Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is the second interview I did with an Asset-Map user. To read the first one, which includes background information on Asset-Map, go here. The first article discusses the history behind the series of Asset-Map articles and a brief introduction to Asset-Map.

Randy Dippell is a partner and advisor for AdvicePeriod in Chicago, Illinois. Some months ago, Randy, who also founded of Nestegg Advisory in 2012, had a big decision to make for his growing firm, regarding whether to:

- Continue to take on the growing responsibilities for the many day-to-day non-client centric business decisions a solo RIA has to make.

- Spend more time in operations, general management, compliance, technology, human resources, and financial management.

- Focus on the work he truly enjoys in client relationship management, investment and wealth management, and business development.

This is a decision many solo advisors regularly make and remake. Randy had more than a dozen years of experience as a senior private banker and client advisor in major banks before starting his own firm. He therefore understood the requirements for managing all the administrative requirements of a firm and decided that he would rather take advantage of the synergies that came with merging his firm into a large RIA like AdvicePeriod with all the corporate capabilities he needed plus its enhanced technologies. AdvicePeriod made a similar decision recently by joining Mariner Wealth Advisors, a mega and growing RIA. Randy can now focus all his energies on serving his clients and growing his business with a top-five RIA firm. Albeit the Mariner merger was a bit of a surprise, it was a happy one as Randy sees it.

Randy’s clients and use of Asset-Map

Randy works with the large pool of high-net worth clients in the $1 million to $10 million range. It’s these first-generation wealthy business owners and corporate executives where he most enjoys working because he knows he can help them reach their personal descriptions of financial success, a secure retirement if that’s what they choose, education for their children, and in general, enjoying the peace of mind they get from, as Randy puts it, staying up at night for his clients so they can sleep better. Randy wants his clients to see him as an extension of their family, their CFO. That’s where Asset-Map comes in. Because he understands his clients and their wants and needs, he is able to take advantage of Asset-Map’s capabilities and creates a base “stencil” (a template) of his prospects’ and clients’ base components of their financial lives, such as:

- Income, current and future

- Assets, financial, real, other, joint, and individual

- Insurances

- Liabilities

In his client and prospect meetings, Randy interactively updates the Asset-Maps with the client specifics, adds their relationships, household, business, other, that are important to the client or prospect, adds the income, assets, insurance, and liabilities that may not have been included initially, and deletes any data that is not part of the current financial situation. Randy shows the client or prospect that he has done his homework, understands their situation, and can present a “visually compelling” picture of the client’s current financial picture in detail, on the spot, in a single page.

While Randy has used other financial planning software including eMoney, MoneyGuidePro, and Right Capital, he now uses Asset-Map for all his clients and has integrated other software into his business, including Riskalyze that integrates with Asset-Map. A small number of his clients also use RightCapital, though its effective use requires more client interactions. Most of his clients prefer to leave updating the maps to their advisor. Randy has found the reports, charts, graphics, tables, etc. of other financial software are outdated almost immediately after they are produced while the Asset-Maps maintain an accurate enough picture of the client’s situation until their next review meeting when changes are integrated.

Asset-Map maintains a directionally correct picture of the client’s financial wellness. As an example, if a target map is created from the picture of the client’s financial situation that says the client must grow their assets by say $500,000 over the next 12 years to reach their target retirement goals, it’s not relevant whether that number is actually $476,789 or $524,382. The client and Randy know what must be done over time and there will be so many events occurring over those next 12 years that minor deviations are irrelevant to knowing exactly what actions must be taken. Asset-Map allows Randy to provide “clarity around the most important numbers and what adjustments to make to fix them.”

Randy’s planning philosophy

Like most advisors, Randy delivers to his client’s wants but as a professional, also makes sure he delivers on the client’s needs. His clients want simplicity. They want to know where they stand financially and what they must do to reach their “desired future state.” It would be unusual for clients to ask the question, “Are the projected numbers in net present value or discounted cash flow?” Randy knows that Asset-Map’s use of net present value reflects the projected numbers of the value of future assets and the projected numbers of shortfalls to meet goals or excesses over goals so there is confidence in what must be done to reach the client’s “desired future state.” The approach provides a clear picture of where the client is today and what they must do to get where they want to go.

Randy believes that given the tremendous number of variables that occur over any five- or ten-year period in the economy, the world markets politically and financially, and even in his client’s situations, making long-term future projections are not pragmatic. He provides year-over-year progress, keeps plans current, and reacts to conditions as necessary if they appear to be long-term, beyond normal market cycles. He monitors significant changes in client’s incomes and outgoes to help ensure plans stay on track.

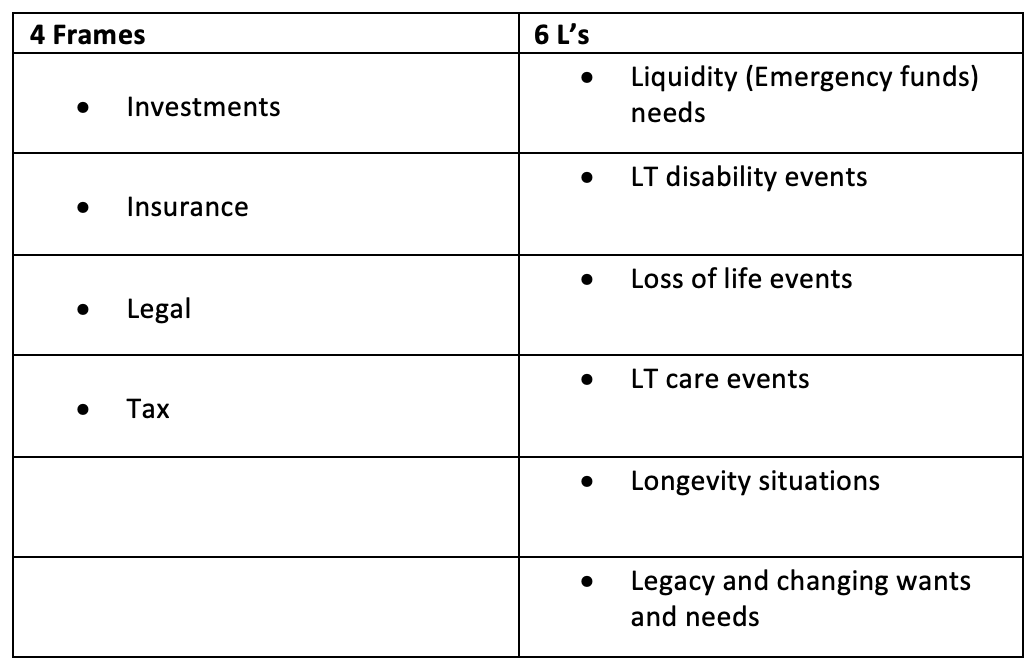

Randy’s clients don’t want multi-hour meetings with excessive detail. They prefer up-to-now information and whether they are on track. If not, Randy provides a do this, don’t do this summary and believes Asset-Map allows him to provide more frequent and focused communications. His use of the “4 Frames” and “6 L’s” allows him to have 10 thematic discussions throughout the year or as he calls it, “snackable wealth management.” As a reminder, these 4 Frames and 6 L’s are the contexts in which financial wellness must be considered. If unprepared for any of the potential situations presented in these areas, the financial plan can be thrown totally offtrack. So, it’s critical to always keep them in mind and discuss these contexts with the client.

These thematic contacts plus his semi-annual reviews as a minimum keep things on track.

In summary

Randy summarized Asset-Map as a tool that provides, “a simple, rich, visual graphic that delivers a snapshot of the client’s total financial condition today.”

He also said the discovery tools, and target-maps have accelerated his sales cycle because of their clarity. The discovery tools are not onerous and allow him to develop of first sketch with prospects that get his clients and him in the same ballpark and with simple tools like the drawing tool, they can verify and update the maps interactively to understand where they are today and quickly enable the discussion of the options to get to where the client wants to go.

The normal rapport-building elements of developing a relationship are a part of Randy’s discussion. But prospects and clients work with Randy because they want to reach a level of financial peace of mind. It’s natural that Asset-Map is a centerpiece of the initial discussions. Time, communications, and broadening the KYC experiences with the regular use of Asset-Map in all meetings will bring the relationships to the level that results in advocacy.

Randy became proficient in the use of Asset-Map within 90 days and said it has helped him and his clients make better financial decisions. As one of his clients told him after his first Asset-Map meeting, “I knew I had a lot of ‘stuff’, but I never knew I had so much and in so many different places.” Can you imagine what Randy’s next suggestion was?

David Leo is founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant, and trainer to financial professionals. David is an experienced business manager who works solely with financial advisors, planners and firms who want to organize, structure & grow their businesses by attracting, servicing, and retaining affluent clients.

David had a 30-year career at IBM including as a business process reengineering consultant and engagement manager for the financial services industry. He also spent seven years at UBS/PaineWebber working directly with financial advisors to assist them in productivity growth.

David received a bachelor of science degree in commerce and engineering from Drexel University and an MBA from New York University.

If you would like additional details or have any questions about his articles or an interest in coaching schedule a free 45 Minute Strategy Session @ https://calendly.com/davidileo or contact him @ [email protected]. Call 212-598-4229 (Office) or 917-379-1249 (Cell) and visit @ www.CoachDavidLeo.com.

Read more articles by David I. Leo

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.