How Market Timing Destroys Wealth

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

So-called “experts” are telling us about the coming uber-bear or why the bull market will continue. Yet the data show that trying to predict the market’s direction to time buys and sells is the wrong approach to investing.

Data from the last seven bear markets show that a large percentage of losses and gains happen in very short periods of time, requiring timers to have uncanny accuracy and resolve. Investors are better served to ignore market calls and follow the time-tested practice of holding well-diversified portfolios that meet their goals across long market cycles.

We are barraged with information about the market and its expected direction. Are we in a bull market or about to enter the worst bear market in history? There is no shortage of opinions, analysis and debate. I enjoy reading some of these analyses. But is it information that investors should use to inform their investment decisions?

The brilliant neurologist, financial advisor to high-net worth individuals, and author of several excellent investment books, William Bernstein, cautions about paying too much attention to stock pickers and market timers in what he refers to as “financial pornography.”

I decided to revisit the research on the track record of market timing and perform my own empirical analysis of data from the last seven bear markets. The results show that market timing is an elusive pursuit.

Research on market timing shows a dismal record for practitioners

Let’s look at average investors’ track record. According to research cited in a 2012 Barron’s article, 85% of sell or exchange decisions that investors make are wrong. More recently, according to IFA, a research report by Dalbar said the typical mutual fund investor earned 5.96% per year in the 20 years through 2020, compared to the S&P 500 index return of 7.43% per year.

The excellent book, Asset Allocation, by Roger Gibson, says that for market timing to pay, investors must predict the market correctly at least:

- 80% of the time for bull markets and 50% for bear markets; or

- 70% of the time for bull markets and 80% for bear markets; or

- 60% for bull markets and 90% for bear markets

Not only have individual investors been burned, but so have professional pension fund managers. Gibson cited the book, Investment Policy, referencing a study of 100 pension funds:

…their experience with market timing found that while all the funds had engaged in at least some market timing, not one of the funds had improved its rate of return. In fact, 89 of the 100 lost as a result of timing and their losses averaged a daunting 4.5% over the five-year period.

But what about market timing gurus? Wim Antoons, author of the paper, Market Timing: Opportunities and Risk, cited research by the CXO Advisory Group. It showed predictions from 68 market timing experts between 1999 and 2012. The majority (62%) were accurate less than 50% of the time. He also looked at 6,582 forecasts between 2005 and 2012 and found that after transaction costs, no single market timer was able to make money.

A look at bear markets since 1987

The main benefit of market timing is to enhance returns over buy and hold by avoiding severe downturns and getting back in when the bull resumes. To assess its efficacy, I will focus on bear markets. To obtain more current data, I slightly stretched the arbitrary bear market definition of a 20% decline by including the 19%+ declines of 1998 and 2018.

Five of seven bear Markets were very short, requiring uncanny timing

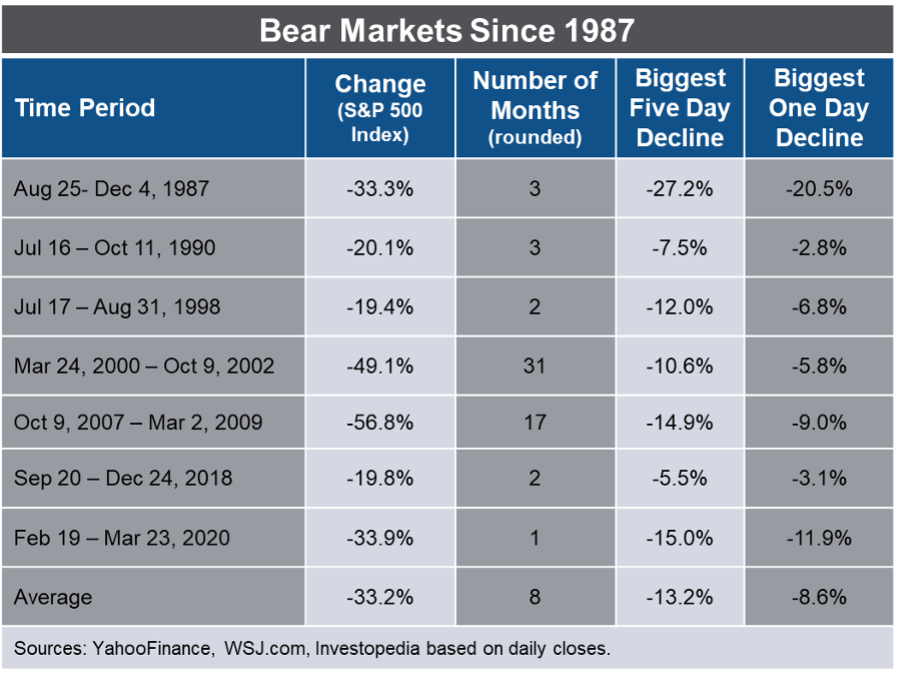

The table below shows an overview of the last seven bear markets, beginning with the flash crash of 1987.

Key takeaways:

- Five of the seven bear markets were very short, with a duration of 1-4 months.

- Six of the seven bears experienced sharp, double-digit declines over a five-day trading period. If you timed it wrong and were in the market during the worst five-day period, you would have incurred 40% of the total losses.

- Six of the seven bears experienced one-day declines of more than 5%, with two of them experiencing double-digit single-day declines. The 1987 bear included the granddaddy of them all on October 19th, down 20.5%.

Market timers needed to be nimble and accurate during these events as the market shifted direction very rapidly and violently in both directions (more on this below). The largest and most severe bear markets, the Y2K bust and the great financial crisis, were multi-year events. Had a timer been able to correctly navigate those two events, the rewards would have been substantial, protecting as much as half of an investor’s capital. Of course, brave investors willing to short would have done even better.

A large percentage of market swings occurred in a span of 40 trading days

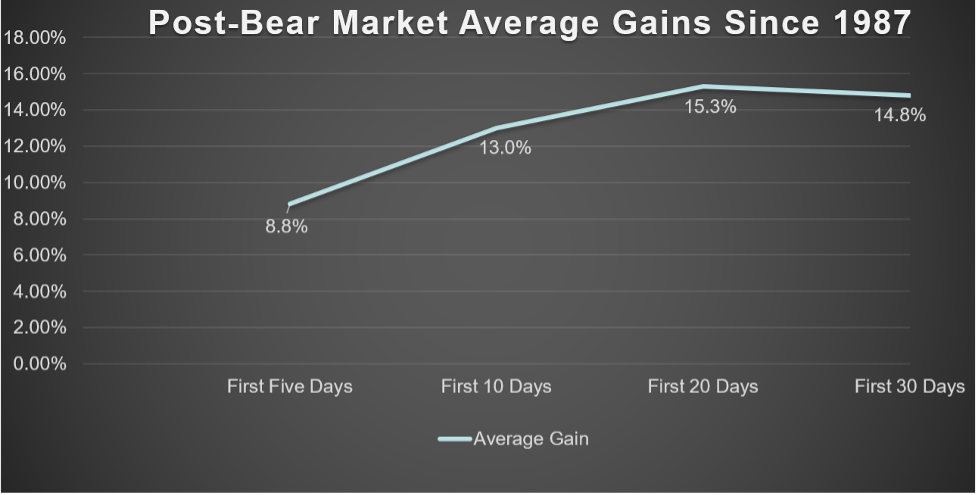

The charts below show that market timers would have to be very accurate over a relatively short period of time to be effective.

The average bear posted a loss of 8.1% in the first 20 trading days and 9.6% in the first 30 trading days. On average, the initial 30 days comprised 34% of the total bear market decline. The average percentage of total decline was less for the two longer bears of 2000-02 (14%) and 2007-09 (8.8%). But the five short bear markets experienced almost half (44.4%) of their total declines in the first 30 trading days.

In mirror-image fashion, after bear markets ended, the S&P 500 was up significantly and quickly – by an average of 15.3% in the first 20 trading days and 14.8% in the first 30 days.

Indeed, in his book Roger Gibson stated:

Much of the problem with market timing is that a disproportionate percentage of the total gain from a bull market tends to occur very rapidly at the beginning of a market recovery. If a market timer is on the sidelines, they will miss much of the action.

Further supporting the idea that missing “up days” is harmful, the 2021 J.P Morgan Asset Management Guide to Retirement showed that S&P 500 index buy-and-hold investors earned 7.47% per year from 2001 to 2020. But investors who missed the 10 best days during that period earned only 3.35% per year. Even worse, if they missed the 50 best days over 20 years, they lost 5.21% per year.

Returning to our data above, the first 20 bear market days and first 20 post-bear days combined represented more than 23 percentage points of investment return at stake. It would take an extraordinary trader to capture this successfully on both selling and reentry.

And if market timing was the way of life for an investor, they would need to do this repeatedly over time to beat a buy-and-hold approach. For each cycle, a timer would have to be right twice to reap the rewards. For someone with at least a 34-year investment career, as represented by this sample, that’s at least 14 major transactions (two for each bear). And that assumes their trading system has the minimum, perfect level of trading activity, which is highly unlikely. Adding more trades would introduce an even higher margin for error or stated conversely – increase the need for accuracy.

Not only that, a market timer would need the conviction to make bold moves with their money. They’d be selling at tops when the market was giddy and buying at the bottoms under the most stressful conditions in history. Not many investors can do this psychologically.

Not all bears look alike

This analysis should be tempered by the fact we have only seven sets of data points. Averages can be deceptive, especially without a lot of data points. When you’ve seen one bear market, you’ve seen…one bear market. Therefore, let’s dig into specific bear markets to see what they tell us.

The 1987 crash featured the infamous October 19th one-day drop of 20%

Most students of market history know the 1987 bear was short and severe, with the main event occurring on October 19th. However, many won’t remember that the bear started at the market top of August 25th. Five trading days later the market had dropped only 3.9%. Thirty trading days later the market was down only 4.8%, hardly a distinctive bear market.

Then the October 19th massacre hit, accounting for 61% of the total bear market drop. Some market historians blame that on program trading. Robert Shiller concluded it was purely due to investor psychology. Regardless of the cause, how many prescient timers would have gotten out on August 25th or even just before October 19th? And how many would have bailed out after their indicators were tripped by that one--day debacle and not gotten back in soon enough? Indeed, the market rallied 11% in the first 10 trading days after the bear was over.

The 1990 and 1998 short bear markets had similarities

The 1990 bear market was characterized by a slow, steady downturn with few sharp moves over three months. The most significant was a drop of 7.5% over five trading days. The 2018 bear market was similar in terms of being steady but short, lasting only two months. Any timing system would have had to be sensitive enough to spot these more subtle, persistent, yet short bears.

The dot-com bubble bear was brutal and was a good timing opportunity, but hard to capture

The 31-month dot-com bust presented a good opportunity for timers to make money. Had a timer been able to get out at the March 2000 high, they could have protected the enormous 1990s bull market gains (assuming they were steadily in the market) and redeployed their money more profitably elsewhere. That bear had modest early moves, with the market down only 1% after the first 10 trading days and 7% after 30 trading days. And the potential benefits of correct timing were high – a total loss of 49% over the period. However, reentry posed a significant challenge. In October of 2002 the market was up 11% in the first five trading days and 15% after 15 days. Looking further out, had investors stayed on the sidelines, they would have missed gains of 28% in 2003.

The great financial crisis bear came on slowly, accelerated and turned on a dime

The 2007-2009 bear had similarities to the dot-com bear in terms of speed and degree. Losses after the first 10 trading days and 30 trading days were only 3% and 5% respectively, yet total losses tallied 57%. Again, a successful timer had the opportunity to do well without being as precise on market exit. However, after five and 10 days post-bear, the market was up 12% and 22% respectively. Again, market timers were challenged to make two precise calls to beat steady, boring, buy and hold investors.

Timing the pandemic bear was like capturing lightning in a bottle

The 2020 pandemic bear was perhaps the most unique and bizarre in history. It was severe, down 34%, and short, lasting just over a month. After the first 10 trading days the market was down 8% and after 20 days, down 29%. Had a timer been 15 days late calling the bear start, they would have failed to avert 15% – almost half – of the total losses. On the other side, had they been late calling the end of the bear by only five trading days, they would have missed gains of 17%. Twenty days after the bear was over the market was up 22%. The market continued to power higher and went on to recoup all its losses in about six months and continues to make new all-time highs. Suffice it to say, these wild swings were highly unpredictable. It would take extraordinary powers to call them and unmatched fortitude to move large sums of money under such historic duress.

Conclusion

The data show that market timing is an elusive pursuit. While it can be enticing to act on advice from convincing market forecasters, it is hazardous to your investment health. Yet, many individual investors, hedge funds, pension funds and professional traders act on this information. Some have success – at least for discrete time periods. But it’s highly unlikely it will work consistently and profitably over the long run.

After learning my own lessons over 40+ years of investing, investors should set their investment goals, determine an appropriate investment plan and asset allocation, and stick with it for the long term. Changing life circumstances and risk-reward preferences play a role and warrant periodic adjustments. But the evidence persuasively demonstrates that making wholesale and frequent buys and sells of stocks based on market forecasts is a losing strategy.

Nonetheless, I will continue to follow what a select few think about the market – but only for entertainment purposes.

Ralph Wakerly is president of Wakerly Partners, Inc. He advises and manages family investments, including a private, not for profit foundation. He is a contributing author for Seeking Alpha and has an investing website www.ralphwakerly.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All