Immunizing Your Mind and Portfolio

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

What if it were possible to immunize yourself from market volatility? Thankfully, it doesn’t require a vaccination. Rather, it demands a prudent investment strategy to help investors ride out and mentally endure inevitable and often painful stock market declines.

As a retirement specialist, I will address how to immunize retirement assets. They are irreplaceable and most in need of a strategy to help enhance their longevity. Immunizing a portfolio provides a reliable source of income in retirement. This strategy involves two essential and united elements: 1) maintaining ample cash for withdrawals; and 2) providing confidence and security in retirement.

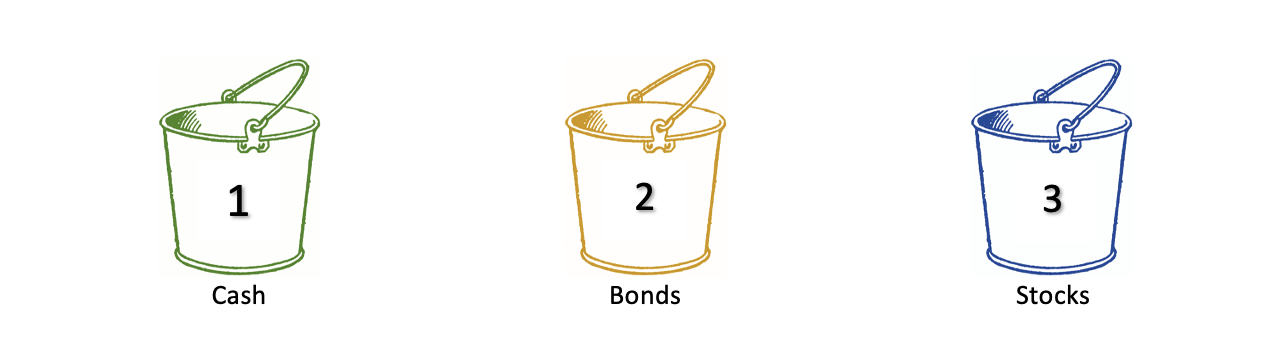

Imagine within your overall retirement portfolios there are three separate and distinct buckets:

- The first bucket is filled with cash. This is money that is going to be spent in the near-term, generally from now up to two years into the future.

- The second bucket is filled with bonds. This is money that is designed to be spent beyond the two years provided by the first bucket.

- The third bucket is filled with stocks. This is money that is for the long-term and is not going to be spent for many years to come, thus giving it ample time to grow.

The first two buckets form the foundation of money to draw on for income in retirement. The third bucket supplements the first two as needed. When the cash in the first bucket runs low, money is “poured” from the second bucket to replenish it. When the second bucket needs more bonds, money is “poured” from the third bucket to top it off. Therefore, a constant stream of money is readily available for the retiree to spend and enjoy in their retirement.

Each bucket’s purpose is instrumental in providing longevity to the portfolio. The first bucket’s job is the most obvious – security and liquidity. Cash serves those purposes well. It’s essential to have sufficient cash to satisfy the immediate needs of the retiree. While this bucket is designed always to be full, a delicate balance must be struck between liquidity and missing out on potential gains. Historically low interest rates mean less interest on cash. Therefore, it’s important not to hold too much cash. Finding a sweet spot is part of the overall investment strategy.

In the second bucket, the role of the bonds is to earn interest, provide stability to the portfolio, and create a cash flow to constantly fill the first bucket. A bond is simply a loan an investor makes that comes due at a set point in the future. The strategy therefore purchases bonds that come due at specifically targeted points in the future. This provides years of reliable income. Imagine you’re on a football field and every yard line there is a bond waiting for you. As you walk forward on this football field of life, you pick up a bond and turn it to cash. Take another step forward and pick up another bond, again turning it into cash. This is the role of the second bucket.

The third bucket is used to grow the portfolio. This bucket is comprised of stocks and other long-term investments. You might be asking – why the third bucket? Answer: growth. Growth in the value of the stocks in the third bucket provides the profits that will be skimmed off to replenish the bonds in the second bucket. This is achieved with an investment strategy designed to take advantage of the propensity for stocks to grow over time. Short-term trading and timing the market with this strategy become less effective than a durable long-term approach. Simply put, the longer you are invested, the higher your probability of making money in stocks.

From 1926-2020, the stock market (as represented by the S&P 500) over any three-year period has been positive 84% of the time. That means, so long as you held stocks for three years, you had an 84% chance of making money. The probability of making money rises to 88% for five-years, and 95% for 10-yearsi. This illustrates why stocks should not, and need not, be sold for income, out of fear of market declines, or to try to time the market in the short-term. You wouldn’t plant an apple tree and cut it down before it bears fruit. This is the same idea in investing in stocks – planting the seeds for future harvests.

Staying invested in stocks for the long run should bear such fruit. From 1937-2020, the S&P 500 gained value in 63 of those years, and lost value in 20ii. That means you’ve made money in the last 83 years in stocks 76% of the time in any given year. Interestingly, not only have positive years occurred three times more often than negative years, but the positive years were better on a relative percentage basis. The average positive year was up 19.6%, and the average negative year was down -12.2%. The best of those years was 1954 with a 52.3% return, and the worst was 2008 with a -37.0% return. A vastly wide array of outcomes is possible in any given year, but the best way to make money is to stay invested over the long run. No investor, particularly retirees living off their investments, wants to endure another painful 2008 scenario. However, missing market rebounds by abandoning a sound strategy is a surefire way to damage portfolio returns in the long-term.

This second part of immunizing a portfolio is equally if not more important – providing the retiree with confidence and a sense of security. Even the most seasoned investors can and will feel fear when markets drop dramatically. The difference between these sage investors and less successful ones is they don’t lose conviction in their strategy nor lose sight of their objectives when markets inevitably turn volatile. Moreover, knowing that stocks often turn volatile will help retirees mentally and emotionally brace for this eventuality.

Understanding normal drops in the stock market helps investors better prepare for the impact. Since 1980, the S&P 500 experienced a decline of -14.3% at some point during the year iii. That was not the overall return for the year; instead, it was what has happened during the year. Simply put, the stock market frequently experiences declines. Acting on the emotional temptation to abandon the markets and run to the perceived safety of cash when stocks drop can permanently damage a portfolio. It’s a constant reminder why immunizing yourself and your portfolio to market volatility is so vitally important. With this bucket strategy, market volatility can be simply waited out until stocks recover. Prolonged losses in U.S. stocks are uncommon.

Sadly, too many investors fall victim to their emotional need to act instead of staying the course with a prudent investment strategy. As a result, from 2001-2020 the average investor dramatically underperformed both the S&P 500 and a balanced mix of 60% stocks and 40% bonds (also known as a 60/40 portfolio). During this timeframe, the S&P 500 delivered 7.5% per year, a 60/40 portfolio delivered 6.4% per year, and the average investor eked out a paltry 2.9% per yeariv. That may not come off as a significant difference at first glance, but over time that adds up to a truly staggering amount. $1 million in the hands of an average investor over that timeframe would be worth $1,771,363 at the end of 20 years. A 60/40 portfolio would be worth $3,458,060 – almost double the amount. The S&P 500 would’ve grown to $4,247,851. This is why staying invested with an immunized portfolio during market distress should lead to far better outcomes.

While it may be emotionally difficult to stay invested when markets plunge, arming yourself with the knowledge of how markets have historically behaved should help you weather any storm. In our view, the risk of outliving your money without a prudent strategy in place is far greater than the risk of the markets. As we discussed, the markets have a track record of resiliency and the ability to recover losses. However, there’s no coming back from running out of money. Therefore, having a durable portfolio strategy and financial plan can help retirees achieve the retirement they’ve always dreamed of. For a retiree with an immunized portfolio, when stocks decline, they know they should not worry. That feeling is priceless.

Michael J. Graziano, CFP®, CMT®, CRPC®, is chief investment officer of Graziano Budny Wealth Management, a Greenwood Village, CO-based wealth management firm.

iSource: Graziano Budny Wealth Management

iiSource: Legg Mason

iiiSource: J.P. Morgan Asset Management

ivSource: J.P. Morgan Asset Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All