If Your Client-Service Model Ain’t Broke… Fix It Anyway!

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Service offerings that were premium yesterday may be considered ho-hum today. To keep your clients loyal and attract new business, you need to continually create “delight” with strategic updates.

Centralized asset accounts were first introduced more than 30 years ago and quickly became a source of “delight” for the investors whose advisors used them. Here was something new and exciting – a service that not every investor was getting. The value was tangible. Then time passed. More and more firms started featuring them, and it became a competitive disadvantage not to offer central-asset accounts.

This cycle – where a novel client offering gradually becomes expected and then taken for granted as a basic requirement – happens with most client-service innovations. Being aware of how your services are perceived and updating them accordingly is vital to keeping and attracting new clients.

The value of pursuing client loyalty

There is much supporting data that shows marketing to existing clients is significantly less expensive than to potential clients. Cross-selling is also much more likely with existing clients. Retention, or loyal clients, can be defined as clients who conduct business with only you now and in the future. In addition, they are very interested in considering new strategies, services, and solutions you recommend while resisting the “pull” from your competition. They also provide solicited and unsolicited referrals.

Client loyalty and retention are based on client satisfaction. The VIP Forum of the Corporate Executive Board stated that very satisfied investment clients are:

- almost three times as likely as the somewhat satisfied to use their primary provider for an unexpected investment need (73% versus 25%).

- twice as likely (75% versus 38%) as the somewhat satisfied to have referred their primary institution.

Mere satisfaction is not enough to allow advisors to reach lofty goals. Delivering satisfaction and therefore gaining loyalty is a process and a strategy, not a one-time event.

The issue in financial services, as in other industries, is that this must be displayed on a continuing basis; contact after contact, opportunity after opportunity, monthly, quarterly, and yearly. You must go beyond the core value of the client’s expectations. You must go “beyond better sameness.”

From working with advisors for over two decades, I know it’s critical to work on your core values and skills, like, rational investment planning and execution, 100% accuracy, comprehensive financial planning, timely, consistent, and proactive contact, and so forth. These are expected and are table stakes for client loyalty and retention. You must also express strengths of investment expertise, personalized planning solutions, experience, education, integrity, performance standards, and caring. Those factors are also expected and no longer the base for client loyalty or retention.

Those skills, capabilities, and values do not differentiate advisors from the other 300,000 or so financial professionals competing with them. All advisors claim all these characteristics.

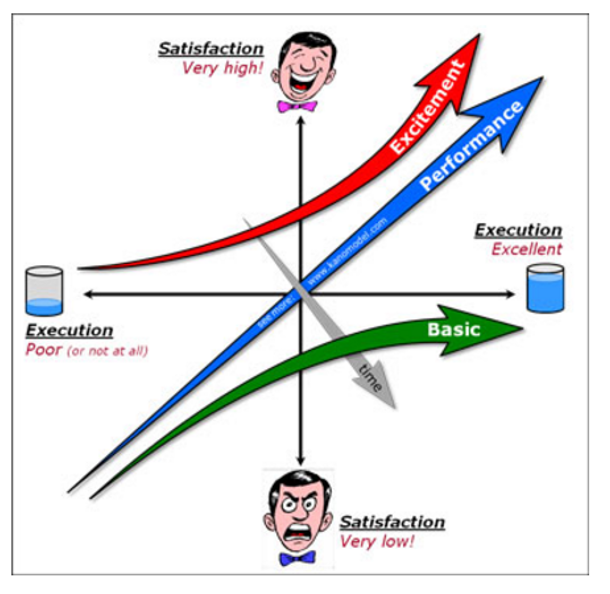

The Kano model

Dr. Noriaki Kano, a leading client satisfaction researcher, developed a model that speaks to this challenge of adding client value. Hhis model of client satisfaction, and the resulting loyalty, predicts that the degree of client satisfaction is dependent upon the degree of need fulfillment but is different for different levels of client expectations.

Dr. Kano’s model can be seen here.

Let’s look at the levels of service within Kano’s model.

Expected (basic)

Expected requirements are so obvious to clients that they do not state them overtly. When these requirements are met, the client says nothing and probably doesn’t even notice. When these features or services are not present, the client complains. Continually improving on meeting these kinds of needs will not elicit client loyalty or delight.

Examples: The telephone dial tone, executing trades

Normal (performance)

These are “fundamental” to quality delivery. Clients overtly state these needs and are very aware of them. When these needs are met, clients are satisfied. When they are not met, clients are dissatisfied. For many types of requirements in this category, it is possible to deliver more than client requirements and generate additional perceived benefit.

Examples: Performance reporting, responsiveness

Deliverables such as estate planning, education planning, tax advantaged strategies, financial/retirement planning, and, as stated above, central-asset accounts are non-differentiated services. Most advisors and advisory firms preach and teach these as standard deliverables.

Delightful (excitement)

Clients are not aware of all their needs. These are “latent” needs. They are real, but not yet in most clients’ awareness. If these needs are not met by a provider, there is no negative client response. They are not dissatisfied, because the need is unknown to them. If a provider understands such a need and fulfills it, the client is rapidly delighted, as in the case of central-asset accounts in the late 1970s.

Example: 3M Post-It Notes when first introduced (notice they are now considered a basic office supply!) The Ritz-Carlton going back many decades and their “Gold Standards” only going back several decades are still not the foundation of standards in that industry.

The future of delight

Sources of excitement when first introduced become expected as the market becomes familiar and saturated with them. That which delighted the client yesterday becomes a basic expectation as competition makes it an undifferentiated service. “Delighting” the client and increasing their loyalty takes more effort, cost, and creative thought over time.

What will be the latent client demands that will delight them and provide a differentiated solution? I see at least three possibilities: One is a function of poor execution on the part of industry participants; the other opportunities relate to enhanced services, financial and nonfinancial.

‘Walk the talk’ – Improved execution

One possibility for delighting the client is in consistently and continuously “walking the talk” rather than just “talking the talk.” One example is to establish a daily game plan for each client that varies based on the client’s value to the advisor’s business. That value is based on more than assets and revenues and is based on relationship, potential, and other factors. Establish a minimum number of face-to-face meetings, telephone-based portfolio reviews, and check-in calls per client. Every meeting has an agenda and goal, and every face-to-face meeting solicits feedback and introductions, if appropriate.

Few advisors do this.

The level of delivery that will meet and exceed client expectations calls for a new delivery and cost paradigm. This leads us to a discussion of enhanced services, financial and non-financial.

Enhanced financial services

Given constantly growing client expectations and competition from many sources, one of the newer possibilities for delighting the client is a whole new set of financial services that are a “facsimile” of family-office services for clients with $5 million or even up to $10 million or more in assets under management. Such services could include:

- Higher levels of financial planning

- Legal guidance and/or paralegal services

- Tax advice and even preparation

- Accounting services such as record keeping, budgeting, and bill paying

- Family governance

These are services that family offices for the ultra-wealthy already provide. Many questions remain, such as:

- Are these services implemented through regional centers at the firm or through tight expert alliances?

- Which clients receive which services?

- How are these services paid for?

- What happens to the referral-based relationships advisors have already established with centers of influence?

- Where do we find the time and expertise to offer these services?

Many top RIAs have become quite large and are offering these services. How many of their advisors are using those resources is not clear.

Enhanced non-financial services

Such services could include:

- Family education programs

- Business and personal security

- Concierge services such as travel planning

- Luxury acquisition services

- Property management

These are also offered by family offices for the ultra-wealthy. Many questions also remain, such as:

- How are these services implemented?

- Is there enough demand to warrant organized lifestyle services?

- How are these services paid for?

The next step is to determine which clients or prospects will value which services.

As Wayne Dyer said, “There is no scarcity of opportunity to make a living at what you love to do; there is only a scarcity of resolve to make it happen.”

Execution is critical because a small advantage will make a large difference in results. Sam Silverstein’s “law of fractional advantage” states that all you need to do to win at anything is to be slightly better than your competition.

“We don’t have a problem knowing what we should do. The problem is that we just don’t do it!” said authors Steve Levinson and Pete Greider in their book Following Through: A Revolutionary New Model for Finishing Whatever You Start.

Remember

- Client loyalty and retention, based on delighting clients, has significant value.

- That which pleased and even delighted the client yesterday is a basic expectation today.

- “Delighting” the client and solidifying their loyalty takes more effort over time.

- Opportunities to “delight” may come from three sources:

1. Improvement in execution

2. Enhanced financial services

3. Enhanced non-financial services

A parting thought or two:

“Well, in out country,” said Alice, still panting a little, “you’d generally get to somewhere else – if you ran very fast for a long time, as we’ve been doing.”

“A slow sort of country!” said the Queen. “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!”

– Lewis Carroll, Alice’s Adventures in Wonderland

Also remember the observation by Henry Wadsworth Longfellow:

The heights by great men reached and kept Were not obtained by sudden flight, But they, while their companions slept, Were toiling upward in the night.

David Leo is founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant, and trainer to financial professionals. David is an experienced business manager who has worked for over two decades solely with financial advisors, planners and firms who want to organize, structure & grow their businesses by attracting, servicing, and retaining affluent clients.

David had a 30-year career at IBM including as a business process reengineering consultant and engagement manager for the financial services industry. He also spent seven years at UBS/PaineWebber working directly with financial advisors to assist them in productivity growth.

David received a Bachelor of Science degree in commerce and engineering from Drexel University and an MBA from New York University.

If you would like additional details or have any questions about his articles or an interest in coaching, schedule a free 45-minute strategy session @ https://calendly.com/davidileo or contact him @ [email protected]. Call 212-598-4229 (Office) or 917-379-1249 (Cell) and visit @ www.CoachDavidLeo.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All