Investment strategies that use buffers and floors to provide downside protection, such as registered index-linked annuities (RILAs) and a growing number of ETFs, are gathering assets and receiving a significant amount of attention in the media and among advisors. But their risk is harder to measure than more traditional investment products. While their returns are going to be based on their underlying index (typically the S&P 500), the realized returns will vary significantly depending on the put and call option exposures used to implement the strategy.

Investment strategies that use buffers and floors to provide downside protection, such as registered index-linked annuities (RILAs) and a growing number of ETFs, are gathering assets and receiving a significant amount of attention in the media and among advisors. But their risk is harder to measure than more traditional investment products. While their returns are going to be based on their underlying index (typically the S&P 500), the realized returns will vary significantly depending on the put and call option exposures used to implement the strategy.

In this article, I provide guidance on the “equity-like” risk of buffer and floor strategies when included in a diversified portfolio, assuming an S&P 500 underlying index. I use four measures of risk: standard deviation, downside risk, value-at-risk and conditional value-at-risk.

This research attempts to quantify the extent to which each product would be considered “equity-like.” Risk is framed in terms of equity exposure since it is a generally accessible metric and normalizes the results across the risk metrics I consider.

This analysis shows that the risks of buffer and floor strategies differ significantly by approach and level. To generalize, the equity-like risk of buffer strategies can be approximated by taking 100 minus four times the buffer level and the equity-like risk of floors can be approximated by multiplying the floor level by four. For example, a 10% buffer product would be approximately 60% equity-like (100-(4*10)=60) and a 10% floor product would be approximately 40% equity-like (10*4=40). These are approximations that don’t capture the more complex risk considerations associated with different product combinations (e.g., a 30% buffer floor has a much greater potential loss than a 10% equity allocation),but provides a useful rule of thumb to advisors.

What are buffers and floors?

Investors want full upside participation with no potential for loss. While this isn’t a realistic goal, it is possible to implement a strategy with some upside potential that limits downside risk by using options such as puts and calls. A fixed indexed annuity (FIA) is an example of such a product, as are more traditional structured products.

The decline in interest rates over the last several decades has reduced the potential upside for products that offer no downside risk. In response, new products have been created that offer varying levels (and types) of downside risks for different levels of upside exposure. These are generally referred to as buffer or floor strategies. These can be implemented a variety of ways, such as in an ETF or an annuity, which is typically referred to as a registered index-linked annuity (RILA).

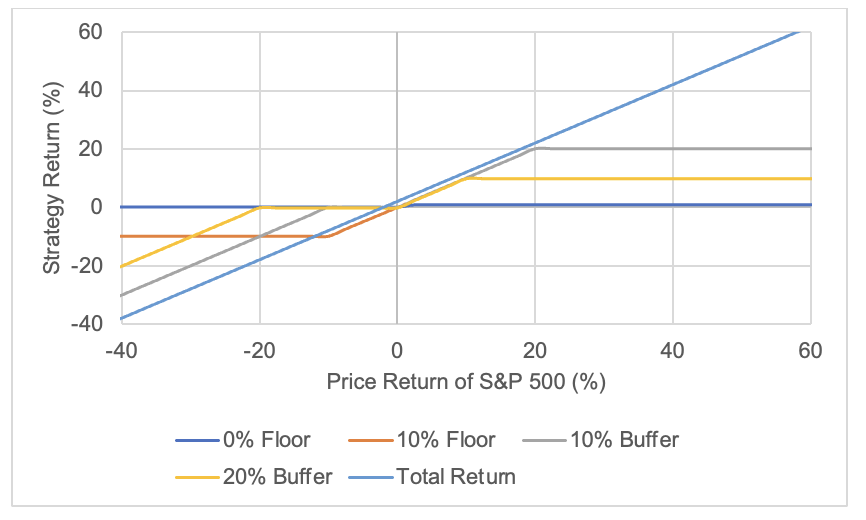

With buffer strategies, the initial loss is absorbed by the product, based on the buffer level, and the investor suffers any loss beyond that. For example, if the buffer is 10% and the underlying index fell 40%, the investor would lose 30%. If the decline of the underlier is less than the buffer, the return would be 0%. For example, if the buffer is 10% and the underlier falls 5%, the investor return would be 0%.

With floor strategies, the downside is limited to a stated percentage, such as 10%. For example, if the floor is 10%, the investor can’t lose more than 10% regardless of the return of the underlier. A buffer product with a 0% floor would have the same risk profile as a FIA.

With buffers and floors, returns vary widely

The potential return distribution can vary significantly by strategy (i.e., buffer versus floor) and the level of the buffer or floor. Generally, the greater the potential loss associated with buffers and floors, the higher the potential upside. The chart below shows the one-year expected returns for different buffer and floor strategies, assuming the underlier is the S&P 500.

Strategy returns vs. the S&P 500

Source: QMA. As of July 15, 2021

An investor who purchases the S&P 500 directly (e.g., through an ETF) would earn the total return of the index (minus fees and expenses). This is a combination of price return (capital appreciation/depreciation) and income return (dividends). With a buffer or floor strategy, the return excludes dividends). This is why the “total return” in the above exhibit is always higher than the floor and buffer returns for a given (positive) price return.

Risks of buffers and floors differ by level

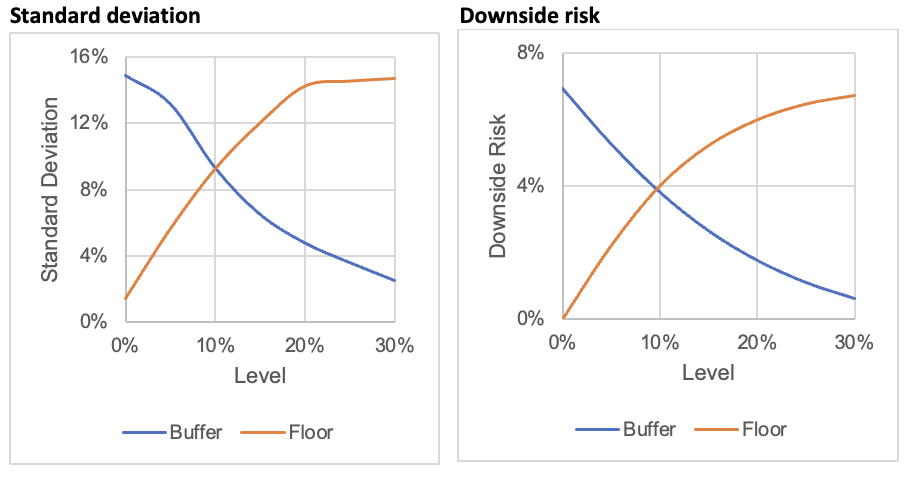

The risks of buffer and floor strategies vary significantly, especially across levels (e.g., 10% versus 30%). The charts below show the standard deviation and downside risk for buffers and floors, given different levels.

The risks associated with the strategies are clearly very different. Some structures are very low risk, while others are quite risky. For example, the standard deviation and downside risk of a 0% floor is low and therefore bond-like. On the other hand, the standard deviation and downside risk of a 30% floor are high and therefore more equity-like.

Risk differences across strategies and levels

Source: QMA. As of July 15, 2021

The risk metric matters. On a relative basis, floors look slightly riskier using standard deviation than downside risk. This is not surprising since standard deviation considers the entire distribution of returns, while downside risk focuses only on the negative returns.

The correlation between the respective strategies and the S&P 500 is very high, roughly 0.8. This is because the returns of the strategies are based on the index and highly correlated to other investments in the portfolio (e.g., equities). Potential diversification benefits may be greater with buffer and floor strategies that are based on a less correlated underlier.

Effective risk: Analysis1

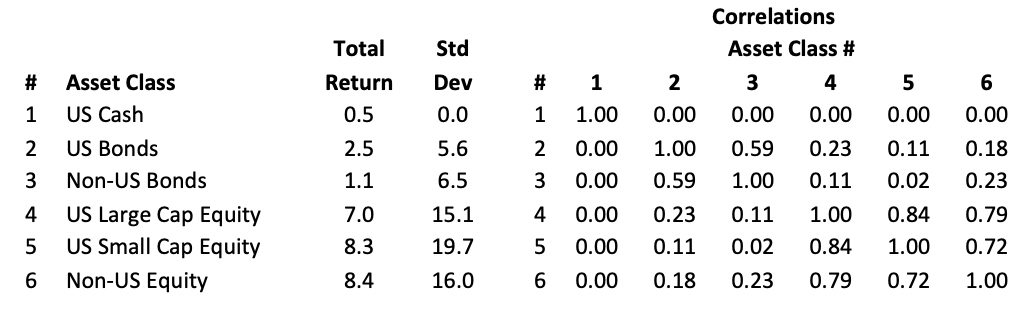

To estimate the effective risk of buffer and floor products, I determine how adding a 20% allocation of a given buffer or floor strategy impacts the risk attributes of a plain vanilla portfolio. This portfolio is assumed to be 50% fixed income and 50% equities. The sub-asset class weights are 10% cash, 30% U.S. bonds, 10% non-U.S. bonds, 30% U.S. large-cap equity, 10% U.S. small-cap equity, and 10% non-U.S. equity.

The returns, standard deviations, and correlations for the opportunity set are included below and are based on QMA’s Q2 2021 capital market assumptions (CMAs).

Return assumptions

Source: QMA. As of July 15, 2021

The analysis assumes returns follow a normal distribution and that the investment period is one year. The assumed underlier for the buffer and floor strategies is the U.S. large-cap equity index (i.e., the S&P 500), and the dividend yield is assumed to be 2%.

The risks associated with the portfolio with the 20% buffer/floor strategy allocation are compared to the different combinations of a plain vanilla portfolio, keeping the previously noted intra-bond and intra-stock weights constant. For example, the base (50/50) portfolio has a standard deviation of approximately 8.0%. If the 20% buffer/floor allocation caused the standard deviation of the portfolio to fall to 6.0%, that would correspond to a 30% equity portfolio that did not include a strategy allocation. This means the 20% buffer/floor allocation had the same risk impact as moving 20% of the portfolio from equities to fixed income, and suggests the equity-like impact of the buffer/floor would be 0% equity-like (i.e., similar to allocating to fixed income).

Risk is defined as an equity percentage since it is a more accessible unit for advisors and consumers. It normalizes the results across risk metrics.

Four different risk metrics are considered: standard deviation, downside risk (negative returns are considered risky), value-at-risk (5th percentile target) and conditional value-at-risk (returns below the 5th percentile are averaged). Each metric has its shortcomings, so multiple metrics are employed for robustness.

Results: Lower buffers and higher floors are more equity-like

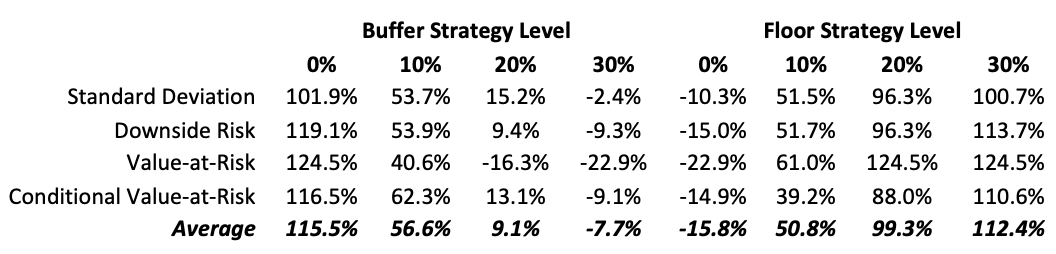

The exhibit below shows the results of the analysis and contains the equity-like risk of the respective strategy when it is added to a plain vanilla portfolio in the form of a 20% allocation. A value above 100% says the risk change was more than a 100% allocation to equities (i.e., the strategy is very risky) and a negative value indicates the risk was relatively low (i.e., like adding more than 100% to fixed income).

Equity-like risk for various buffer and floor strategies

Source: QMA. As of July 15, 2021

While the equity-like risk of the products differed among the four risk metrics and the respective strategies, the overall values for each respective strategy combination were relatively similar. The results suggest the risk of buffer strategies decreases at higher levels, and the risk of floor strategies decreases at lower levels.

Estimating equity-like risk

Using these results and some algebra, we can arrive at a formula for estimating the varying levels of equity-like risk for different-sized buffer and floor strategies.

For buffer strategies:

Equity-like risk = 100 – 4*(the buffer level).

For example, a 10% buffer product would be approximately 60% equity-like (100-(4*10)=60).

For floor strategies:

Equity-like risk = 4*(the floor level).

For example, 10% floor product would be approximately 40% equity-like (10*4=40).

Conclusions

The growing number of buffer and floor strategies represents an exciting opportunity for advisors. However, these products come with complexities that advisors should understand and consider before recommending them. In this article, I provided perspective on the equity-like risk of buffers and floors so that advisors can have a better perspective about where they fit as part of a total portfolio from a risk perspective.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research, DC solutions for QMA, which is the quantitative equity and multi-asset solutions specialist of PGIM, the global investment management business of Prudential Financial, Inc. In this role he develops research and innovative solutions to help improve retirement outcomes for investors.

Disclosures

QMA is the primary business name of QMA LLC, a SEC-registered investment adviser that is organized as a New Jersey limited liability company. Registration with the SEC does not imply a certain level of skill or training. QMA is a wholly-owned subsidiary of PGIM, Inc., and a Prudential Financial, Inc. (PFI) company.

These materials represent the views and opinions of the authors regarding the economic conditions, asset classes, or financial instruments referenced herein and are not necessarily the views of QMA.

These materials do not take into account individual client circumstances, objectives or needs. No determination has been made regarding the appropriateness of any securities, financial instruments or strategies for particular clients or prospects. The information contained herein is provided on the basis and subject to the explanations, caveats and warnings set out in this notice and elsewhere herein. Any discussion of risk management is intended to describe QMA’s efforts to monitor and manage risk but does not imply low risk. Past performance is not a guarantee or reliable indicator of future results. An investment cannot be made directly in an index.

QMA-20210622-167

1The options are priced using a Black-Scholes options pricing model that incorporates a nonconstant implied volatility level based on the historical median relation using data obtained from deltaneutral.com on SPX from January 1990 to December 2020. Note, the options pricing only affects the standard deviation estimate since the other metrics are focused entirely on downside. The analysis assumes the options budget to build the buffer and floor is 50 bps higher than the risk-free rate and that implied volatility is 20% (500 bps higher than the base risk assumption for large cap equities). For reference purposes, the resulting caps for the 0% buffer, 10% buffer, 20% buffer, 30% buffer, 0% floor, 10% floor, 20% floor, and the 30% floor are 100%, 18%, 9%, 5%, 3%, 14%, 100%, and 100%, respectively.

Investment strategies that use buffers and floors to provide downside protection, such as registered index-linked annuities (RILAs) and a growing number of ETFs, are gathering assets and receiving a significant amount of attention in the media and among advisors. But their risk is harder to measure than more traditional investment products. While their returns are going to be based on their underlying index (typically the S&P 500), the realized returns will vary significantly depending on the put and call option exposures used to implement the strategy.

Investment strategies that use buffers and floors to provide downside protection, such as registered index-linked annuities (RILAs) and a growing number of ETFs, are gathering assets and receiving a significant amount of attention in the media and among advisors. But their risk is harder to measure than more traditional investment products. While their returns are going to be based on their underlying index (typically the S&P 500), the realized returns will vary significantly depending on the put and call option exposures used to implement the strategy.