Despite the strong recovery for value stocks since late 2020, they are still priced at historically cheap levels – comparable to their level at the peak of the tech bubble. That is especially true for small-value stocks.

Despite the strong recovery for value stocks since late 2020, they are still priced at historically cheap levels – comparable to their level at the peak of the tech bubble. That is especially true for small-value stocks.

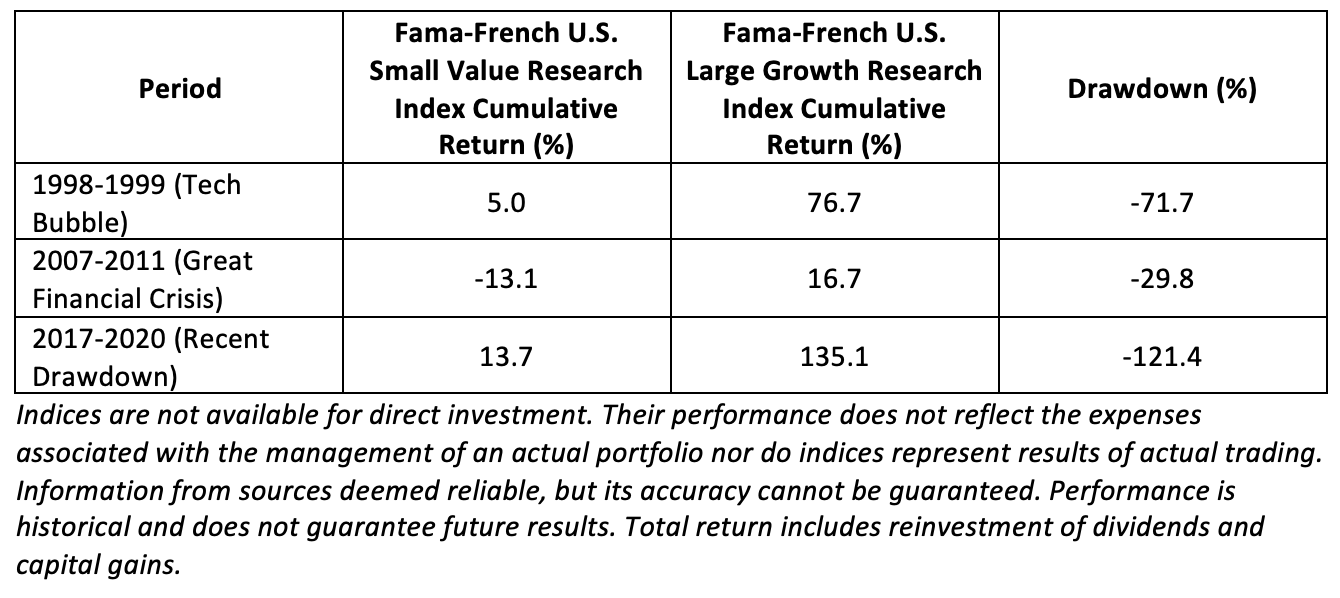

For the period 1927-2020, the Fama-French U.S. Small Value Research Index returned 13.9%, outperforming the Fama-French U.S. Large Growth Research Index, which returned 9.9%, by 4 percentage points a year. This outperformance led many investors to “tilt” their portfolios to small-value stocks (overweight them relative to their share of the total market). However, over the 23-year period 1998-2020, investors in U.S. small-value stocks have been disappointed, as the Fama-French U.S. Small Value Research Index slightly underperformed, returning 9.7% versus 9.9% for the Fama-French U.S. Large Growth Research Index. That disappointing performance was caused by three large drawdowns for small value relative to large growth, with the most recent drawdown being of historic proportions.

Small-value stocks began a dramatic recovery in late 2020. Using the last 12 months of available data (October 2020-September 2021), the Fama-French U.S. Small Value Research Index returned 87.9% versus the 27.1% return of the Fama-French U.S. Large Growth Research Index, an outperformance of 60.8 percentage points. Using live funds, we have access to more current data. Using Morningstar data, over the one-year period ending November 17, 2021, the Bridgeway Omni Small-Cap Value Fund (BOSVX) outperformed the iShares Russell 1000 Growth ETF (IWF) by 31.8 percentage points. However, despite that dramatic outperformance, BOSVX’s performance still trailed IWF’s over five- and 10-year periods by significant margins, 14.6 percentage points and 6.5 percentage points, respectively.

With that said, BOSVX’s valuation relative to the market indicates that small-value stocks are still trading at historically cheap levels – despite the fact that interest rates are much lower, and their earnings are growing faster as they recover from the cyclical lows caused by the pandemic.

Using Morningstar data, BOSVX had a P/E of just 9.3. At the end of 2013, before the expansion of the P/Es of growth stocks, BOSVX had a P/E of 11.0. Thus, small-value stocks are trading cheaper today than they were back in 2013, while the valuation of the market overall, and growth stocks in particular, have significantly increased. For example, in 2013 the S&P 500 earnings were about 105 and the index closed at 1782, a P/E of 17. The current full-year forecast for S&P 500 earnings is about 205. As of this writing, the S&P 500 was at about 4,700, producing a P/E of about 23. While BOSVX’s valuation has fallen 9%, the valuation of the S&P 500 has risen by 26%. As Adam Zaremba and Mehmet Umutlu, authors of the 2019 study, “Strategies Can Be Expensive Too! The Value Spread and Asset Allocation in Global Equity Markets,” demonstrated, the valuation spread provides information as to the future expected premium – the wider the spread, the larger the expected outperformance.

Valuation spreads at historic highs

Thanks to the research team at AQR, we can examine how the current spread between value and growth stocks compares to historical spreads. AQR’s hypothetical value composite includes five value measures: book-to-price, earnings-to-price, forecast earnings-to-price, sales-to-enterprise value and cash flow-to-enterprise value, and spreads are measured based on ratios. To achieve industry neutrality, their value spreads are constructed by comparing the value measures within each industry, which are then aggregated to represent an entire portfolio. AQR examined the current percentile ranking for large-cap stocks over the period 1984-October 2021 and found that in both the U.S. and emerging markets, value stocks were trading at the 100th percentile. In developed international markets, they were trading at the 99th percentile.

In other words, despite their strong recovery that began in late 2020, value stocks all around the globe are trading about as cheap as they have since 1984 relative to growth stocks.

AQR’s research team then examined what the current valuation spread implied about the market’s expectations for the cumulative difference in earnings growth for value and growth companies over the next five years and then compared that to actual analyst forecasts. They found that valuations implied that the earnings of developed-market growth stocks would be about 80 percentage points greater than those of value stocks despite analysts’ forecasts of only about 20 percentage points more growth. For emerging markets, the implied gap was more than 120 percentage points, while analysts’ forecasts predicted only a gap of about 40 percentage points. AQR also examined the historical data back to 1990 and found that the current spread in cumulative expected earnings growth was about two times the maximum historical realized spread for developed markets and about three times the maximum historical realized spread for emerging markets. In terms of the actual realized spread in earnings growth, it was about 20 percentage points for both developed and emerging markets.

While there is no formal definition of a bubble in stock prices, this has indications of being one.

Information in the valuation spread

Keeping in mind the historic cheapness of value stocks relative to growth stocks, AQR then examined the information content in the valuation spread. Using their HML Devil B/P measure for value, they found that over the period July 1950-December 2020, the correlation of the value premium to the valuation spread was 0.89, resulting in an r-squared of 0.79 – the spread contains significant information as to the future value premium.

The impact of valuation changes on returns

In an interesting exercise, AQR also examined how the changes in the valuation spread impacted the value premium over the period July 2018-December 2020. They found that the realized premium was -9.4%. However, if valuations had been unchanged, the premium would have been +3.1% – valuation changes had a -12.5% impact on the value premium. The change in valuation spread had a large impact on performance.

With this in mind, we can examine how the value premium performed after the previous peak in valuations (at the height of the tech bubble). Using data from the Ken French Data Library, from 2000 through 2006 the Fama-French U.S. Value Research Index returned a cumulative 140.1% versus the -8.1% return for the Fama-French Growth Research Index. Over the same period, the Fama-French U.S. Small Value Research Index returned 264.9% versus -8% for the Fama-French U.S. Large Growth Research Index.

Investor takeway

Despite the imprecision inherent in forecasting returns, market valuations provide valuable information as to expected returns. With the valuation spread between value and growth stocks at levels comparable to the spread at the height of the tech bubble, the evidence argues that the ex-ante value premium is at a historic high and that investors should expect (understanding that there is still a wide dispersion of possible outcomes) a repeat performance of what we experienced from 2000 through 2006.

The problem for investors is that over my more than 25 years of experience as Buckingham’s chief research officer, I have learned that one of the greatest mistakes investors make: When it comes to judging the performance of risk assets, they think three years is a long time, five years a very long time and 10 years an eternity. On the other hand, any financial economist would tell you that when it comes to risk assets, 10 years is likely nothing more than “noise.” Thus, such periods should not cause you to abandon a well-thought-out plan and make the mistake known as “resulting” – judging the quality of a decision by the ex-post outcome instead of by the quality of the decision-making process.

Larry Swedroe is the chief research officer for Buckingham Strategic Wealth and Buckingham Strategic Partners. He owns CCLFX in his personal accounts and Buckingham recommends it to its clients.

This is for informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Mentions of the specific securities above are not a recommendation of the securities. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of the Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy or adequacy of this article. LSR-21-189

Read more articles by Larry Swedroe

Despite the strong recovery for value stocks since late 2020, they are still priced at historically cheap levels – comparable to their level at the peak of the tech bubble. That is especially true for small-value stocks.

Despite the strong recovery for value stocks since late 2020, they are still priced at historically cheap levels – comparable to their level at the peak of the tech bubble. That is especially true for small-value stocks.