflows turn positive, then they would only earn the low early-year fund returns

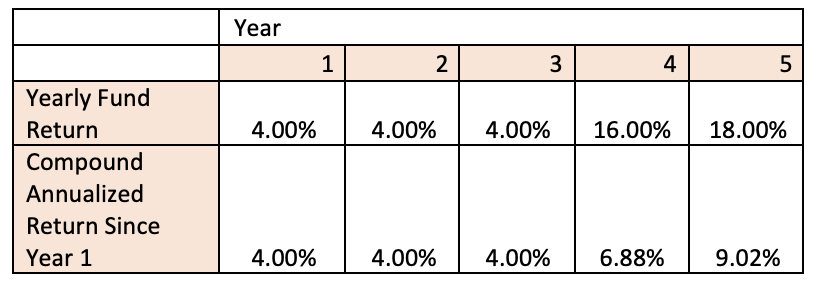

That is true unless the fund has overvalued its assets, in which case the low early-year fund returns would be passed on to investors who exit later. To make matters worse, any new investor who gets lucky and invests in an open-ended life settlement fund just before the large positive cashflows materialize will experience great returns that would have otherwise gone to the investors who had been there since the beginning, as illustrated in the table below.

Hypothetical open-ended fund with unlevel yearly asset returns

As the above table shows, an investor expecting to earn a 9% compound annual return would need to stay for the entire five-year period since the returns are low in the early years and high in the later years. If the investors exit before year four, they earn only a 4% compound annual return.

An open-ended fund with low early-year returns and high later-year returns benefits later investors who invest just before the large cashflows materialize at the expense of those who invested from the beginning. New investors that come in only during the later years essentially dilute the original investors’ equity. Furthermore, if the fund continues to buy new life-settlement assets with the capital they raised from new investors, the fund is essentially restarting the “low-return” part of the investment profile. This lowers short-term returns for all investors in the fund. The longer the fund continues to buy new assets, the longer they delay the “high-return” part of the return profile.

This is why asset classes with unlevel cashflows are better suited to closed-end funds, where investors have a longer time horizon and can wait for the cashflows to materialize as opposed to open-ended funds that need to provide liquidity for investors. Investors who exit early will miss out on the high cashflows in the later years.

While an open-ended fund offers better liquidity for those wanting early exit options, there’s a premium paid for this in the form of lower returns. A fund that faces redemption requests needs to hold a larger cash reserve to meet those requests or must use leverage. Furthermore, if large numbers of investors choose to redeem, an open-ended fund has to sell assets to meet those redemptions. This can significantly hurt returns if the asset has a large bid/ask spread.

Consider an asset that has a bid of 90 and an ask of 100. Imagine the fund is valuing those assets on its book at the $100 ask price because it expects to keep the asset for the long term. Let’s assume the fund receives a redemption request for $100 and has to sell assets to meet the redemption request. It can’t simply sell $100 of assets to meet the cash redemption, because the bid price is $90. To meet the $100 cash redemption by selling assets at the bid price it has to sell assets worth $111.11 on its books ($100 cash redemption = $111.11 of booked assets X $90 bid price/$100 ask price). This sell-off of assets hurts the investors who are staying due to the loss of value.

Open-ended funds that invest in assets with large bid/ask spreads must either hold large cash reserves to meet these redemption requests or sell assets at below the value on their books, either of which drags down returns. These funds could also book the assets at lower values to reduce this liquidation problem, but that would result in the fund showing lower returns to their investors.

A more nefarious problem arises when the value of the assets being held on the books is subjective and can be manipulated. Consider an open-ended fund which values its assets based on third-party reports. If the fund uses third-party providers or practices that allow it to inflate the value of the asset greater than what buyers are willing to pay for it, then the fund can show great paper returns every time it purchases new assets.

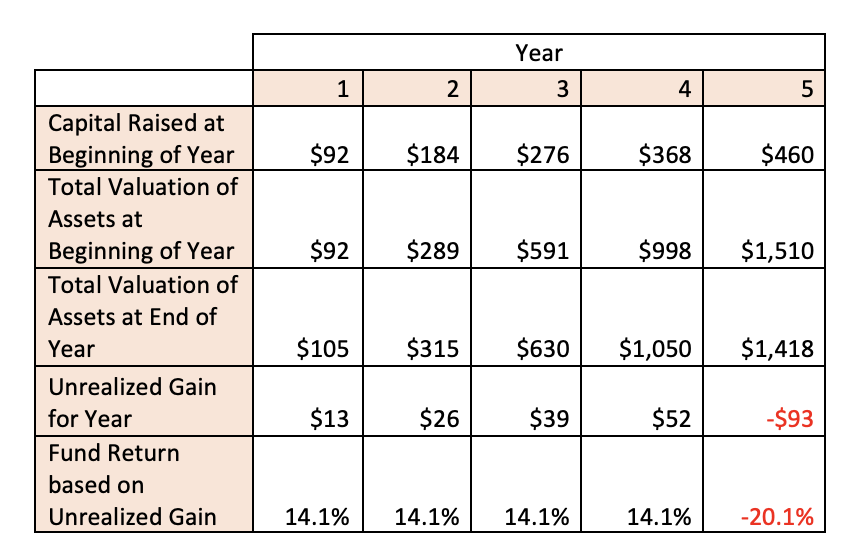

Let’s go back to our example of an asset with a $90 bid price and a $100 ask price. Let’s assume a fund can buy the asset at around $92. Now let’s assume that it uses a third-party provider or practice that allows it to value the asset at $105 – which is greater than the ask price. This means the fund can purchase the asset at $92 and immediately value it on its books at $105 – a $13 gain which amounts to a 14.1% immediate paper gain. Even if the fund had no other gains for the remainder of the year, it would still be able to post a 14.1% return for the year.

Let’s assume that the open-ended fund posts a 14.1% return for the year and is able to attract more investors in year two based on the strong performance in year 1. Let’s say in year 2 the open-ended fund raises $184. Once again, the bid/ask spread of the assets are at $90/$100. But this year, they’re able to buy twice as many assets at the $92 price and book it at a $105 price for another 14.1% gain. In years three and four they use this same strategy again but with an even greater amount of assets. In year five, the fund finally writes down the value of their assets to bring it more in line with the current market value.

Effect of booking unrealized gains on assets with large bid/ask spreads

We can quickly see how this poses a problem. By continuing to play this valuation game, small funds can become large funds by raising increasing amounts of capital using great unrealized paper returns while generating minimal realized returns for investors. If investors ever decide to redeem, funds that use this valuation tactic will have to sell assets at well below their booked value thereby generating losses for the fund.

However, for small funds using such tactics, the reward can be well worth the risk. The fund gets to show great returns in its early years – when capital raising is difficult – by booking assets at higher prices than they could be sold. The fund can then raise increasing amounts of capital and earn management and performance fees all based on these unrealized returns. As long as these funds buy new assets, they continue to show great paper returns.

By the time investors start to redeem en masse, or the fund finally writes down the book value of its assets to align with prices buyers will pay, the fund has already made millions of dollars in fees and established relationships in the space that will with withstand the one-time hit to their NAV. This success would not have been possible if it had not employed such tactics and posted lower returns in the early years.

Even early investors benefit from this strategy – as long as they exit before everyone else. It’s only later investors that decide to invest off these great paper returns and don’t exit in time that will pay the price.

This is not to say that all open-ended funds of assets like life settlements with unlevel/hard-to-value future cashflows are inherently bad. Open-ended funds of such assets can provide highly valued liquidity to investors who otherwise may not wish to invest in the asset class at all.

Difficult-to-value assets – particularly those with unlevel cashflows – are best suited for closed-end funds where management and performance fees can be based on actual realized returns and not manipulated by how the assets are valued based on a volatile future cashflow stream.

Investors that allocate capital to life settlements through open-ended vehicles need to understand that there is a large premium being assessed on this liquidity. As such, extra due diligence is required to ensure both the expertise of the fund manager and the determination of the fund’s realized and unrealized returns.

Rajiv Rebello, FSA, CERA is the principal and chief actuary of Colva Capital LLC. Colva Capital LLC is a registered investment advisory (RIA) firm that helps other RIAs, family offices, and institutions invest in low/uncorrelated asset classes like life settlements in both open-ended and closed-ended structures. Rajiv can be reached at [email protected].

Read more articles by Rajiv Rebello

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

As the above table shows, an investor expecting to earn a 9% compound annual return would need to stay for the entire five-year period since the returns are low in the early years and high in the later years. If the investors exit before year four, they earn only a 4% compound annual return.

As the above table shows, an investor expecting to earn a 9% compound annual return would need to stay for the entire five-year period since the returns are low in the early years and high in the later years. If the investors exit before year four, they earn only a 4% compound annual return. We can quickly see how this poses a problem. By continuing to play this valuation game, small funds can become large funds by raising increasing amounts of capital using great unrealized paper returns while generating minimal realized returns for investors. If investors ever decide to redeem, funds that use this valuation tactic will have to sell assets at well below their booked value thereby generating losses for the fund.

We can quickly see how this poses a problem. By continuing to play this valuation game, small funds can become large funds by raising increasing amounts of capital using great unrealized paper returns while generating minimal realized returns for investors. If investors ever decide to redeem, funds that use this valuation tactic will have to sell assets at well below their booked value thereby generating losses for the fund.