Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

“Banks have conditioned us to trust them and what have we got from that?” – Mark Baum (Steve Carell)- The Big Short

In his book and movie, The Big Short, Michael Lewis tells the story of a few intelligent and courageous investors who saw what no one else wanted to see. Instead of turning a blind eye to absurdity, they did their homework. What they quickly found was many subprime loans were likely to default. These investors were laughed at by Wall Street’s “best and brightest” simply for betting on an obvious truth.

Myopia and fat profits clouded the ability of many investment professionals to see the housing bubble. Worse, well-educated PhDs at the Fed, charged with preventing financial instability, had the same blind spot.

Now, a decade later, a much larger problem is brewing. Once again, those on Wall Street and the Fed do not see the debt elephant in the room. Even worse, they see it but ignore that perpetuating the problem serves their interests best.

Spotting The elephant

In 2008, the sub-prime mortgage market crashed for several reasons. Chief among them, borrowers were ill-equipped to make mortgage payments if interest rates rose and/or incomes were compromised. Equally problematic, the collateral (home prices) backing the loans were grossly overvalued.

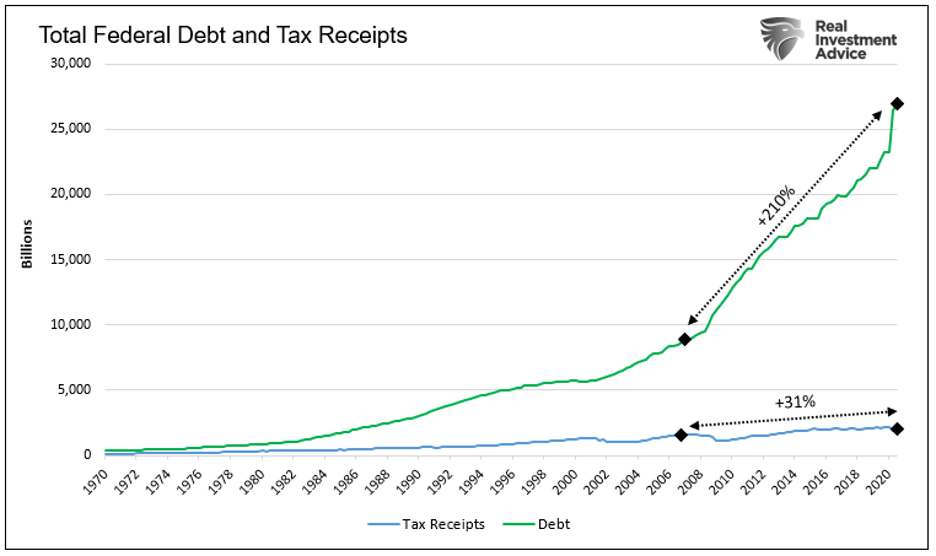

Federal debt, while vastly different than private debt, is equally unsustainable. The graph below quantifies the fiscal problem.

Over the last 15 years, debt has grown at seven times the rate of tax receipts and more than four times faster than economic growth. The divergence between federal debt and the ability to pay for it accelerated during the subprime crisis and is accelerating again due to pandemic-related multi-trillion-dollar deficits.

Are the odds of perpetually increasing the gap between spending and tax revenue any better than the Miami exotic dancer, featured in The Big Short, making good on her loans on five houses and a condo?

While the problem is obvious, the Fed, government, and just about every banker opt to ignore it. Even those who understand the problem tell the public now is not the right time to address it. There always is a more pressing issue requiring more debt which perpetuates the problem.

No one wants to solve the deficit problem because the cost of fixing it involves short-term financial and economic pain. The hurt is too detrimental to the careers, wallets, and egos of bankers and politicians.

To answer my question comparing Uncle Sam and the Miami dancer: No, the odds are similar, but the government has a much longer runway to perpetuate its shenanigans.

Responsible ways to deal with federal deficits

I could write pages on the many ways the government could reduce deficits. Why bother? It is a waste of my time and yours. The answer, some combination of higher taxes and reduced spending, is a pipe dream. Politicians’ intent on holding office know higher taxes reduce the chances of reelection and showering government funds on the public wins votes.

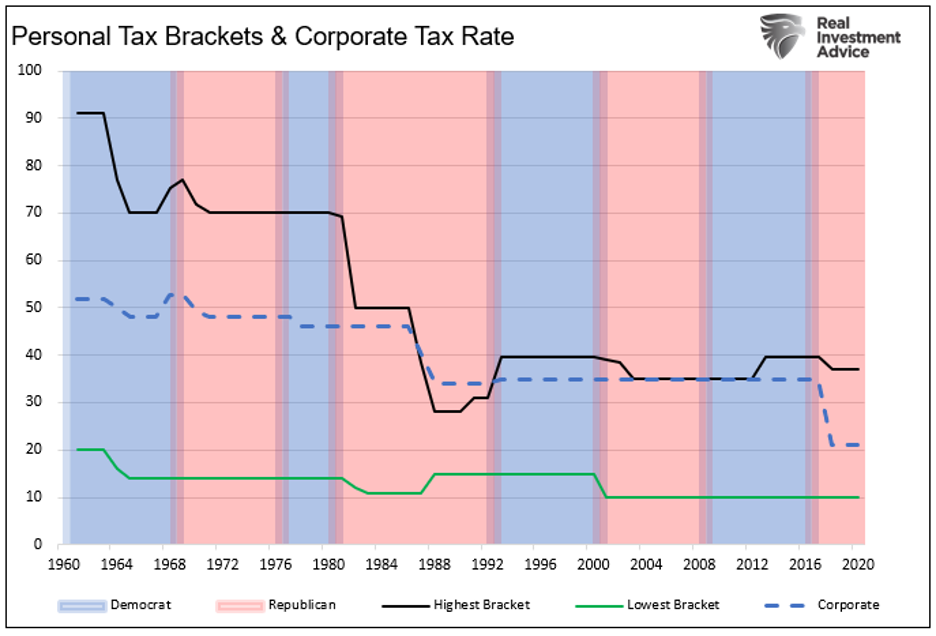

The graph below shows over the last 50+ years, personal and corporate tax rates have trended lower. Both Democrats and Republicans have presided over lower tax rates despite increasing shortfalls between tax revenue and debt.

Enter the magician

If the government intends to spend at an increasingly greater rate than tax revenue growth, a new funding source is required. Traditionally Treasury debt funds the deficit. The problem with relying on debt is that progressively larger debt loads push interest rates higher, complicating the situation. The amount of debt that investors are willing and able to take at a reasonable cost is limited.

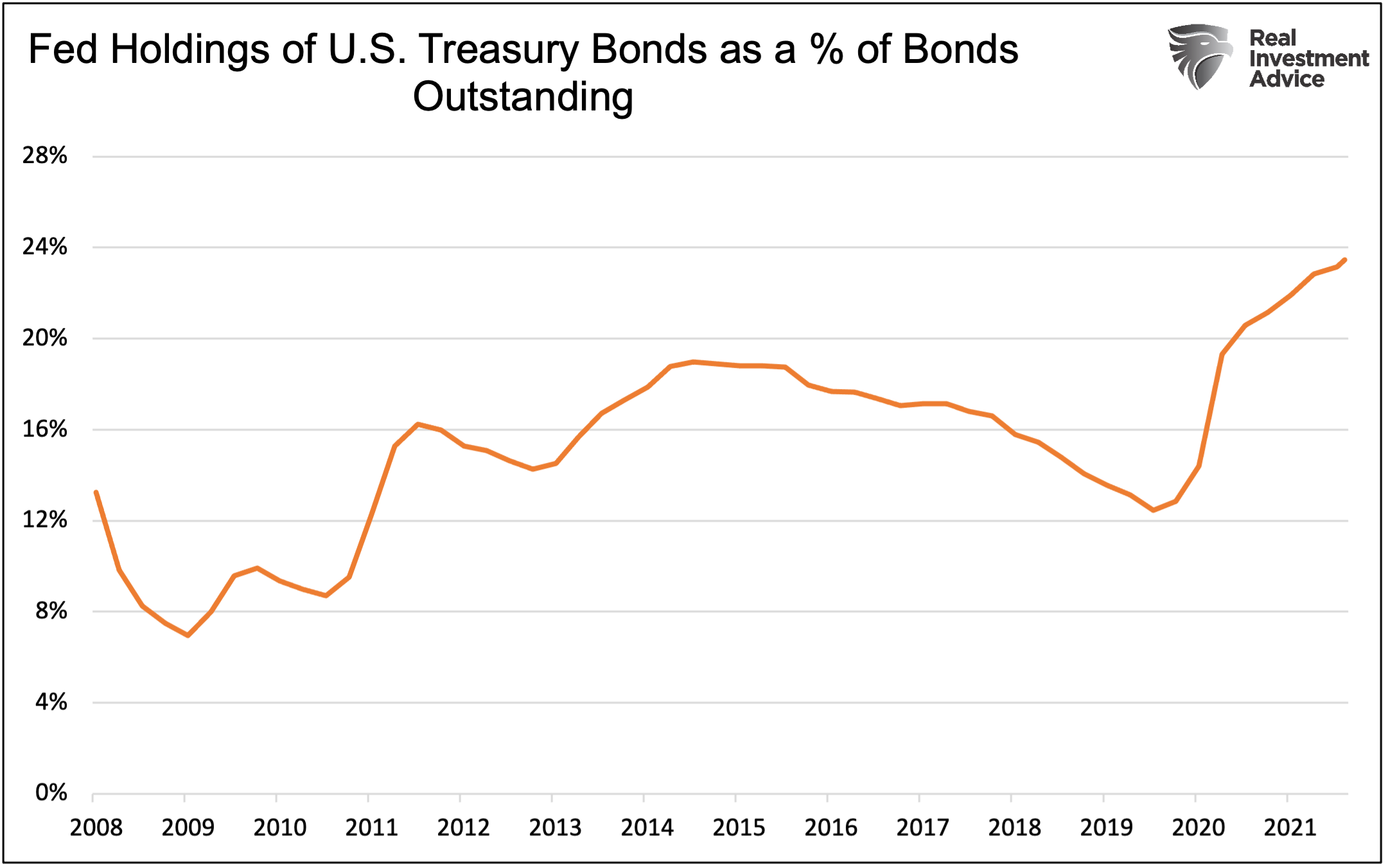

Enter the magician. Since 2008 the Fed has helped fund the deficit via quantitative easing (QE). The Fed now holds nearly a quarter of all outstanding federal debt. It is as if $5 trillion of Treasury debt was never issued. The Fed also has another $3 trillion of mortgage, agency, and corporate debt.

The Fed’s combined holdings of $8.25 trillion significantly reduce the supply of debt weighing on the markets, keeping interest rates artificially low.

In Willful Blindness, I wrote the following:

Currently, the government’s interest expense is less than 8% of total expenditures. That is the lowest percentage since at least 1947. Now contemplate the following:

- Total federal debt has risen 8320% since 1966.

- Federal debt-to-GDP is 127%, up from 40% in 1966.

- Interest expense declined by $46 billion as Treasury debt rose by over $7 trillion over the last year.

Fed magic allows for cheap funding of deficits. What could go wrong?

The cost of magic

Unlike the dancer in Miami and other overleveraged homeowners, the Fed can monetize federal debt pushing interest rates even lower. As we see in Europe, with negative interest rates, there are no limits to the madness.

The problem is the Fed’s magic comes with a cost.

For starters, savers, including a large chunk of baby boomers and retired people, must take on inappropriate levels of risk to compensate for zero interest rates on their cash.

Hey Gen X, Y, and Z, don’t laugh; you pay the price too.

As I wrote in Willful Blindness:

Aggressive monetary policies funding immense fiscal spending will only widen the wealth gap and further slow economic growth, as it has done in the past. At the same time, said policies drive more people to seek shelter from the rapidly devaluing dollar. Speculative investments will further dominate, leaving less capital for productive investment. Productive investments build economic growth and help everyone prosper.

Ignoring history and logic may be expedient, but it only aggravates our societal and economic shortfalls.

For more on why the Fed’s antics to push interest rates obscenely low are damaging, my article Wicksell’s Elegant Model is worth reviewing.

Summary

“The ratings agencies, the banks, the government, they’re all asleep at the wheel.” – Danny Moses (Rafe Spall) The Big Short

Michael Bury and others prospered by ignoring politicians, the media, and Wall Street. They uncovered the simple truth behind the subprime bubble. The sad fact of America’s fiscal position is just as easy to see for those willing to look.

Unlike The Big Short, our story is not as easy to time. As debt grows beyond our means, economic growth will continue to slow. The Fed will perform its magic and fill the funding gaps. Like any Ponzi scheme, it either gets bigger, or it fails. This one will get bigger, and it will fail.

As investors, we must understand what the Fed does and take advantage of its near-term benefits to asset prices. However, while others blissfully think this is normal, we must remain prepared for the end game, whenever it may occur.

Michael Lebowitz has been involved in trading, portfolio construction, and risk management involving some of the largest and most active portfolios in the world. In addition to broad institutional experience, he also built a successful independent RIA allowing him to further extend his experience into the realm of investment management for individuals and family offices. Grounded in logic and common sense, he blends vast trading and investment expertise with economic viewpoints that delivers pragmatic and actionable thought leadership to clients.

Join our website today for a look behind the data at what is really going on with the markets and your money. www.realinvestmentadvice.com

Contact him at [email protected]

More Portfolio Building Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.