Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

|

For a copy of the unabridged 2021 Global Hedge Fund Survey, including extensive statistical information on each of the Top 50 funds, five manager profiles, and a Q&A with noted economist David Rosenberg, please contact Eric Uhlfelder at [email protected] or call 917.459.8408.

|

Hedge fund investing during the time of COVID-19 – Part II1

For the third year in a row, the top 50 hedge fund managers, relying on a variety of strategies, generated net returns comparable to the S&P 500 with significantly less risk and performance that was largely independent of the market. Hedged equity, multistrategy, and global macro funds led the way with more than half the funds in the top 50 managing less than $1 billion.

*

“The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time and still retain the ability to function.”

- F. Scott Fitzgerald

What a difference a year makes.

Last spring, this survey was focused entirely on what everyone felt: the world had suddenly changed. A deadly pandemic was metastasizing at warp speed across the planet.

Economies and societies locked down, unemployment soared, real interest rates turned negative, stocks collapsed, and the exponential spread of Covid-19 has led to more US deaths than tallied in all the major wars fought in the 20th and 21st century.

When central banks and governments unleashed unprecedented liquidity, investors looked past the trauma that was unfolding, which sent equity markets soaring. Further, the fear of cascading business failures hasn’t materialized. By the second half of 2020, investors decided nothing really had changed.

Economist David Rosenberg put the market recovery in simple terms. “Over the past 40 years, the difference between monetary and economic growth has been about 1%. In 2020, this spread gapped to around 30%. Excess liquidity that’s not being absorbed by the economy is finding a home in the financial markets.”

With economies reopening and pent-up demand unleashed, the growth outlook appears robust. In April, the International Monetary Fund projected global growth of 6% in 2021 and 4.4% in 2022.

The Economist magazine reported, “businesses are starting to invest in huge numbers. In America, capital spending is rising at an annual rate of 15%, both on hard stuff, such as machines and factories, and intangibles, like software. Firms in other parts of the world are also ramping up spending. Forecasts for business investment have never looked so rosy.”

While Giovanni D’Alesio, head of alternative investment research at the $132 billion Swiss-based asset manager GAM, is well aware of these trends, he believes, “equity fundamentals don’t make any valuation sense.” Broadly speaking, he sees multiple, not real earnings, expansion driving markets higher. As a result, “many investors are looking away from the essential indicators and more towards technical analysis and sheer momentum which isn’t sustainable,” explains D’Alesio.

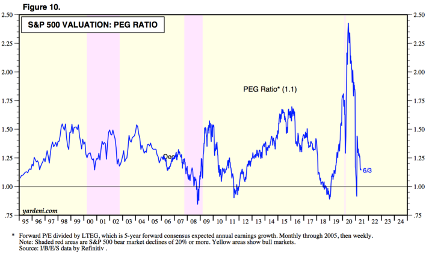

Source: Yardeni Research, 16 June 2021

Uncertainty and volatility that characterized 2020 was a boon for many hedge funds. Last year’s Top 50 funds delivered collective returns that were in line with the market, but they did so with far less drawdown and volatility.

And this year’s Top 50, 33 of which made the leap from the 2020 survey, did even better. They averaged gains of more than 24% in 2020 versus the S&P 500 Total Returns of 18.40%. And they more than doubled the hedge fund industry average gains of 11.14%.

But making the cut for this survey involved more than having thrived last year. The Top 50 represented funds with the highest trailing 5-year annualized returns through 2020.

Collectively they generated:

- 5-year net annualized returns of 14.81% versus the S&P 500 Total Returns of 15.22%. The hedge fund industry average gain over this period was 6.41%.

- Like last year’s list, this year’s Top 50 generated comparable gains with significantly less risk. Average worst drawdown of the Top 50 over this period was -12.22% versus -19.60% for the market. The industry average drawdown was -11.9%.

- Annualized standard deviation was 11.17% versus the market’s 15.13%. The industry average was 7.18%.

- Average Sharpe Ratio was 1.57 versus the market’s 0.93 and the industry’s average of 0.73%.

- These funds delivered this performance with only limited correlation to the S&P 500 – just 0.31. The hedge fund industry’s correlation to the market – suggesting how much the average fund tracks the main holdings of the S&P 500 – was 0.92.

As a group, these alternative investments – reflecting the performance of a variety of strategies – delivered market-like performance by being far more than just long equities.

Takeaway: While the majority of hedge funds do not deliver solid, consistent performance, there are a select number of managers that do through a well-established record of proven active management.

Methodology

The 50 funds that made this survey are not reflective of the hedge fund industry. They are outliers, revealing the industry’s promise.

They have defied the averages. Their mean age is 14.5 years – nearly triple the life expectancy of the average fund. Their returns have collectively kept up with a raging bull market while exposing investors to less risk.

The initial search started in early February with various databases, including BarclayHedge and Preqin, casting a wide net across the industry. They initially screened for broad strategy funds, excluding sector, country, specialized strategies (e.g., FX, metals, and commodities) and those applying exogenous leverage to a flagship portfolio.

A key screen that helps ensure reliability of data is to target funds managing at least $300 million. When funds reach that size, they frequently retain top-tier service providers – administrators, prime brokers, accountants, and lawyers – whose involvement may help deliver best-in-class practice.

The survey provides another layer of due diligence by contacting each manager to confirm the numbers. While funds feed data directly into each database, mistakes can happen, and individual numbers may have been revised since submission. This process also eliminates UCITs and other non-hedge fund entities that slip into databases.

There are always a handful of managers who will not verify their data. This does not mean the numbers are wrong. But it reinforces the need for perspective investors to do their own due diligence. The data provided here should be considered a starting point.

Perhaps the survey’s most unusual filtering is the use of performance hurdles for each of the last three years. This has raised the threshold for making the list, enhancing the value of this survey as a source of consistently performing managers.

This was initiated in the 2019 survey I prepared for The Wall Street Journal, which tracked performance over a trailing five-year period through 2018.2 Because 2018 was the first year in a decade when the market had lost money, setting a performance hurdle of 5% for that year was a clear way to see which funds delivered some form of alpha – swimming on their own without support of a buoyant market. Paraphrasing Warren Buffett, the hurdle helped reveal who had shorts on when the tide went out in 2018.

That hurdle was again maintained in this year’s survey for 2018 and 2019. For 2020, it was lowered to 4.5%, reflecting the decline in risk-free interest rates. The reasoning: requiring funds to generate only several hundred basis points of returns above the risk-free interest rate seems modest for any manager collecting management and performance fees.

Maintaining hurdles over the last three years, while identifying the best trailing five-year returns, helps this survey highlight managers that are generating consistent absolute returns while containing downside risk, eliminating funds whose performance bounces all over the place.

Further, while not appearing to be a demanding performance threshold, these modest hurdles recognize the fortunes of many strategies are not tied to a roaring stock market.

Survey results

While strategy-level performance may provide a base guide to what hedge funds have done, Sam Monfared, hedge fund research specialist at Preqin, observes “they tell little about the wide range of fund performance within each strategy.”

That’s certainly evident in the historical performance of the 21 strategies this survey tracks, which reveals a narrow range in returns over the trailing 3-, 5-, and 10-year periods. [See table below.] During these three periods, the industry’s annualized gains were one-third of the returns of the S&P 500.

While looking at a single year can also be misleading as well, 2020 revealed extraordinary breadth of performance by strategy. Equity long bias, volatility trading, convertible arbitrage, and emerging market funds delivered gains in excess of 15%. At the bottom, equity market neutral, asset-backed securities, and collateralized debt obligation funds were down slightly.

Structured credit strategies were the hardest hit by the pandemic as investors worried about the reliability of interest payments and potential impairment of underlying assets – both of which support these financially-engineered vehicles. This is most evident by the failure of a single such fund to qualify for this year’s Top 50.

Outliers

The remarkable outliers that comprise this survey are evident when comparing their performance with their respective strategy averages.

There are 15 equity long-short funds in the Top 50 – the highest showing of any strategy – that collectively returned nearly 19.5% per year over the past 5 years through 2020. But the strategy average return over the same period was a paltry 4.5%.

The top-performing equity long-short manager over the past 5 years was North Peak Capital (No. 2), which generated annualized returns of nearly 36% over that period. Woodson Capital Partners has also generated strong gains, averaging 33.47% over the past 5 years through 2020.

The survey’s 8 multistrategy funds also show substantial collective outperformance versus its peer strategy average return over the past 5 years: 11.42% versus 2.91%. The two top-performing funds in this category is the venerable $23.6 billion Citadel Wellington (No. 19) that’s been generating annualized returns of 14%. (Citadel declined to comment for this survey.) Hong-Kong based Segantii Asia-Pacific Equity Multistrategy fund (No. 48), which was managing $4.8 billion at the end of last year, has produced annualized returns of 13.8% since its launch 13 years ago.

The contrast between the average global macro fund performance and the 7 that made this year’s survey is also striking: 12.13% versus 3.48%. Over the last 5 years, the $704 million Haidar Jupiter (No. 7) and $18.2 billion Element Capital (No. 17) generated gains of 22.1% and 14.5%, respectively – the highest returns of all global macro funds in the Top 50.

Size

Some very large funds are strong, consistent performers, including Tiger Global, Citadel, D.E. Shaw, and Element Capital. Seven big funds that made the survey are collectively managing $108 billion, more than double the assets of the other 43 smaller funds that comprise the list. However, 10 of the top 15 funds on this survey each ran less than $900 million in assets.

This annual survey has regularly identified smaller funds as being more consistent long-term top performers than their larger brethren, with 28 of the Top 50 managing less than $1 billion, 20 ran less than $725 million, and 13 had assets of less than $500 million.

Panayiotis Lambropoulos, a hedge fund portfolio manager at the $32 billion pension fund ERS Texas, believes “in the merit of proven, smaller, institutional-caliber managers to help potentially achieve long-term investment goals.” His pension fund has teamed up with the fund of funds manager PAAMCO-Prisma to underwrite small, emerging managers to help boost returns.

“Because of their size,” explains Eric Costa, global head of the hedge funds investment group at the consultancy Cambridge Associates, “smaller managers have the ability to invest meaningfully across a wider universe, compared with larger peers, and move in and out of positions more nimbly, without impacting prices.”

Opportunities and risks

In May, before the Delta variant metastasized across much of the country, most allocators interviewed for this survey (including The World Bank, GAM, Notz Stucki, and Investcorp-Tages) generally believed the risk of the pandemic to economies and markets is mostly behind them. One allocator did not – Panayiotis Lambropoulos of ERS Texas.

Most allocators also believe current inflation fears seem to be transient – caused by bottlenecks resulting from economies reopening – and central banks will not be raising interest rates this year. Toward the end of 2021, however, they expect these banks to start tapering their quantitative easing.

Allocators agree valuations are high and will likely go even higher, because as GAM’s Giovanni D’Alesio explains, “most investors don’t see any other place to go.” But he notes not all sectors and industries are overvalued.

One main reason allocators remain keen on hedge funds is their various strategies extend well beyond high-priced stocks. That said, hedged equity funds remain in vogue. But allocators are targeting managers more focused in delivering uncorrelated Alpha.

With the tremendous rally in growth shares, allocators last year started to rotate into value. Many believe any pullback in value shares offers additional opportunities to up their exposure to this asset class.

Discretionary global macro is also attracting allocator attention as economies move out of the shadow of the pandemic. The strategy can offer investors a prompt response to unexpected turns in bond and equity indices, interest rates, commodity prices, and volatility.

Fixed-income relative value is also being embraced by many allocators as a means to gain uncorrelated returns through leveraged exposure to corporate and sovereign debt spreads, assets that otherwise are offering virtually no returns and capital risk if interest rates begin to rise in earnest.

Allocators are also hedging inflation risk by moving into commodities (including industrial and precious metals, grains, and fuel) real estate, and businesses protected by large moats that have the ability to pass on higher costs, like some of the big name tech giants.

While allocators are globally diversified, their exposure is tilted toward the US.

And while many allocators are looking at China as a source of outsized gains, down the road others see the country as the leading source of geopolitical risk.

Divergence

Allocator opinions diverge on several key issues. While ERS Texas’ Panayiotis Lambropoulos predicts economic data for the rest of 2021 will likely surprise on the upside, he remains cautious about Covid-19.

“Most of the country is functioning as if the pandemic is in the rearview mirror,” explains Lambropoulos. But as of mid-June, the country’s vaccination rate seems stalled in the mid-60%.” While transmission, hospitalization, and death rates are all trending in the right direction, he wants to see if these numbers hold past summer and into winter (when people are back inside) to have a clear understanding where we are in the pandemic.

With hedge fund assets approaching $4 trillion and a limited number of high quality, consistently performing managers, Giovanni D’Alesio thinks allocators need to pay careful attention to managers’ stated capacity limits.

He also cautions small-cap managers may allow positions to appreciate into mid-caps and may venture into the pre-IPO market to expand their investment universe, both of which introduce new risks and performance expectations.

Two allocators think Europe offers a solution to overvalued US markets. Elisabetta Manuli, vice president and fund manager at the Milan-based fund of funds Hedge Invest, “thinks European opportunities are more attractively valued compared to US shares, especially since continental recovery is about 6-12 months behind the States.”

GAM’s Giovanni d’Alesio also likes Europe. But he notes any shocks that hit US markets are very likely to reverberate across to Europe.

Structured credit strategies were the hardest hit by the pandemic. Because Vincent Berthelemy of Investcorp-Tages sees plenty of dislocation in the space, he thinks certain mortgage-backed securities and collateralized loan obligations can attractively compensate investors for related liquidity risks as housing prices continue to improve.

The World Bank’s Mohamed Farid and GAM’s D’Alesio think meaningful distressed opportunities will still evolve. “So far, troubled companies have been able to survive because economies have been pumped full of liquidity and interest rate spreads have not widened, which would trigger borrowing stress,” explains D’Alesio. “However, over the next two to three years, rates may climb and this could generate a rise in defaults.”

Debt

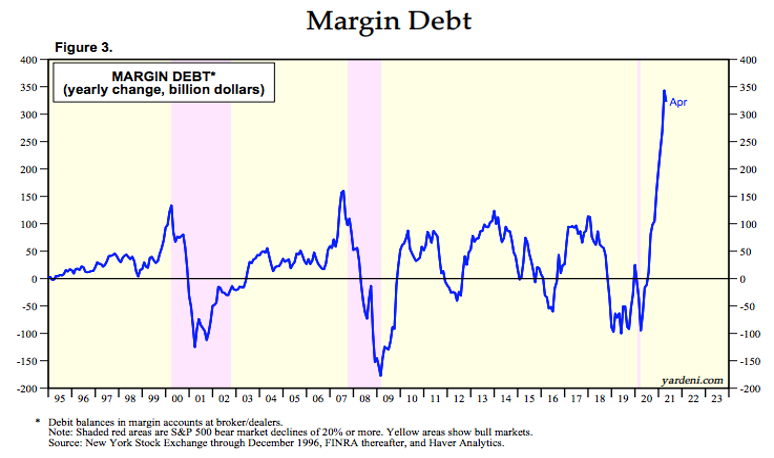

Several of the allocators express concern about rising margin debt related to investments. “Just as it helps elevate the market,” observes Lambropoulos, “margin can quickly reverse course if companies fail to meet lofty growth expectations.”

Originally published in: “Stock Market Indicators: Margin Debt,” Yardeni Research, 7 June 2021.

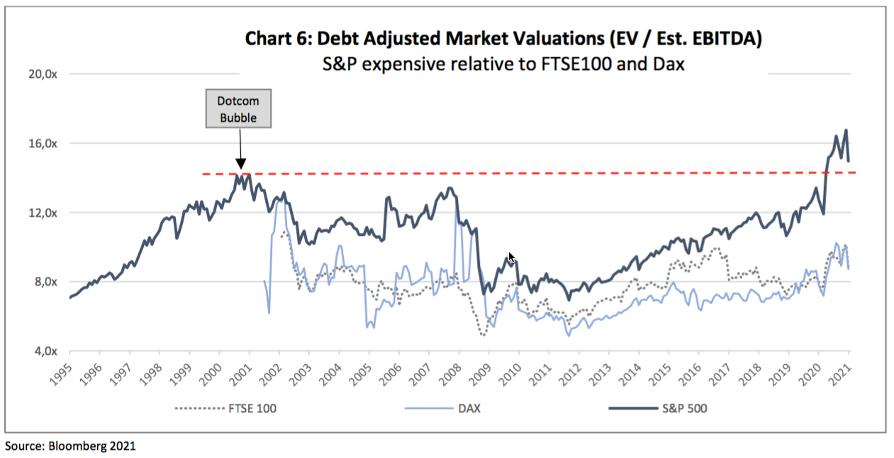

Soaring overall debt piling up in response to the pandemic worries Eric Knight, CEO and CIO of the Swiss-based asset manager Knight Vinke. “With global debt-to-GDP levels approaching 400% and pandemic-related public expenditures set to increase without restraint almost everywhere,” cautions Knight, “the world’s financial system is more than usually fragile at this moment and will become even more so.”

Knight is worried about southern Europe, including France, and believes the US market is trading – on a debt-adjusted basis – 10% above its valuation at the peak of the dot-com bubble. [See table below.]

“The value investor in me feels a correction is long overdue,” explains Knight. But he admits the euphoria driven by vaccinations, government handouts and the lifting of restrictions on travel and social interaction is hard to ignore. “Dealing with this contradiction is hard for many asset managers and often leads to paralysis,” says Knight, especially as the music plays on.

About this year's survey

My 18th annual global hedge fund survey is being published under my own banner – Global Investment Report. The 17 previous editions were commissioned by The Financial Times, Barron’s, The Wall Street Journal, and last year by SALT.

This year’s survey continues improvements I’ve been making on methodology and reporting, which I initiated in the 2019 Wall Street Journal version.

This included extending the period for which performance is ranked to the trailing 5 years. Further enhancements included tracking worst drawdown, standard deviation, Sharpe Ratio, and market correlation over the same period to gain a more complete understanding of performance.

With the exception of market correlation, I also tracked these metrics since the inception of each fund – which was never done in any previous survey. With the average fund age being nearly 15 years, this revealed performance consistency that extends back to when each qualifying fund was launched.

Combining this extensive statistical study with qualitative overview of the hedge fund industry as observed by leading global allocators, economists, consultants, and managers who made the Top 50 presents a comprehensive assessment of what the most consistent performing hedge funds can deliver and what they expect may play out for the rest of 2021.

Eric Uhlfelder has prepared 17 annual hedge fund surveys for Barron’s, The Financial Times, and most recently The Wall Street Journal. He covers global capital markets from New York over the past 25 years for various major financial publications. He wrote the first book on the advent of the euro post currency unification, “Investing in The New Europe,” for Bloomberg Press. And he has earned a National Press Club Award. His website is www.globalinvestmentreport.net.

1To see Part I of this survey, which was published last year, please go to globalinvestmentreport.net. Quarterly updates through 2020 are also viewable at this site.

2Uhlfelder, Eric. "As Hedge Funds Struggle, These Are Standing Out," The Wall Street Journal, 6 May 2019. This survey of 60 funds was based on the same methodology as the current survey.

Read more articles by Eric Uhlfelder