Next-Generation Business Development and Services

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The rationale for putting a strong and comprehensive plan in place to serve the next generation of investors is simple. An article on CNBC stated:

- For financial advisors, the transfer of wealth from baby boomers to heirs over the next two decades is a bit like climate change: The consequences may eventually be huge, but it’s easy to ignore the issue in the short-term.

- Cerulli Associates estimates that as much as $68 trillion will move between generations within 25 years.

- Most studies suggest that 80% or more of heirs will look for a new financial advisor after inheriting their parents’ wealth.

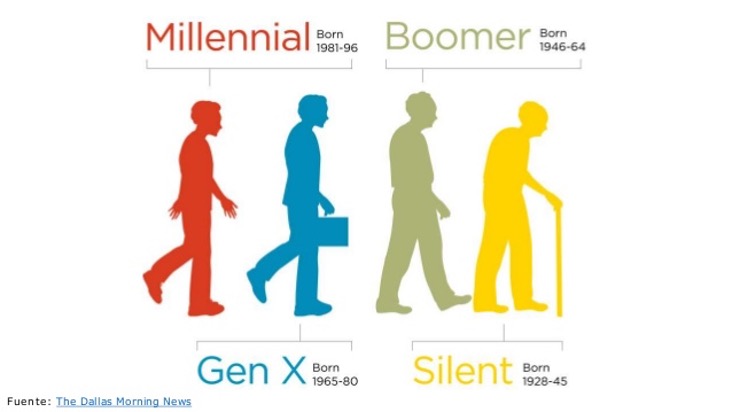

A tremendous amount of money will flow over the next 25 to 35 years or so from about 70 million Boomers (born 1946 to 1964) to about 65 million Generation X adults (born 1965 to 1980) and/or the Millennial Generation (born 1981 to 1996).

About 60% of affluent investors met with their first financial advisor before the age of 45. This means you have already potentially lost a great share of today’s younger Generation X prospects.

Ideally, financial advisors need to establish relationships with millennials before they reach the age of 35. In the referenced CNBC article, Peter Mallouk, head of RIA Creative Planning, said, “I expect we’ll see a tipping point in the industry in about five years,” and “The industry is unprepared for this wealth transfer.”

Mallouk’s firm has a leg up on most advisors in this regard. Creative Planning is regularly involved with setting up trusts and financial plans involving multiple generations for its ultra-high-net-worth clients. “We do a lot of legal work involving multi-generational estate planning, so that gets us involved with kids,” he said. “Not a lot of advisors do that kind of work.”

Key points:

- You may already be late to the game of next-generation business development and services; and,

- Some of your competitors are already focusing on having your HNW clients’ assets transferred to their firm’s advisors.

What to do

While rationale for putting a plan in place for the development and servicing of next generation of investors is simple, the plan is not.

A robust next generation plan involves working with at least three age groups with varying degrees of emphasis on each:

- High-school age

- Their interest in financial skills are very limited. It’s just not what they are into. Given a choice of their smartphones, friends, music, social media, video games, hobbies, sports and more, understanding finances will take a back seat.

- Having said that, most high school students are also motivated to learn. The vast majority do report being motivated to apply themselves in school by thinking, listening, and completing assignments. In their last two years of high school they are interested in colleges and preparing to leave their parent’s homes.

- Though it may not be top of mind, high school students need to understand how to stay out of the most expensive forms of debt: long-term student loans, depreciating car loans, high interest credit cards, etc. But they also need to understand when to use debt and how to manage it wisely.

Ideally, they should at least know about:

-

-

- budget and banking basics

- How much things actually cost and value versus cost

- What family finances look like and basic life skills

- Why saving is more satisfying than instant gratification

- Wants versus needs and saying no

- The value (and fun!) of a part-time or summer job

- Giving back

- How to save for/on college

- Why healthy choices lead to wealthy lives

- How to protect their identity

- Bill paying

- Investing basics and long-term planning

-

This is a huge list and is too much to absorb for a 16- to 18-year-old in a single session. Of course, parents have a big role in sharing these topics with their children. While many do, parents are also in overload and may not have the structure to help their kids. This is an opportunity for you to help kids and their parents.

-

- Offer events that address the above subjects. They can be online and/or in-person. For maximum attendance, we suggest online classes which would be available on demand. For maximum relationship building, we suggest in person meetings. We will discuss an important step of “inventorying” your clients to understand where you should deliver in-person events.

- College age

- Their interest in financial skills are limited but are much more important as they are preparing for the world on their own. College students are often in overload with school, their social lives, personal interests including friends, music, and sports, not to mention sleep. Time is at a premium.

- Having said that, most also remain motivated to learn. They are in school to think, listen, and learn to prepare for their current and next phase of life - the real world as they are learning about it. In their last two years of college they are interested in preparing to either go on to graduate school and more often get ready for the working world. Perhaps they will take a period to travel.

- Though it may not be top of mind, college students need to understand the same things as above for high schoolers with a focus on:

- Debt

- Budgets

- Wants versus needs and sacrifice

- Renting apartments and bill paying

- Investing basics and long-term planning

Ideally, they should also know about preparing for life’s next experience, specifically work. Skills like:

-

-

- Resume and cover letter preparation

- Approaching job interviews

- Networking

- Interviewing

-

-

- A great way of helping and getting to initially meet the college age children of your clients is also offering events that address the above subjects. They can be online and/or in-person. For maximum attendance, we again suggest online classes which would be available on demand. For maximum relationship building, we suggest in person meetings. We will discuss an important step of “inventorying” your clients to understand where you should deliver in-person events.

- Post college to age 40

- This is the group on which to focus because about 60% of affluent investors met with their first financial advisor before the age of 45. Other data reported that thirty-three percent who have met with a financial advisor first did so before the age of 35, and 26 percent had that first meeting between the ages of 35 and 44.

- You should approach the next generation of your clients now!

- For this group, money is now top of mind. They are thinking about family, homes, various big ticket purchases, and their future as yet perhaps not clearly defined, e.g., retirement which may be 40 or 50 years away. This group also needs to understand:

- Debt

- Budgets

- Wants versus needs and sacrifice

- Saving

- Financial planning for both the current, mid-, and long-term

- The range of wealth management services

- Investing and its many options

- Insurance

- Trusts and estates despite the relative youth of many millennials

Where to start and who are your best millennial prospects

Your first step is to “inventory” your clients to identify your ideal millennial prospect.

- Which clients have children 35 years of age or younger? The ideal millennial prospect is one who will likely inherit at least $1 million over the next number of years. This is a function of their current age, the age of their parents, and the projected future AUM of the parents. For example, parents who are 70 with four adult children and an AUM of $1 million are less likely to inherit large sums of money than a 50-year-old client with two teenagers and an AUM of $3 million. An inventory will give you raw data for further analysis.

- If your inventory shows potential and/or you believe you can attract children from adults who are not your clients, start building your multi-part program focused initially on education. Your prospects, people on your newsletter list, children of colleagues, family members, neighbors, religious affiliations, and many more offer opportunities for attendance to your educational offerings.

- Do you have a very good relationship with the parents? Do the parents have a very good relationship with their children? Are the parents willing (and even happy) to have you work with their children?

- While 70% to 80% of adult children approximately 28 to 32 years of age have not yet met with a financial advisor, this is waiting too long to start to build a next-generation business development program. You need to start while children are young to show the parents and the children you are interested in them and want to be of service.

- You should have built a base with the younger children of HNW clients, you may then have a basis for having individual conversations with HNW potential adult children of HNW clients and prospects.

- Your target audience are children that have or will most probably be a college graduate.

- The adult children will be employed in a job paying over $60,000, for a recent college graduate, and close to $100,000 for older millennial prospects. They should have the prospect of a six-figure job before reaching 35 years of age.

- They will possibly be an attorney, manager, high profile CEO, physician, entrepreneur in the tech sector, or software developer.

- Your best millennial prospects will be ambitious, savers, and entrepreneurial individuals with social and/or philanthropic interests. This will be part of your evaluation during discovery conversations.

Each of these factors is part of your discovery process by which you get to know your clients and their families. This is especially important with your high-net-worth clients — those whose assets you would like to retain in perpetuity.

Next steps

With your target market in mind, you must develop a set of programs for the three groups mentioned:

- High school age millennials – We envision three approaches:

- Online programs, e.g., semi-annual programs with monthly reminders of replays

- In-person programs, e.g., annual events using outside speakers where appropriate and available, e.g., Selecting the right college

- Email drips

- College age millennials

- Online programs, e.g., semi-annual programs with monthly reminders of replays

- In-person programs, e.g., annual events outside speakers where appropriate and available, e.g., Resume preparation, interviewing skills

- Email drips

- In-person meetings with high potential millennials

- Post college to age 40 millennials – most of these programs should center on in-person meetings.

- Special in-person programs TBD based on the above stated needs

- Email drips

- Most importantly, in-person meetings with high potential millennials

Also think about each program’s need for and use of:

- Invitations and thank you for attending notes

- Regular personal cards and notes for occasions with invitations to contact you and words that show caring

- Birthday cards that are personalized

- Discovery formats to learn about interests and hobbies to post to your CRM

- Occasional gifts such as books with important messages, e.g., “The Go-Giver”

Delivery of each of these programs involves similar requirements as any event such as using technology, venues for in-person meetings, invitations, follow ups, etc.

To secure attendance think about incentives, door prizes, speakers, etc.

Get your millennial strategy in place, and if you collaborate with the right ones, they can grow into optimal long-term clients. Identify those clients who have children falling into the various age ranges mentioned above build robust programs to meet, educate and curate them into clients.

David Leo is founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant, and trainer to financial professionals. David is an experienced business manager who works solely with Financial Advisors, Planners and firms who want to organize, structure & grow their businesses by attracting, servicing, and retaining affluent clients.

If you would like additional details or have any questions about his articles or an interest in coaching schedule a free 45 Minute Strategy Session @ https://calendly.com/davidileo or contact him @ [email protected]. Call 212-598-4229 (Office) or 917-379-1249 (Cell) and visit @ www.CoachDavidLeo.com

Michael Silver is co-founder and managing partner of Focus Partners. Michael is a speaker, coach and consultant who has worked with financial services firms and financial professionals for the past 28 years.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All