How to Create an Advisory Board for Seniors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Picture from https://www.igniteag.com/complete-guide-to-starting-your-customer-advisory-board-in-2021/

Creating a special advisory board will foster a better understanding of the questions facing seniors as they plan for retirement.

Many people have not thought through their lives in retirement. Some seniors are being underserved and have questions that wealth managers can answer. Seniors are dealing with stressors they had not previously considered.

As an advisor, you have an opportunity to address the questions your older clients have about their next 20 to 30 years of life or more. Some in the advisory profession don’t fully know, appreciate, empathize, or even understand what those issues might be for their clients.

This was evident from the BCG Global Wealth Report 2021, which stated, “In the hurly-burly of working life, few individuals map their vision of retirement or think through the financial and nonfinancial concerns that attend its various stages. As a result, the changes that accompany a person’s golden years can make it a time of great opportunity and stress.”

The article went on to state, “That’s particularly true for individuals in the affluent and lower-end HNWI bands ($250,000 to $5 million in wealth). Individuals in these segments who are at least 65 years old hold $10.3 trillion in financial assets accessible to WMs, (35% of the total retirement asset pool), and they generate $13.7 billion in annual WM revenues. These individuals are especially impacted by the advisory gap in the decumulation phase. Their wealth gives them options, but it also introduces lots of questions, from tax and estate planning to broader life planning. Often, they have few reliable outlets to consult in trying to gather answers. And those that are available often require them to chase down specialists in particular domains, such as accountancy and estate lawyers – a time-consuming and often frustrating exercise.”

The article went on to state, “That’s particularly true for individuals in the affluent and lower-end HNWI bands ($250,000 to $5 million in wealth). Individuals in these segments who are at least 65 years old hold $10.3 trillion in financial assets accessible to WMs, (35% of the total retirement asset pool), and they generate $13.7 billion in annual WM revenues. These individuals are especially impacted by the advisory gap in the decumulation phase. Their wealth gives them options, but it also introduces lots of questions, from tax and estate planning to broader life planning. Often, they have few reliable outlets to consult in trying to gather answers. And those that are available often require them to chase down specialists in particular domains, such as accountancy and estate lawyers – a time-consuming and often frustrating exercise.”

Advisory boards for seniors

Advisory boards help you make decisions to ensure your strategies, solutions and services match your client’s wants and needs. They should answer the question, “Does what we are thinking about provide value to our clients?” While advisory boards can also build relationships, they are primarily designed to help you make good use of your resources and should not be used as a sales vehicle.

Most, if not all, client advisory boards have as an underlying value for business growth. Boards may be effective for that growth, but using an initial client advisory board development program with no ulterior motive other than to appreciate, understand, and service this specific subset of clients will definitely be effective. This will not only help you improve relationships with your senior clients, but it will also prepare you to understand and service the rest of your clients who will be fortunate enough to become seniors in their next 10, 20, or 30 years.

We propose a first senior advisory board investigatory meeting to determine the what and how of future board meetings, if any. The audience should be clients roughly 70 years old. Where possible, we strongly suggest couples as well as single women and men. Data shows 35% to 40% of the population are 70 plus years of age and 57% or so of those are women. If you have done a segmentation by age, you can know what your client data shows as well as the revenues and assets for that set of clients. I suspect you will find it enlightening and the data meaningful.

The details of how to construct client advisory boards are detailed in many articles, so we will focus primarily on the “why” of an advisory board and what to address based on this octogenarian’s beliefs and research.

Advisory boards typically have 8 to 12 participants. This senior board should include the full complement of 12 participants to get a good representation of the perspectives of your older clients.

Senior’s wants and needs

Most of you are familiar with Abraham Maslow, an American psychologist who developed his hierarchy of needs in 1943. This is a theory of psychological health predicated on fulfilling innate human needs in priority, culminating in self-actualization. Part of our research is based on the hierarchy and suggests that the seniors we generally work with are focused on:

- Level 2 – Security

- Level 3 – Sense of connection

- Level 4 – Respect and self-esteem, whether from self or others

- Level 5 – Desire to become the most one can be, a level of achievement, living well with aging in general and extending a healthy and happy life

Based on research, we believe there are nine key areas of primary concern to seniors:

- Establishing a purpose for the last third of your life – This is a broad subject on which much has been written such as, “The New and Improved Third Act of Life,” by Lawrence R. Samuel. . Samuel says while first two chapters of our lives follow previous generations of Americans, Chapter Three often involves creating something different and new options for seniors, e.g., going back to school, starting new relationships, exploring new careers, and perhaps bucket listing. What’s on your senior client’s agendas?

- Relationships with friends and family – According to the United States of Aging Survey, relationship needs outweigh financial concerns, as seniors simply want to spend their time with people they care about. Where does this need fit in your senior client’s lives?

- Education and lifelong learning – Where You Live Matters said, “Senior wellness includes mental workouts as well as physical workouts.” Developing new skills, physical and mental, can enhance personal wellness and even slow cognitive decline. The Great Courses, continuing education in local area, and One Day University are examples of opportunities. What do your senior clients do to maintain and improve their wellness?

- Health and wellness for establishing quality of life – Stress can contribute to poor mental and physical wellness. Discuss with your board what they do to keep both their minds and bodies in wellness. Do they meditate or use yoga to reduce stress? What exercising do they do to maintain physical wellness? What diets and nutrition protocols do they follow? How do they take care of their health?

- Intergenerational programs linking youth and older adults – Programs like family meetings, financial education programs, and family events such as a good old-fashioned ballgame both promote linking of families and friends together and build your intergenerational relationships. Would they be of interest to “your” senior clients?

- Technology – Both health and social technologies can be very important to seniors, yet many aren’t comfortable with them. Will helping them leverage these technologies such as health wearables, Facetime and Facebook be of interest?

- Travel – Travel is very popular with seniors. What types of adventures are of most interest to seniors? What parts of the world do they want to see while they are fit and able to travel? Are they interested in traveling alone, in groups, or with family?

- Security and safety – In today’s growing tech world, the need to protect ourselves against identity theft, and being taking advantage of in our online presence is critical. How important is this area to seniors? Are they concerned about their physical or home security?

- Financial concerns, this topic could make up your entire discussion, though we believe the above topics are as important to seniors as their financial wellness, e.g., retirement income, outliving their assets, health care costs, etc.

The financial topic is among many issues of concern. For this program, financial discussions can be left to individual clients and their advisors. Discussing money, insurances, etc. can make it seem that the focus of the Senior Board broaches the area of products and selling. This program is about value add and learning about the wants and needs of your senior community so you can serve them better. We hope that your business can grow because of the value add of programs that address topics such as these. We would not focus on addressing finances unless, or until, the Board wants more on that topic in a group form or you have specific questions you want help answering.

Senior advisory board meeting

The structure for this meeting would be a separate topic. We do want to address the purpose, and an agenda that addresses the approach to participation. The venue can be decided by the FA and team, but should obviously be in a quality location with appropriate refreshments or food.

Agenda and approach to participation

The agenda would also include a ‘fun’ introduction of participants so everyone can get to know each other.

The times and style of the meetings are flexible given the nature of the senior attendees. You may consider a brunch buffet on the weekend or a weekday, a lunch meeting or an afternoon meeting with appetizers and beverages, etc. Your geography, clients, and other factors can determine what’s best for your clients and your team. Select a few potential client participants to talk about the idea and the times, days, and styles that would be of most interest to them.

- Arrival

- Time A to Time B – Social time (30 minutes)

- Personal welcomes and mingling

- Refreshments and beverages

- Time B to C – Instructions by team (15 minutes)

- Discuss purpose and plan of meeting, introductions format, introductions by advisor team members

- Introductions Format – Select a subset of questions from these examples:

- Name

- Where were you brought up?

- Best lesson you learned in life to date?

- Views on the present state of the world and biggest need?

- Thoughts on biggest changes in your lifetime?

- What made you happy this week or month?

- Biggest changes you see in the next 10 to 20 years?

- How would you like to be remembered?

- What do you do for fun?

- What is a new skill you would like to learn?

- What are you most proud of?

- What is a most interesting thing in your life that shaped you?

- What lesson would you like to pass on to future generations?

- We suggest narrowing this set of questions or you can choose to send them out in advance to gather important client information. Much of this will be useful for follow up discussions also.

- Time C to D – Introductions by clients (60 minutes)

- Plan is 5 minutes per couple or individual attendee

- Time D to E – Discussion and completion of questionnaire below (30 minutes)

- The objective is to select topics for future Board Meetings as well as to identify events/speakers that would have broad appeal to Board members, their friends, families, and neighbors

- Time E to F – Conclusion, Summary, Social Time (Open)

Future advisory boards for seniors would have a different agenda to focus on the content your clients are most interested in along with different questions that may help you improve your practice for other seniors.

In summary

The purpose of your ongoing senior advisory board is to better understand the wants and needs of your senior clients and deepen the relationships with this group and all the rest of your clients who will all hopefully become your senior clients.

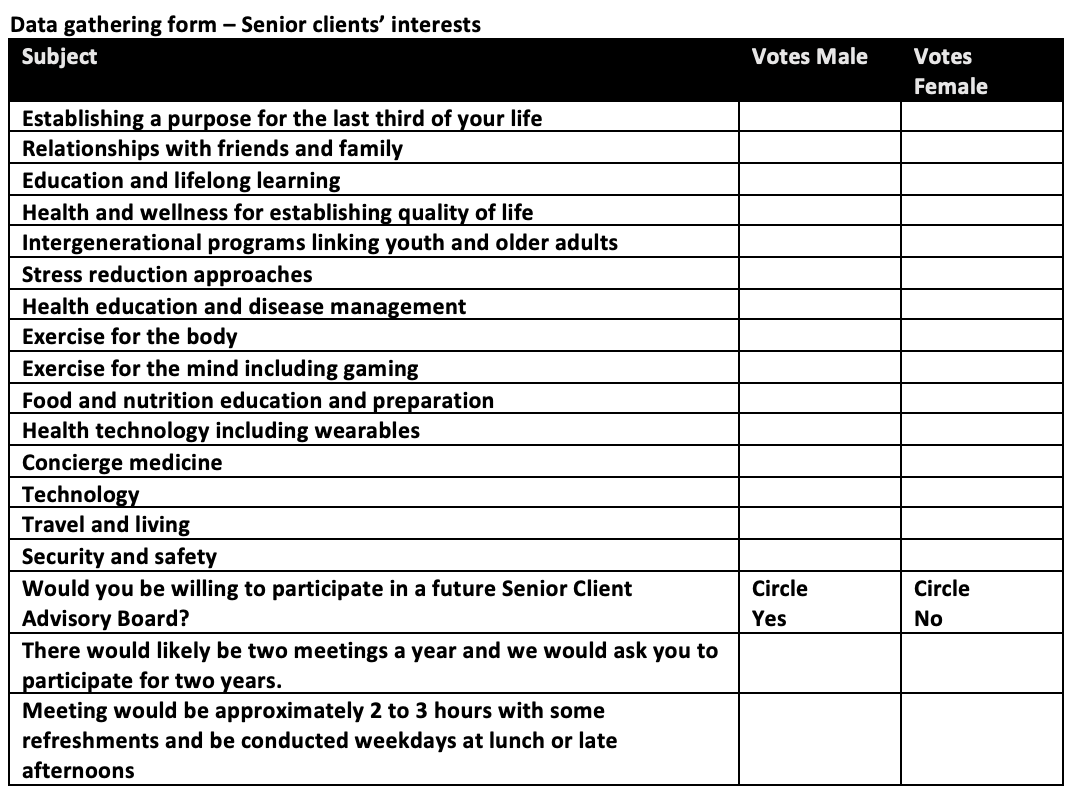

The agenda above focuses on your clients. As their advisor you can learn more about them through their self-introductions and the use of a written survey to gather data. Following our bios is a data gathering sample based on the topics outlined in the agenda.

A senior advisory board may be one of several advisory boards you may want to consider based on your practice focus. You may want advisory boards that focus on other age groups or niches that are important to your business.

There are many benefits to advisory boards including more brains equals more ideas, getting perspectives from outside of your focused thinking and into the thinking of those you serve, as well as validating your thoughts and ideas before making investments. As importantly, advisory boards make your clients feel more ingrained in your practice, leading to higher retention and qualified introductions.

David Leo is founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant, and trainer to financial professionals. David is an experienced business manager who works solely with Financial Advisors, Planners and firms who want to organize, structure & grow their businesses by attracting, servicing, and retaining affluent clients.

If you would like additional details or have any questions about his articles or an interest in coaching schedule a free 45 Minute Strategy Session @ https://calendly.com/davidileo or contact him @ [email protected]. Call 212-598-4229 (Office) or 917-379-1249 (Cell) and visit @ www.CoachDavidLeo.com.

Michael Silver is founder and managing partner of Focus Partners. Michael is a speaker, coach and consultant who has worked with financial services firms and financial professionals (solo producers and advisor teams) for the past 28 years.

Feel free to modify anything in the agenda or questionnaire that best fits your practice.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All