The predominant approach to classifying securities geographically is based on domicile, which is generally be defined as the legal home of a company. But that approach has lost its relevance. Instead, investors should look at foreign revenue to achieve internationally diversified allocations.

The predominant approach to classifying securities geographically is based on domicile, which is generally be defined as the legal home of a company. But that approach has lost its relevance. Instead, investors should look at foreign revenue to achieve internationally diversified allocations.

Domicile is typically a binary attribute, where a company is attributed entirely to a single location (i.e., country). But other metrics should be considered when defining the “internationalness” of a company.

In this article, I explore the role of foreign revenue, based on some of my research that was recently published in the Journal of Portfolio Management.

The key findings of that paper include:

- The diversification of benefits of international investing have declined significantly over time. A key reason is the increasingly interconnected global economy. This highlights the weakness of defining geographic risks based entirely on a company’s location and not considering economic risks, like geographic revenue exposure.

- There were notable differences in foreign revenue exposures across countries (and funds). While approximately 40% of revenues for U.S.-domiciled companies is foreign, it is much higher (75% in UK) and lower (8% in China) elsewhere. This suggests the economic benefits associated with investing in a country may be lower than suggested by domicile-based metrics and that investors interested in obtaining a “purer” exposure to a region would be better served from revenue-based strategies.

- Revenue exposure explained a meaningful level of variation in excess returns and excess risks among domestic mutual funds at a level that is similar to domicile. This suggests that foreign revenue needs to be considered when assessing the risk of a fund (or portfolio) and that ignoring foreign revenue is akin to ignoring the size and value dimensions for a U.S. equity fund from a risk-factor perspective.

- Overall, domicile provided a incomplete perspective on global risks and other metrics, like revenue, should be considered when defining the “internationalness” of an investment or portfolio.

Domicile

Domicile is by far the most common metric used to classify securities geographically. A variety of metrics can be used to determine domicile. For example, to be included in the S&P 500 a company must file 10-K annual reports, meet certain fixed assets and revenue thresholds, and have a primary listing on an eligible U.S. stock exchange. Morningstar1 considers four key factors to determine domicile: country of incorporation, country of primary headquarters, country of primary exchange listing, and geographic source of revenues and locations of assets.

Investors often seek funds with different domiciles given the research noting benefits associated with international diversification. But the realized benefits of international diversification have declined significantly since it was originally noted in the 1970s.

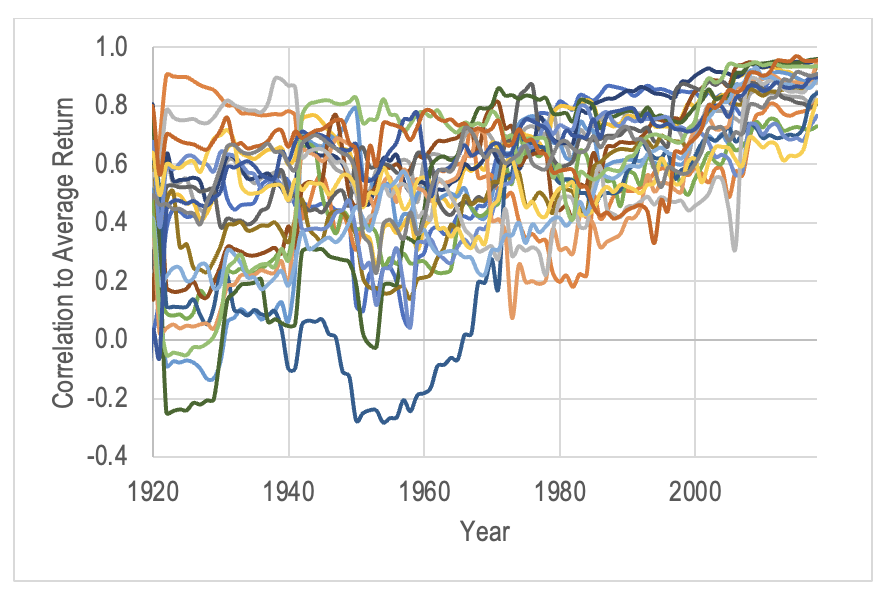

This effect is exhibited below, which shows the rolling 20-year correlations of equities within 21 countries to a global index2 from 1900 to 2020 using the Dimson, Marsh and Staunton dataset.

Rolling 20 Year Country Equity Return Correlations to Global Index

Source: Dimson, Marsh, and Staunton dataset, Morningstar Direct as of December 31, 2020

Correlations to a global index have increased considerably and the dispersion has declined. In 1920, the average correlation was .46 with a standard deviation of .26. This has been a significant change since then. For example, in 1975 the average correlation was .61 and the standard deviation was .18. Recently the correlation has increased to an average of .88 with a standard deviation of .06. In other words, while international investing has some diversification benefits, those benefits have declined significantly over time.

Foreign revenue

Just because a company is domiciled in Germany does not mean its revenue come from Germany. Also, just because an investor invests domestically (e.g., owns only the S&P 500 for a U.S. investor), it does not mean he or she has no international risk exposure.

Revenues are one of the many economic variables that have become available for publicly traded securities over time. For example, the London Stock Exchange started requiring listed firms to disclose some segment-level information, such as turnover and profits, in 1965, and the first international segment-reported standard, IAS 14, required reporting on both line-of-business and geographic segment data.

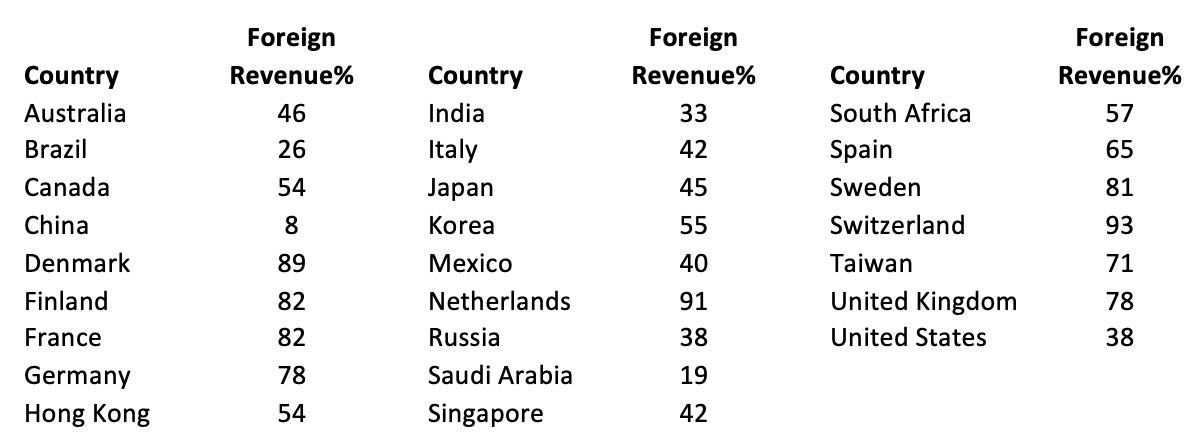

There are notable differences in the levels of foreign revenues across countries, as demonstrated in the following exhibit.

Foreign Revenue Exposure by Country

Source: “Foreign Revenue: A New World of Risk Exposures” by David Blanchett, Journal of Portfolio Management. Published March 31, 2021.

While approximately 40% of revenues for U.S.-domiciled companies are foreign, the level of foreign revenues is much lower in China (8%) and higher in the UK (78%). The country-specific diversification benefits associated with investing in China will be higher than investing in the UK.Source: “Foreign Revenue: A New World of Risk Exposures” by David Blanchett, Journal of Portfolio Management. Published March 31, 2021.

There is a positive relation between country foreign revenue exposure and market capitalization that is statistically significant at the 5% level (p value of .013); however, there is no relation between country foreign revenue exposure and GDP. This suggests it isn’t necessarily the size of the country’s economy that drives foreign revenue exposure; it is whether capital markets are more advanced.

While the historical risk levels of countries with higher foreign revenue exposures tends to be lower, the effect is primarily due to market capitalization. In other words, countries that have more foreign revenues don’t drive lower volatility; it’s the fact they are larger.

Foreign revenue-focused investments

There are relatively few, if any, investments focused specifically on geographic revenue exposure despite a growing body of research on the topic. MSCI was an early leader making the case for “economic exposure indices,” where investors could achieve risk exposures to a given region (e.g., emerging markets) by targeting firms with representative revenue exposures, although it’s not clear whether any investment strategies were created from the research.

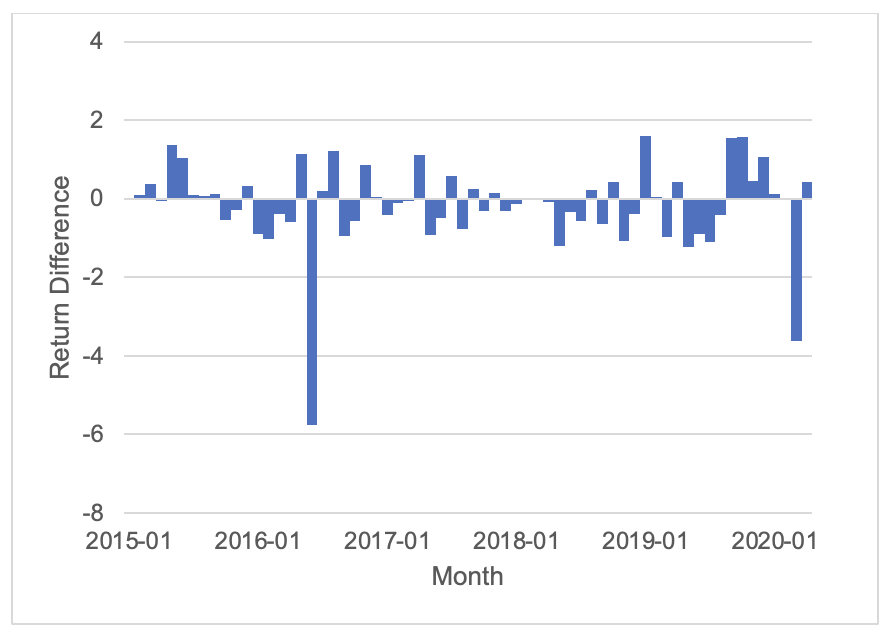

I created revenue-focused industries for eight countries3 from December 2014 to March 2020, where the weights were reconstituted annually. I created a variety of indices that tilted the underlying security weights towards companies with higher levels of domestic revenue and a series that attempted to control for things like sector differences (since tilting based on revenue can notably change the underlying risk characteristics).

There were two notable findings:

- There were large differences in the returns for revenue-focused indices versus the more traditional domicile-based indices. For example, there is a notable deviation in returns for the United Kingdom in June 2016 (-5.76% lower), the month of the Brexit vote, as demonstrated below. This effect has been noted previously by Whitelaw et al (2019).

Source: “Foreign Revenue: A New World of Risk Exposures” by David Blanchett, Journal of Portfolio Management. Published March 31, 2021.

- While the revenue-focused strategies didn’t typically have higher returns or lower levels of risk, they were a purer way to get exposure to a given country. It’s not necessarily clear whether the risk/return relation will continue, but it does suggest an investor interested in gaining risk exposure to a given region (e.g., France) will be better served using a strategy that is more focused on the economic attributes of the respective companies versus purely domicile.

There are potential cost and tax savings using these types of approaches. For example, an investor interested in gaining exposure to a certain country (e.g., Germany) could be better served focusing on U.S.-listed securities with higher levels of revenue exposure to Germany than using an investment strategy that focuses on stocks with a German domicile.

Foreign revenue and investment risks

How did foreign revenue exposure vary across investments within various countries, and what was the relation of foreign revenue to excess risk and return?

For the analysis, I focused on actively managed domestic equity mutual funds (as classified by Morningstar) in seven countries: Australia, Canada, France, Germany, Switzerland, the United Kingdom, and the United States. I tested a total of 25 country/style combinations from a total of 3,155 funds.

The level of foreign-domicile exposure among the funds was relatively low, which is not surprising since only domestic-focused investment styles were included in the analysis (and used as a filter for inclusion). The average foreign domicile was approximately 10% with an average standard deviation of approximately 10%.

There were much higher levels of foreign-revenue exposure among the funds and that varied significantly. For example, while the average France-based large equity fund had 13.7% of securities domiciled outside of France, 79.6% of the revenues of the companies came from outside of France. This is consistent with the previous analysis but highlights how the potential benefits of international diversification vary by region.

The average standard deviation of foreign-revenue exposure across the fund groups was approximately 10%, which is roughly consistent with the variation noted by domicile. In other words, while the absolute differences were relatively substantial, within each country the distribution of the differences for foreign revenue were relatively tight.

There were notable differences in foreign-revenue exposure across the size and value spectrums, where larger cap-based funds and growth funds tend to have higher foreign-revenue exposure weights. This effect was relatively consistent across countries although there were exceptions (e.g., small funds in Canada had higher foreign exposure than large funds).

To better understand how foreign revenue was related to excess returns and excess risk, I ran a series of factor regressions. I found that foreign revenue had similar explanatory power to domicile when it comes to explaining the variation in risk and returns (both raw and excess) with funds that had similar styles. Additionally, both provided better insight into variations in returns of funds (i.e., standard deviations) versus returns. In other words, understanding foreign revenue was important when understanding the underlying risks of a fund. Ignoring foreign revenue will provide an incomplete perspective of the true global risks of a given fund.

Conclusions

Diversification is often touted as the only “free lunch” in investing. Investors are increasingly looking beyond their domestic markets to be diversified. The most common metric to determine the geographic location, and often risks, of a company is domicile.

Foreign-revenue exposure is an important consideration when assessing the risk exposures of a fund. Foreign-revenue exposure provides a different perspective on the underlying risks of a given investment, and unlike domicile it is not binary, allowing for a more complete consideration of risks.

Creating investments focused on foreign-revenue exposure (e.g., a domestic revenue-focused index or fund) should be of interest to investors, especially those who want a “purer” allocation to a given country or geographic region.

Overall, as global economies continue to become increasingly interconnected, legacy metrics such as a domicile will become less relevant when describing the risks of a given strategy. Therefore, it is incumbent on investment professionals to understand, and use, foreign-revenue exposures when selecting funds and developing portfolios for clients.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research, DC solutions for QMA, which is the quantitative equity and multi-asset solutions specialist of PGIM, the global investment management business of Prudential Financial, Inc. In this role he develops research and innovative solutions to help improve retirement outcomes for investors.

Notes to Disclosure

QMA is the primary business name of QMA LLC, a SEC-registered investment adviser that is organized as a New Jersey limited liability company. Registration with the SEC does not imply a certain level of skill or training. QMA is a wholly-owned subsidiary of PGIM, Inc., and a Prudential Financial, Inc. (PFI) company.

These materials represent the views and opinions of the author regarding the economic conditions, asset classes, or financial instruments referenced herein and are not necessarily the views of QMA.

These materials do not take into account individual client circumstances, objectives or needs. No determination has been made regarding the appropriateness of any securities, financial instruments or strategies for particular clients or prospects. The information contained herein is provided on the basis and subject to the explanations, caveats and warnings set out in this notice and elsewhere herein. Any discussion of risk management is intended to describe QMA’s efforts to monitor and manage risk but does not imply low risk. Past performance is not a guarantee or reliable indicator of future results. An investment cannot be made directly in an index. Diversification does not protect against a loss in a particular market; however, it allows you to spread that risk across various asset classes.

Certain information contained herein may constitute "forward-looking statements," (including observations about markets and industry and regulatory trends as of the original date of this document). Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements. As a result, you should not rely on such forward-looking statements in making any decisions. No representation or warranty is made as to future performance or such forward-looking statements.

QMA- 20210810-211

1Morningstar. 2015. “Methodology for Morningstar Business Country Assignment.” White Paper.

2Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, South Africa, Spain, Sweden, Switzerland, the United Kingdom, and the United States

3Australia, Canada, France, Germany, Japan, Switzerland, United Kingdom, and United States

The predominant approach to classifying securities geographically is based on domicile, which is generally be defined as the legal home of a company. But that approach has lost its relevance. Instead, investors should look at foreign revenue to achieve internationally diversified allocations.

The predominant approach to classifying securities geographically is based on domicile, which is generally be defined as the legal home of a company. But that approach has lost its relevance. Instead, investors should look at foreign revenue to achieve internationally diversified allocations.