Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This third quarter update of Global Investment Report’s 18th annual global hedge fund survey highlights some of the remarkable distortions revealed across markets, while reporting on the current sentiment of leading investors and tracking how the top 50 funds have performed through the first three quarters of 2021.

A Dickensian sounding article in The New York Times caught my attention. Written by the paper’s senior economics correspondent Neil Irwin, it started off saying, “Americans are, by many measures, in a better financial position than they have been in many years. They also believe the economy is in terrible shape.”

This got me thinking of other paradoxes.

The flagship gap – triggered by consumer and corporate demand colliding with clogged supply chains – sits off southern California’s ports with dozens of massive, fully loaded container ships waiting to dock.

Then there’s the great macro divide: many economists and asset managers see inflation, which in October hit an annual rate of 6.2% (the highest since 1990), as more than a response to economies reopening. They are increasingly fearful of how far the Federal Reserve may be falling behind the inflation curve. Fed Chair Jerome Powell finally announced a start to tapering the bank’s $120 billion monthly bond purchases. But as of mid-November, Powell was against directly raising rates, believing this will not address the underlying issues driving inflation, despite overnight rates remaining at crisis-level lows.

The Fed’s fear of letting the bond market adjust to a vastly improved economy since Covid struck nearly two years ago has created sharp imbalances reflected most clearly in negative real returns across the yield curve. Fearful of the recovery’s fragility, European and Japanese monetary policies remain even more accommodating. And the Bank of England just spooked bond markets on both sides of the Atlantic when it suddenly yanked back on a proposed rate hike (see graph below).

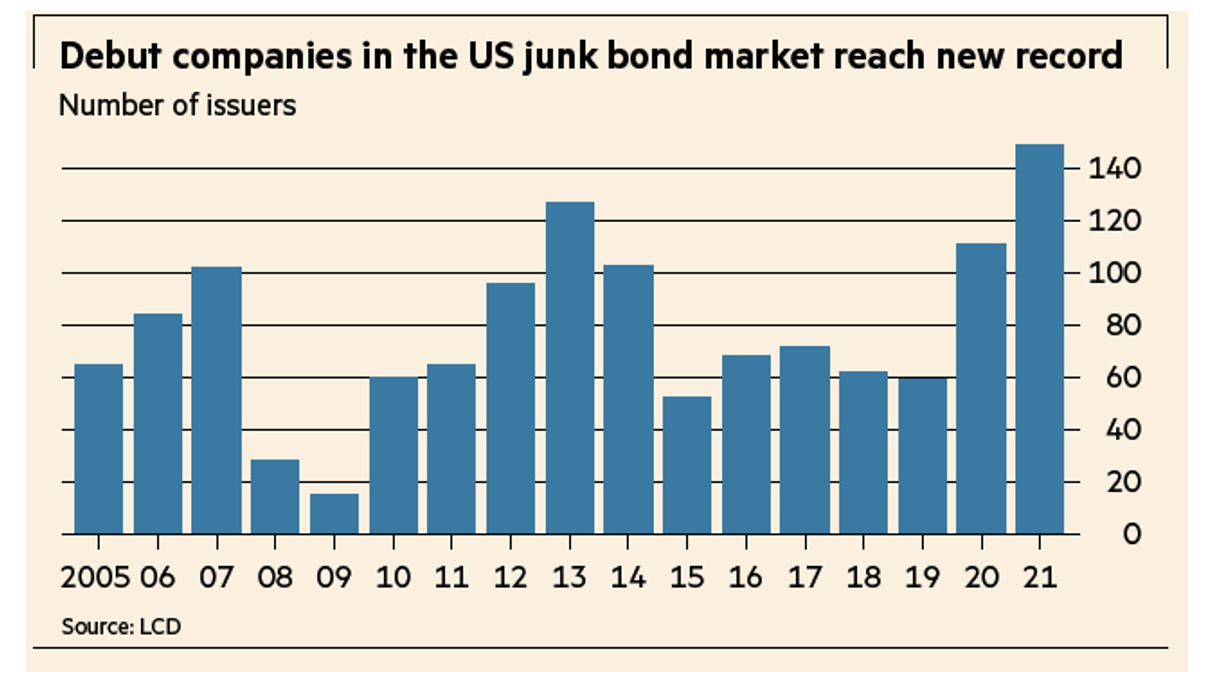

Ultra-low rates continue to fuel capital flows into higher risk assets, keeping the junk bond rally going. According to ICE Data Services, soaring issuances has pushed the high-yield debt market above the $1.5 trillion mark for the first time. The Financial Times reported a record 149 companies have tapped into the junk bond market so far this year, including the likes of the cryptocurrency exchange Coinbase and gaming platform Roblox, the latter paying less than 4% for $1 billion (see table below). The gap between risk and return on sub-investment grade debt has rarely been so wide, pushing bond prices even higher while major equity markets continue to rally, even after the S&P 500 has doubled since March 2020.

Then there’s the polar divide between the world’s two largest markets. Through September, US stocks gained more than 15%, according to MSCI. China was down more than -16% in Yuan terms as local authorities pursue actions that have chilled investor sentiment. And this performance gap drastically widened by early November as US stock returns surged to nearly 26% for the year while Sino shares have remained unchanged.

Despite a broad sense Covid-19 is finally coming under control, we're seeing disturbing infection spikes among the large percent of the unvaccinated as the weather turns cold, leading to lockdowns. That indicates we'll likely see another wave of the pandemic hit developed nations this winter.

In seeing stocks and bonds (not to mention real estate) at record highs, Yale economics professor, Robert Shiller, recently noted, “these three asset classes have never been this overpriced simultaneously in modern history.”

That said, Howard Silverblatt, senior analyst at S&P/ Dow Jones Indices, recently reported third-quarter sales of the companies comprising the benchmark 500 index hit a record high of $3.3 trillion and operating margins are still near all-time highs at 13.17%. At the same time, 80% of the firms are reporting earnings that have topped expectations.

Michael Mauboussin, a managing director of Counterpoint Global at Morgan Stanley and a long-time well-respected market observer, doesn’t believe stocks are generally mispriced. While there are pockets of speculation, Mauboussin thinks markets have been acting rationally over the past 18 months.

So while there are plenty of provocative schisms, what do they mean? Maybe tipping points? Maybe opportunities?

Said Haidar, manager of the highly volatile and profitable global macro fund Haidar Jupiter appears to have rallied off these current imbalances and dislocation, with his fund having soared by more than 70% year-to-date through September.

The manager wouldn’t comment for this report. But a clue about his exposure may have been revealed in his recent investor letter obtained by Institutional Investor. Haidar believes the global transition towards renewable energy has resulted in under- investment in fossil fuels. Along with rapid economic recovery, this has contributed to significant tightness in energy markets. Then add supply chain problems, rising labor costs, and other issues. Together this makes him think central banks may be forced to acknowledge high inflation is likely to be less transitory than they had originally forecasted. And to this macro manager, this suggests equities are vulnerable.

Uncertainty borne out of these and other concerns may be why some hedge fund managers are pulling back a bit on leverage and risk from their books.

Appaloosa Management’s founder David Tepper is more blunt. “I don’t love stocks. I don’t love bonds. I don’t love junk bonds,” says the hedge fund manager. Not particularly concerned about a crash and still substantially exposed to the market, Tepper says he “just doesn’t know how interest rates are going to behave next year.” And this is what’s giving him and many other managers pause as the rally continues.

Strategies

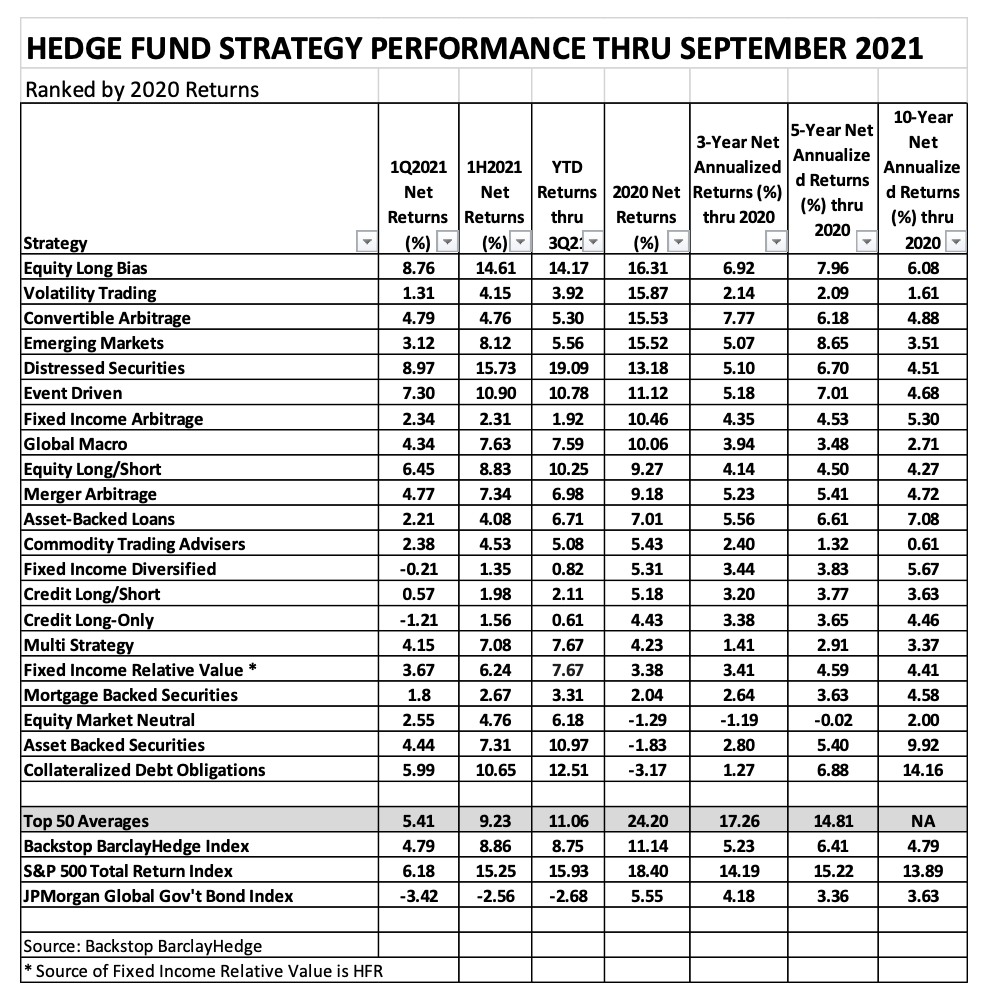

Through the first 9 months of the year, hedged equity strategies performed in line with the market. (See Strategy Performance table below.) Equity long bias led the pack, returning more than 14%, followed by event driven funds (up an average of 10.78%) and equity long-short funds (which gained 10.25%).

The biggest turnaround from a year ago have been asset-backed securities and collateralized debt obligations, fueled by return of credit confidence, an abundance of liquidity, and the search for yield. While they both ended 2020 down more than -2%, through the first three quarters of 2021, ABS strategies have rallied 11% while CDOs did even better, up 12.5%.

But the strategy that continues to thrive above all others is distressed securities. “This has been a remarkable period for funds investing in struggling companies,” explains Tilo Wendorff, managing director of absolute returns at the $10 billion German Alternative Investment firm Prime Capital.

Wendorff explains the distressed rally has been driven by the rapid recovery of the economy along with many of the same factors that have propelled ABS and CDOs. Distressed managers bottom-fed on corporate debt most exposed to the pandemic and shutdowns. And as the demand for secondary and new debt offerings helped repair broken balance sheets as the economy rallies, the price of distressed legacy debt has greatly improved.

As of the end of September, distressed funds were up more than 19%, topping both the market and every other strategy by a wide margin. Wendorff expects the strategy to continue to thrive as economies recover into 2022.

Credit strategies, however, have struggled the most this year. Long credit and fixed-income diversified returns haven’t cracked 1%; credit long-short managed gains of 2.1%. The primary issue: conjuring interest rate trends has been tough. And this was most evident early into the 4th quarter when fund managers across developed markets misread central bankers from the US, the UK, to Australia. Bloomberg reported substantial losses “show how even some of the most sophisticated traders have been caught flat-footed by the rapid shift in sentiment that has raced through markets.”

The top 50

This group of select funds have shown wide performance dispersion through the first nine months of the year, ranging from a loss of -20% to a gain of 70%. However, the strength of the group’s overall performance is evident with 26 funds registering double-digit gains compared to only 3 funds logging double-digit losses.

Supply and demand gaps, dislocation, and confusing trends may be the source of opportunities, enabling many fund managers to uncover alternative, uncorrelated idiosyncratic investments.

Waha MENA emerging market equity fund (No. 22) has benefitted from resurging Middle Eastern economies as they fully reopen supported by high levels of vaccination, rebounding energy prices, and soaring travel. The fund has gained nearly 22% through the first three quarters of 2021.

Manager Mohamad El Jamal remains upbeat for the near term believing energy prices will continue to increase along with corporate earnings. He also expects valuations to receive “a boost from rising multiples as emerging market investors rotate into dollar-pegged economies, especially energy-oriented MENA markets.”

His largest concern? The gap between rising US inflation and interest rates. “Aggressive Fed intervention is the key risk,” El Jamal explains, “especially in our region where energy prices are quoted in dollars and our local currencies are also pegged to the Greenback. Fed decisions are the most impactful of all central banks, and if it plays catch-up and starts moving aggressively, then this will likely shock financial markets.”

Over in Asia, China’s disruption of markets and the global economy has blurred thinking about the region’s near-term investment prospects. But some active fund managers are profiting around the confusion.

Hong Kong-based Segantii Asia-Pacific Multistrategy (No. 48) is having one of its best years in a while because of various emerging opportunities. Year-to-date through September, the fund has gained more than 12%. Singapore-based emerging market fund FengHe (No. 28) is up 24.5%.

Chinese policy hasn’t prevented corporations in the region from being active in capital markets and pursuing M&A in response to the pandemic, supply chain problems, Beijing’s market interference, inflation and projected rising interest rates.

Asset managers are investing in new listings and secondary offerings along with convertible and credit issuances. They’re establishing positions in targeted and acquiring companies, and arbitraging the gaps forming between legacy and new secondary listings.

Having effectively navigated this year’s unique dynamics so far, FengHe’s founding partner and CIO Matt Hu doesn’t seem particularly surprised by the Chinese government’s recent behavior. “Markets have been shocked by various policy announcements and events in China, from K12 education reforms to Internet crackdowns to a common prosperity drive to the Evergrande problems to power cuts,” observes Hu. But he views “such changes as normal and not unexpected.”

NY-based macro manager Said Haidar is far more worried seeing China’s “crackdown of numerous industries threatening to slow Chinese growth significantly, further weighing on emerging markets.”

Back in the States, small-cap activist fund Legion Partners (No. 14) was up 17.3% during the first three quarters of the year as the fund’s targeted companies continue to rally with the economy and adjusting to an evolving reality related to supply chain backlogs, inflation, and anticipated rise in interest rates.”

Managing director Ted White sees dealing with these matters as part of navigating Covid. “We believe many of the changes that companies have been forced to make,” explains White, “are often simply expediting what was likely to happen further down the road, demanding disciplined responses in making firms stronger.”

One such response to supply chain challenges is diversifying the number and geography of suppliers. In addition to targeting suppliers in Central and Eastern Europe and shifting deliveries to US east coast ports, White also believes there will be increased demand for domestically produced parts and products, in spite of their higher prices. A portion of these costs may be passed on to consumers, but he does expect margins to tighten. Overall, White remains constructive about near-term economic and market outlook well into 2022.

Looking ahead

European prospects recently received a dose of bad news with new Covid-19 cases surging in Germany that’s threatening consumer demand and further exacerbating supply chain issues that have been weighing on the country’s industrial output. (The Financial Times reports only two-thirds of Germany has been vaccinated.)

In response, the German Council of Economic Experts lowered its 4th quarter growth projections to 0.4%, a large drop from last quarter’s 1.8% expansion. Being Europe’s largest economy, this slowdown will hit the continent’s near-term growth prospects.

Neighboring Austria just announced a lockdown of all unvaccinated citizens, which is an even larger percent of the public than in Germany.

Such COVID spikes may temporarily ease inflation worries, supporting the European Central Bank’s loose monetary policy. But rising prices remains a top concern globally.

Prime Capital’s Wendorff doesn’t know if inflation is a temporary or more systemic concern. If it’s the latter, he believes it could create more uncertainty and volatility from which hedge funds can profit.

Waha MENA’s El Jamal takes some comfort in past Fed behavior. “Every time the central bank started moving overnight rates back up, they’ve peaked at sequentially lower levels,” observes El Jamal. And each time investors have panicked in response to tighter Fed policy, the central bank has backed off, quickly revitalizing shaky growth and markets. “And the stimulus response has gotten larger each time around,” notes El Jamal.

Some asset managers are less optimistic about lagging monetary policy.

Vincent Berthelemy, cross-asset strategist and portfolio manager at the $7.5 billion global alternative investment firm Investcorp-Tages, is less certain of market response to central bank policy playing catch up with inflation. But he thinks it might be wise to start raising cash to deploy when markets sell off. He recommends to “be tactical in risk taking, buying on dips (especially value) & selling on rips.”

But overall, Berthelemy remains positive about the broad economic backdrop, anticipating further healthy growth. Given the market’s prolonged rally, he recommends staying defensive with below average beta exposure. “Valuations and positioning leave little room for error even in the absence of major risk catalysts ahead,” notes Berthelemy, “so we prefer to proceed carefully with neutral exposure across markets.”

Strategically, as dispersion increases he favors proven equity market neutral managers with wide industry reach. He also sees event driven managers well positioned to play mergers and special situations. And he believes quality discretionary macro and relative value managers will be able to respond to evolving central bank-driven markets.

Key to matters of global supply chain and growth, China is the other big unknown. Economist Mohamed El-Ehrain, now president of Queen’s College at Cambridge, says, “government actions during the past few months (has triggered) a real concern about the investability of the (Chinese) market.” He surmises Western investors may be “treated as the equivalent of a high-risk junior tranche . . . the first to be hit by any shock.” El-Ehrain explains the split in investor sentiment with some seeing the recent sell off as a rare buying opportunity, while others thinking this is the calm before another storm.

In its recently released 2022 Outlook, the Economist Intelligence Unit believes a property crash in China as a leading global risk that could trigger a sharp economic slowdown. “Chinese property giant Evergrande has already missed some repayments on debt totaling about $300 billion,” states the EIU, “and given exposure to the company across much of China’s economy, its potential default represents a serious risk of financial contagion.”

It fears a string of defaults across China’s real estate sector could substantially weaken the country’s banks, wealth, investment and growth prospects, potentially “instigating a global economic downturn.” Commodity exporters (and we can assume prices) would be particularly affected by a period of much weaker demand from China.

Concluding on an upbeat note, accounting and consulting advisory Deloitte paints an especially benign domestic picture. Senior manager, Daniel Bachman believes greater vaccination should allow the US to continue to recover, stimulated by pent-up demand across consumer sectors.

The approved infrastructure package and the likely passage of Biden’s Build Back Better bill should propel further growth in 2022 around the same time consumer and housing demand and capital investment may begin to ease back to pre-pandemic levels.

Bachman expects improved productivity growth and improving supply chain performance will help reduce inflation pressures. He also surmises unemployment will continue to fall to around 4%, the Fed will likely hold rates close to zero until late 2023, and long-term rates should remain constrained.

So what does this all mean for the various economic, monetary, budgetary and performance gaps? A major event will likely be required to narrow some of these imbalances. But over the near term, they will probably remain with us well into next year – sources of uncertainty, confusion, risk, and opportunity. So probably best to mind the gaps.

Global Investment Report is the only independent global survey of broad-strategy hedge funds, managed by Eric Uhlfelder. The 2021 survey was his 18th annual hedge fund review. Previous editions were commissioned by the Financial Times, Barron’s, The Wall Street Journal, and SALT.

For a copy of this year’s survey along with the Mid-Year and Third-Quarter Update, contact the author at [email protected].

Read more articles by Eric Uhlfelder

As of the end of September, distressed funds were up more than 19%, topping both the market and every other strategy by a wide margin. Wendorff expects the strategy to continue to thrive as economies recover into 2022.

As of the end of September, distressed funds were up more than 19%, topping both the market and every other strategy by a wide margin. Wendorff expects the strategy to continue to thrive as economies recover into 2022.