Why Risk Tolerance Questionnaires Don’t Work for Determining Retirement Strategies

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsCan’t get there from here.

R.E.M.

Using a risk tolerance questionnaire (RTQ) to establish a retirement income strategy is akin to your doctor checking your pulse to measure your cholesterol. There is nothing wrong with checking your pulse, but it is an inappropriate test for the situation. We propose an alternative test – the RISA – to select the best deaccumulation approach.

During your accumulation years, you work and use the proceeds to fund essential living needs, emergencies, financial milestones, and hopefully save and invest a portion for retirement. Through it all, your human capital is how you pay the bills and “invest for the long term.” These savings enjoy a long-term horizon meant to cover retirement. Though there will be expenses that will need to be funded, thinking in terms of the assets-only wealth accumulation process offered by modern portfolio theory (MPT) is a reasonable approximation.

Investors are generally told to invest as aggressively as possible to earn the greatest risk premium from the stock market over the long-term, subject to their comfort with stomaching short-term market fluctuations that will hopefully balance out into a greater growth rate over time. RTQs have emerged as a tool to help advisors identify the amount of volatility their clients can stomach with their investment portfolios.

During accumulation, RTQs can serve as a helpful tool for advisors. They fit well with an assets under management (AUM) revenue model that offers a set of model portfolios designed with different risk levels. An RTQ also provides documentation for compliance about why a particular portfolio recommendation has been made.

While we applaud the many new developments that incorporate risk tolerance, capacity, and composure into RTQs, it is unclear how well they measure risk tolerance, how stable risk tolerance is during different market environments, and so forth. This article is not about these issues. Rather, we identify a significant shortcoming with RTQs, as well as a solution, when it comes to the question of retirement.

Why is investing during retirement different?

Investing during retirement is different than accumulation. The definition of retirement continues to be elusive. Whatever form (or even name) it takes, retirement is about a life transition. It is a transition away from being dependent on your human capital to fund your spending goals. If you don’t have employment income to fund your essential expenses, you have effectively transitioned how you fund your daily expenses from human capital to your investment capital. This changes the mental calculus.

If you are funding most of your essential expenses from your investment portfolio, the phrase “investing for the long term” is incomplete. MPT was designed for portfolios with no finite time horizon or distribution need. While the 30-year horizon in retirement may be a similar horizon to the accumulation years, retirement triggers new risks.

First, you need the portfolio to fund your expenses for an unknown lifetime. Investment risk also behaves differently in retirement. While you experience market downturns during your accumulation years, you are still earning a living and you continue to draw from your human capital for essential expenses while your portfolio remains invested. If anything, a market downturn allows you to buy more shares with your savings. Because your human capital is funding your daily needs, you have a very significant degree of separation from your portfolio during your working years. Once retired and taking distributions to cover spending, a market downturn has the opposite effect by increasing the number of shares you must sell to meet an expense. This is sequence-of-return risk, and its practical impact is to amplify investment volatility.

Then there is the burden of spending shocks and other contingencies. Retirees must also consider how much of their asset base is available for their retirement budget, and how much must be set aside as reserves to cover unexpected events like a long-term care need, a large healthcare bill, higher than expected inflation, and so on.

Retirement concerns

These new retirement risks can be classified into several distinct areas:

Longevity. Longevity concerns are directly related to the main risk of retirement income: outliving your money. Most examples center on financial independence and knowing that you can pay your basic expenses and not be a burden to others. These include but are not limited to daily living expenses, housing, and health care.

Lifestyle. Lifestyle concerns focus on maintaining your desired standard of living and enjoying your retirement with more discretionary spending. This aspect of retirement planning includes maintaining or improving your current lifestyle, rather than behaving more frugally than you would like to throughout retirement. This includes being able to spend on loved ones without impeding your retirement success. Typical lifestyle goals include travel and leisure, self-improvement, and social engagement.

Liquidity. Liquidity concerns involve maintaining enough reserves for unexpected contingencies. Maintaining enough liquidity is especially important for dealing with family emergencies, home repairs, long-term care, and an unexpected death or illness. Liquidity can also be a resource to fill in gaps when there is an unexpected market downturn.

These retirement concerns are largely absent from investment considerations while accumulating assets. While active financial planning during your accumulation years to accommodate your life milestones is essential, the main determinant of a successful investment experience for your retirement account while working relies on the asset allocation decision and maintaining your investment discipline.

Retirement strategy options

Because of the concerns we outlined, various retirement income strategies have been developed to source retirement income in a different manner than how you managed your investments during your accumulation years. Common retirement income strategies include:

Total return approach. This means you prefer to draw income from a diversified investment portfolio rather than using contractual sources to fund your retirement expenses. You expect portfolio growth to support a sustainable spending rate. In addition, you don’t mind the inherent variability of drawing income from an investment that will fluctuate in value.

Protected income approach. This allows for immediate and deferred annuitization to support greater downside spending protection by relying on contractually guaranteed lifetime income to build a floor for essential expenses. A total return investing approach can be added to this for more discretionary goals, but it will not be used for the essential longevity expenses.

Risk wrap approach. This blends investment growth potential with lifetime income benefits, generally through a variable annuity, a registered index-linked annuity, or a fixed-index annuity. Such tools can be designed to offer upside growth potential alongside secured lifetime spending, even if markets perform poorly. This provides a protected source of lifetime income as part of the overall investing strategy.

Time segmentation or bucketing approach. This approach offers contractual protections without sacrificing flexibility. Money is divided into different categories, earmarking assets for spending immediately, soon, and later. Bond ladders are often a good solution for shorter to intermediate income needs, and a diversified growth-focused investment portfolio is deployed for longer-term expenses. The longer-term portfolio can gradually replenish the short-term buckets as these funds are spent.

One of these strategies must be chosen before considering an investment allocation in retirement. But there is a significant gap in the planning profession because there have not been tools to help retirees or their advisors assess what retirement income strategies will fit their retirement income style.

New slang

We have various retirement income strategies, but no way to determine which strategy is most appropriate for a given individual. How do you want to source retirement income in a way that addresses your retirement concerns? Unfortunately, RTQs are mistakenly tasked with answering this question. While RTQs are directionally useful for accumulation-based portfolios, they were not intended to handle the broader question of retirement strategies. They will still play a role with deciding on asset allocation, but the broader question of choosing a retirement income strategy must happen first.

Using an RTQ to settle on a retirement income strategy is akin to putting the cart before the potentially wrong horse! One should not bypass the retirement income strategy decision and go right to an investment allocation.

RTQs do not explicitly address the new risks a retiree faces, and they completely sidestep the identification of an appropriate retirement income strategy for a client. Identifying your preferences for sourcing retirement income to fund essential expenses is a better way to assess what retirement income strategies will best fit your style. RTQs were developed with only a total return worldview in mind.

Over the past few years, we have been engaged in a research process to look at individual preferences. This has led to our Retirement Income Style Awareness® (RISA®) Profile as a model for selecting retirement income strategies. This is a scale developed from the two primary retirement income beliefs:

Probability-based versus safety-first (PS) details how individuals would like to source their retirement income. Probability-based income sources are dependent on market growth to provide a continuous and sustainable retirement income stream. On the other hand, safety-first income sources incorporate contractual obligations. Though no strategy is completely safe, the inclusion of contractual protections implies a relative degree of safety compared to unknown market outcomes.

Optionality versus commitment (OC) delves into the degree of flexibility sought. Optionality reflects a preference for flexibility to respond to economic developments or changing personal situations. Conversely, commitment reflects a preference for one solution. That generally means you're less concerned about unfavorable economic or personal developments, confident that your strategy solves for such contingencies.

For more detail on our methodology, scale creation, and results, read here.

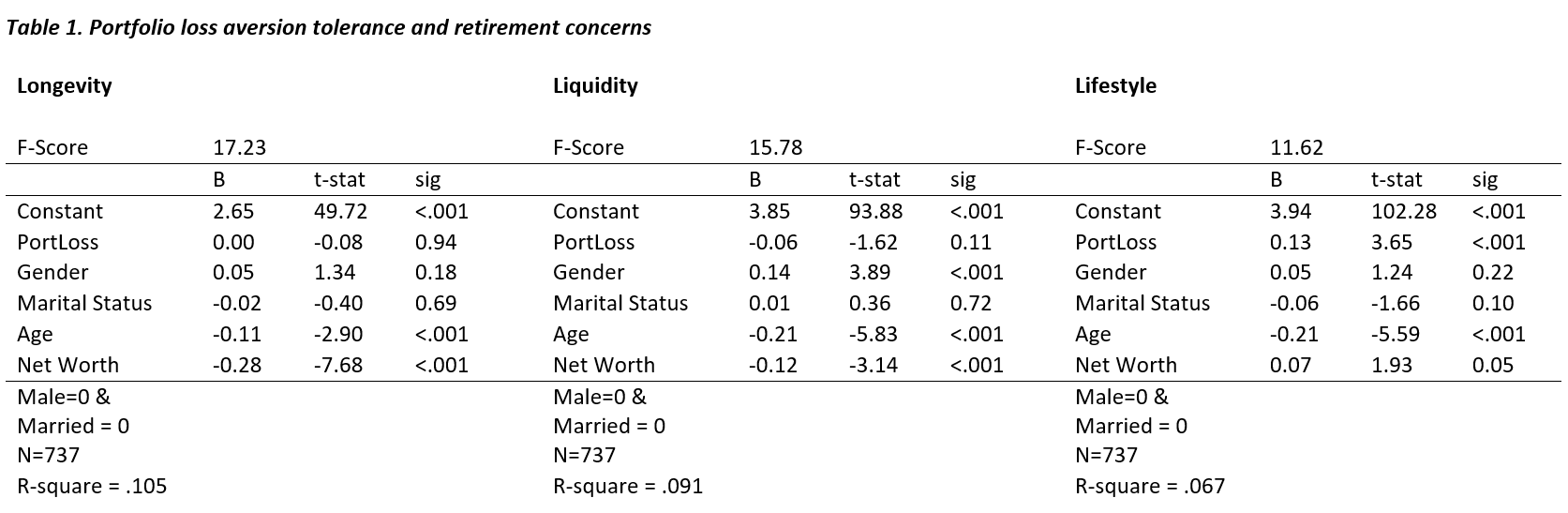

Let’s analyze how an RTQ compares with these broader retirement measures to understand the concerns people have when facing the new risks of retirement. Specifically, we look at whether portfolio loss aversion tolerance (PortLoss), which is the foundational component of RTQs, is significantly associated with the retirement income concerns related to longevity, lifestyle, and liquidity. We will also account for gender, age, marital status, and net worth (a potential proxy for risk capacity) in the analysis.

Table 1 shows the results from our ordinary least squares standardized regressions for PortLoss, our demographic variables, and retirement concerns.

PortLoss was not significantly related to either longevity or liquidity concerns. Unfortunately, these two retirement concerns represent very real risks that individuals need to address as they select a retirement income strategy. Portfolio loss aversion does not provide the necessary specificity to address these risks nor provide significant insight into potential strategies. Portfolio allocation suggestions via an RTQ to address your longevity and liquidity concerns in retirement will miss the mark and make little sense.

Lifestyle concerns, however, were related to PortLoss. This is intuitive since this concern focuses on maximizing lifestyle with discretionary spending during retirement that may require capturing upside market potential. In other words, those seeking to maximize lifestyle are more tolerant of risk, or more amenable to relying on market growth to fund their retirement. The retirement literature emphasizes investing approaches that focus on the lifestyle goal, which matches the thought process of the RTQ.

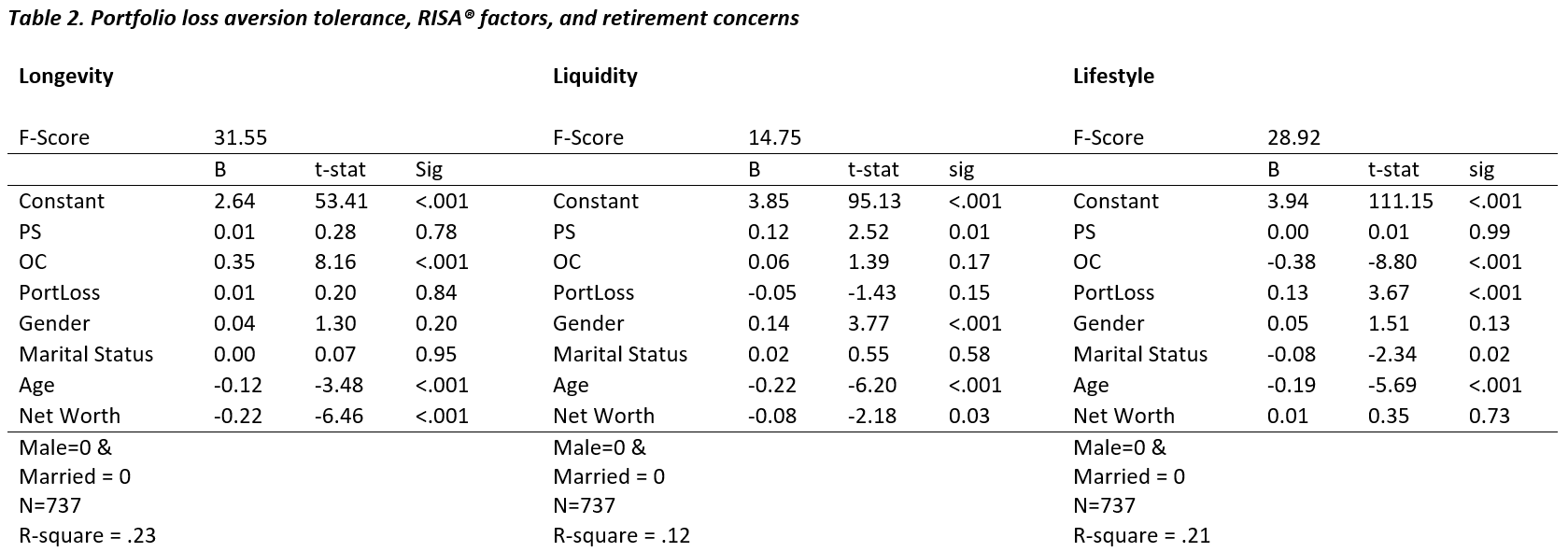

Table 2 presents the same analysis with the RISA® components and the PS and OC subscales added to the regression as independent variables. The RISA® subscales are significantly accounted for with each of the retirement concerns. These beliefs indicate that capturing these personal tradeoffs provide more insight into how someone feels about their ongoing retirement concerns and signals appropriate strategies to address them. Even when accounting for various demographic factors, the RISA® components remain significantly related to all retirement income concerns.

OC is significantly related to one’s longevity concern (b=.35, p<.001). The positive slope indicates a commitment orientation. It signifies a willingness to commit to a lifelong retirement income solution to reduce this longevity concern. These strategies include risk wrap and protected income. There is a focus on committing to an income floor because the security of having a dedicated retirement income solution outweighs missing out on potentially more positive future outcomes. There can also be satisfaction from planning in advance and not leaving difficult decisions for later, when your ability to make decisions may be hampered by stress or cognitive decline.

The significant PS relationship with the Liquidity concern (b=.12, p<.01) indicates a focus on safety first. Safety-first income sources incorporate contractual obligations and includes income protection and time segmentation as potential retirement income strategies. The income provided by these sources is less exposed to market swings. A safety-first approach may include protected sources of income such as defined-benefit pensions, annuities with lifetime income protections, or government bonds held to maturity. By earmarking specific assets with contractual protections to cover at least a portion of the retirement budget, it becomes clearer to these individuals what remains as excess reserve assets that do not have to be earmarked for retirement spending and can be a source of reserves for the unexpected. Those with concerns about liquidity will appreciate this delineation.

OC is closely related to lifestyle concerns (b=-.38, p<.001). The results indicate an optionality preference, which suggests that a total return strategy or time segmentation is a viable option for those concerned about lifestyle. Optionality reflects a desire to maintain flexibility to respond to economic developments or changing personal situations. This preference aligns with retirement solutions that do not have pre-determined holding periods and can be easily adjusted.

While PortLoss is also significantly related to one’s lifestyle retirement concern, one’s desire for optionality was more influential (b= -.38 vs .13, using normalized coefficients). The desire for optionality is more powerful than an RTQ in assessing which retirement strategy is a better fit to alleviate one’s lifestyle retirement concern. A portfolio allocation derived from an RTQ doesn’t signal potential sustainable withdrawals from a portfolio, whereas a high degree of optionality may indicate a range of potential sustainable withdrawal strategies.

Conclusions

Investing for retirement is inherently different and creates a new set of variables that need to be assessed. Instead of framing the decision with portfolio risk tolerance, we need to assess the tradeoffs that the individual is willing to make to address the new risks they face in retirement. Unlike the accumulation phase, during decumulation there is no singular metric for an advisor to optimize. Different retirees will have different concerns.

Retirement income preferences, as assessed through the RISA®, identify how one wants to source retirement income. Once the broader strategy decision is made, the RTQ can still play a role choosing the asset allocation for the investment piece of the strategy. But we need to understand the broader context for how the individual wants the investments to fit into the broad strategy.

Using the RISA® shaves off substantial time for individuals trying to navigate through the various retirement strategies. It will protect organizations overseeing financial professionals whose time is increasingly consumed with documenting the rationale behind recommending a solution that meets a given client need or preference.

Identifying these preferences allows us to better assess retirement income strategies that resonate with the individual. We can’t do that with an RTQ because it does not address the relevant issues and bypasses any strategy consideration. A RTQ implicitly assumes everyone wants to tether their retirement income strategy to the stock market. At best, and this is generous and assumes the only path to a retirement income strategy is to recommend a total return approach. And while this may be a viable approach for a significant subset of retirees, it ignores other viable and credible retirement income strategies such as time segmentation, risk wrap, and income protection.

Understanding your client’s retirement income style will let you build an effective retirement income plan that will make your clients comfortable. The RISA® makes sense of the many competing yet viable views about how to approach retirement income planning.

To learn more, we invite you and your associates to join us on October 25th and 26th for our Retirement Income Advisor Challenge. We will provide an in-depth review of our RISA® framework, provide an opportunity for you to take the RISA®, discuss how the RISA® can be mapped to various strategies and solutions, and demonstrate how to use it with prospects and clients. At the end of our challenge, we will launch the RISA® profile tool to the advisor community! But to have access to all of this you need to register and attend!

Click here to register.

Wade D. Pfau, Ph.D., CFA, RICP, is the director of the Retirement Income Certified Professional program at The American College. He is also a principal and director at McLean Asset Management, RetirementResearcher.com, and a co-founder of RISA, LLC. His most recent book is Retirement Planning Guidebook. He can be reached at [email protected].

Alejandro Murguía, Ph.D. is Managing Principal of McLean Asset Management, Retirement Researcher, and a co-founder of RISA, LLC. He can be reached at [email protected].

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All