Making Sense of Tesla’s Run-up

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

I would like to thank Rob Arnott, Andrew Cornell, Shuan Cornell, Richard Gerger, Eric Madsen, and particularly Aswath Damodaran for helpful comments on earlier drafts of this paper

Abstract

Tesla has run-up again. Between December 2, 2019 and April 30, 2021, the price of Tesla rose more than ten times creating over $600 billion in investor wealth. The analysis presented here implies that the 10x jump cannot be explained by the arrival of fundamental information regarding the macroeconomy, the auto industry, or company specific information related to Tesla as an electric vehicle manufacturer. The only feasible explanation for the run-up was a spreading narrative that Tesla is more than a car company. As stated by Mr. Musk, and echoed by Cathie Wood and others, Tesla is also going to be a renewable energy, artificial intelligence, ride sharing, and robotics company. Such narratives have the advantage that they can blossom and replicate with little in the way of capital expenditure and improvements in operations both of which tend to have a sluggish impact on value. They also benefit from a feedback effect by which spread of the narrative drives up the stock price and the rising stock price is then interpreted as evidence for the veracity of the narrative. Of course, the spread of a narrative and the feedback effect can operate in both directions. A narrative that arises, spreads, and drives stock prices to new highs can collapse just as quickly.

Introduction

Tesla has done it again. As Exhibit 1 shows, between the end of 2019 and early 2021, the price of Tesla rose dramatically creating over $600 billion in investor wealth. The exact size of the run-up depends on the dates selected, but whatever dates are chosen the price increase was on the order of 10x or more. The sample used here runs from the first trading day of December 2019 through the current date (as of the initiation of this research) of April 30, 2021. On December 2, 2019, Tesla was trading at a split-adjusted price of $66.97. On April 30, 3021, it closed at $709.44, a price increase of 10.6x. Had the high-water mark of $883.09 in January been used as the end date, the run-up would have been more than 13x. To make matters more extraordinary, the run-up did not begin from a low market value as was the case with an earlier Tesla run-up analyzed by Cornell and Damodaran (2014). On December 2, 2019, the market capitalization of Tesla was $60.3 billion compared to $51.3 billion for General Motors. By April 30, the market capitalization of Tesla had risen to $672.4 billion while GM had increased, but only to $81.9 billion.

Of course, there are other examples of huge run-ups during the same period. The most famous recent example is GameStop whose price gyrations even attracted the attention of Congress. But what makes Tesla unique is the sheer size of the value created. The more than $600 billion that Tesla added to its equity value during the sixteen-month sample period we study would have made it one of the ten most valuable companies in the world by market cap. During the period, the company, and its chairman Elon Musk, were at the center of a worldwide media blitz. No development, or even rumor, involving Tesla went unnoticed. Not surprisingly, Tesla was one of the most actively traded companies in the world. Given all of this attention and activity, if the change in Tesla’s value from December 2 to April 30 cannot be explained on the basis of fundamentals, it raises interesting questions regarding the concept of market efficiency.

The first challenge undertaken is trying to explain the rise in Tesla’s market cap on the basis of valuation fundamentals. Were there changes to the company, the industry, and the economy sufficient to rationalize such a massive appreciation? The approach taken is comparing relative valuations on two nearly contemporaneous dates because it is far easier then attempting to value the company at either date. As Summers (1985) quipped long ago, it is easy to estimate the value of a two-quart bottle of ketchup if you can observe the price of a one-quart bottle, but pricing either bottle in terms of the underlying demand and supply for ketchup is far more challenging. The same is true of stocks, particularly stocks like Tesla with such a controversial future. There is always a combination of cash flow forecasts and discount rate that will rationalize any price. As a result, debates about Tesla’s valuation typically devolve into arguments whether the inputs reasonable. One way to get around those debates, at least to an extent, is to analyze changes in price over relatively short periods of time. It is far easier to ask whether it is reasonable to assume that an input has changed over a short time interval, than to assess the level of that input at any point in time. For Tesla’s market cap to grow by a factor of 10x from an already large base something dramatic must have changed. The question is: what was it?

Valuation factors

In a rational valuation model changes in value must be due to changes in either expected cash flows, discount rates, or some combination of the two. While the foregoing is a truism, it hides a good deal of complexity because many factors can impact expected cash flows and discount rates. To attempt to make sense of Tesla’s extraordinary run-up and value creation, it is necessary to dig deeper to identify and examine those factors.

Discount rate-related factors

Discount rates are determined by three factors: (1) the risk-free rate, (2) premiums on priced risk factors, (3) Tesla’s sensitivities to the priced risk factors. With regard to the risk-free rate, the yield on 10-year Treasury bonds, the asset most frequently used as a proxy for the risk-free rate in valuation analysis, was 1.78% on December 2 and 1.64% on April 30. Such a small decrease explains almost none of the 10x run-up.

Dealing with factors premiums and factor sensitivities is more difficult. As Harvey, Liu, and Zhu (2016) document there is an immense literature on the subject that proposes a host of factors all with different premiums. The point here is that no matter what asset pricing model is chosen, it is difficult to argue that Tesla’s risk premium declined measurably over the sample period. To the extent there was risk added by the volatility induced by Covid, that presumably would have increased risk premiums.

The risk premium issue is one of the key benefits of looking at the valuation of Tesla at two nearby points in time. Although estimating the risk premium for Tesla is a highly controversial undertaking, it is hard to imagine a model that would imply a significant drop in the premium between December 2, 2019 and April 30, 2021.

Cash flow-related factors

Macroeconomic conditions

At the highest level, a company’s cash flow will be affected by macroeconomic conditions. While macroeconomic conditions affect stock prices, they tend to have a good deal of inertia and generally change somewhat slowly and by relatively small amounts. This makes it difficult to see how they could explain much of a 10x run-up. But putting the general observation aside, to the extent there were changes between December 2 and April 30, they were typically in the wrong direction. As of December 2, 2019, the economy was humming along. The unemployment rate of 3.6% was close to an all time low. Inflation was steady at less than 2%. The economy had not been through a recession since the great financial crisis. Corporate tax rates were low by historical standards following the tax reform act of 2017.

As of April 30, conditions were less favorable. Although the economy was recovering from the Covid pandemic, things were not yet back to normal. The rate of unemployment was down from Covid induced highs, but it was still at 6.1%. There were renewed fears of rising inflation caused by the massive government monetary and fiscal stimuluses used of offset the economic damage caused by inflation. What is more, the new President was proposing significant new taxes to help finance the growing government deficit. Even though GDP was recovering, it was still below the trend path it was on prior to the Covid shock.

Although not a macroeconomic event per se, the election of Joe Biden was a plus for the EV industry. As part of his plan to combat global warming, Mr. Biden floated proposals to increase subsidies for the EV industry. What specific programs will be instituted, in any, remains uncertain.

To conclude, while it is difficult to construct an index of “macroeconomic conditions,” it seems safe to conclude that those conditions were no better on April 30 than they were on December 2. The one possible exception to this conclusion, is the possible introduction of new subsidies for the EV industry. Overall, however, there was no dramatic improvement in macroeconomic conditions that could explain the 10x growth in Tesla’s market capitalization.

The industry and competition

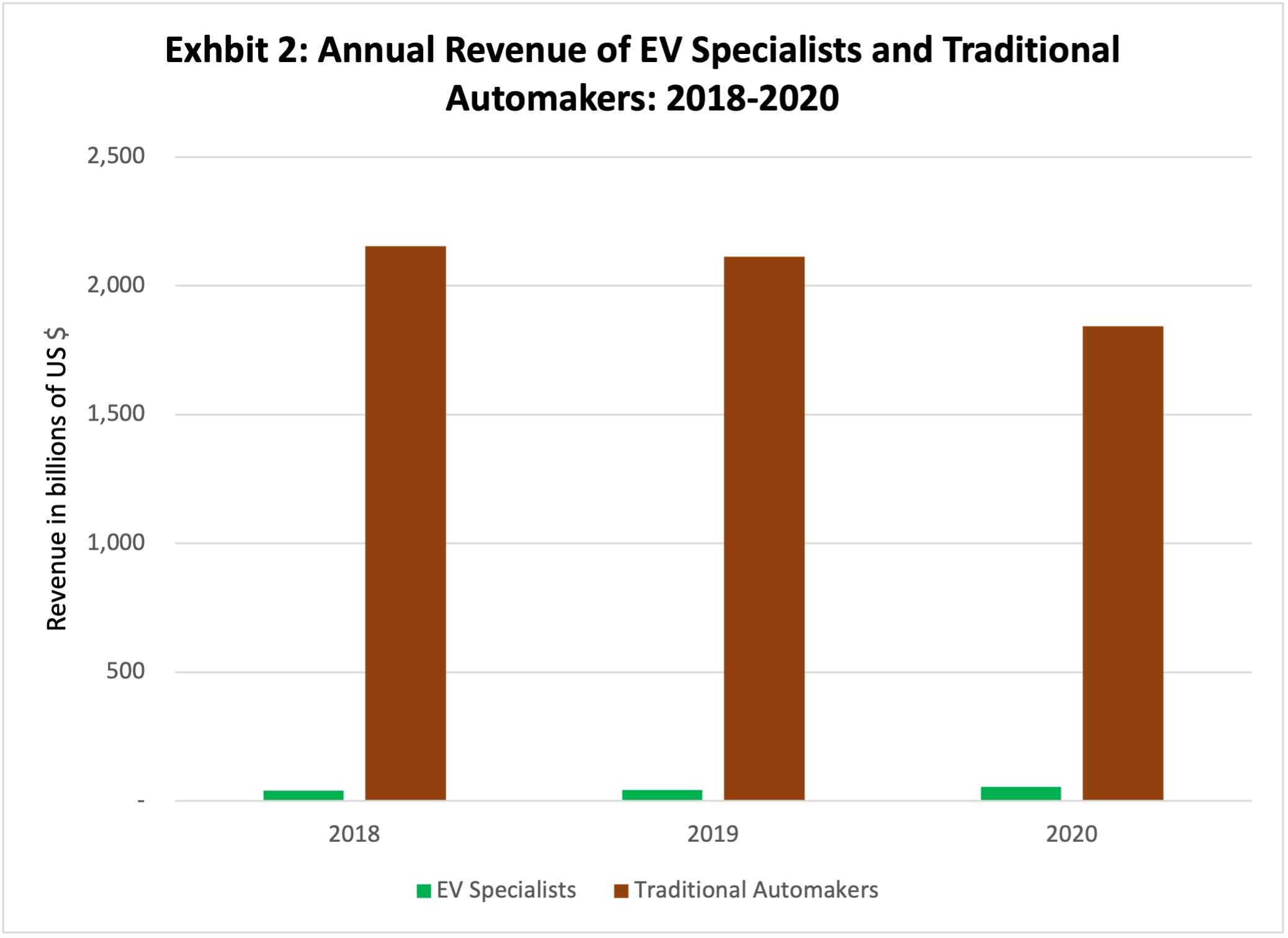

The electric vehicle industry news during the sample period was positive. One source of stimulus were the new regulatory policies and new incentives instituted by various governments to promote zero-emissions vehicles. In addition, the public was warming to EVs. It is not surprising, therefore, that EV sales grew to 3.25 million in 2020, an increase of 43% on a year-over-year basis. The downside is that high growth rate was due in large part to the low starting point compared to the sales of ICE vehicles. To provide perspective, Exhibit 2 presents data on revenue from sales of cars for the three years from 2018 through the 2020. As shown, revenues reported by EV specialists remained a tiny fraction of those reported by traditional ICE automakers.

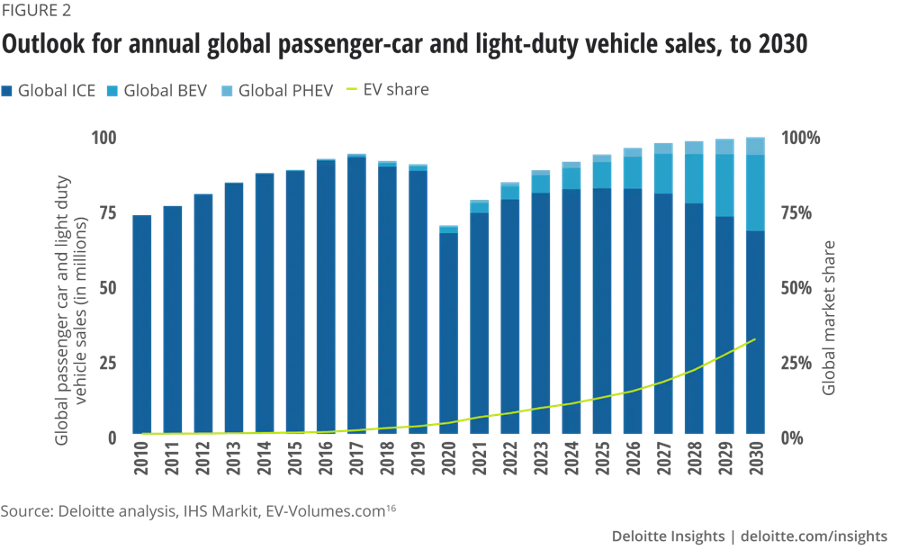

What moves the market, however, is not history but changes in expectations regarding future cash flows and discount rates. Given the diversity of opinions, it is difficult to determine exactly how expectations changed during the period. Despite the enthusiasm for EVs, changes in the pattern of actual purchases tends to be sluggish and experts in the field of projecting future sales know this. An example of typical projections are those published by Deloitte in July 2020 and presented as Exhibit 3.[1] The projections show a ramp-up but that ramp-up is similar to those from other sources published at various times during the sample period. There is no pronounced tendency for projections made later in the period to show larger long-run growth than those made earlier. There is certainly no change in projections sufficient to explain anything close to a 10x change in market cap for the largest firm in the EV space.

Exhibit 3: Deloitte projections for light-duty vehicle sales

There is a more fundamental problem when attempting to explain the 10x jump in Tesla’s valuation, even if there was growing enthusiasm for EVs during the sample period. No matter how rapidly the industry grows, for an individual company to earn returns in excess of the cost of capital, there must be barriers that prevent competitors from entering. Such barriers are what allowed Amazon, Google, and Facebook to build dominate positions in their industry and achieve market capitalizations even in excess of Tesla’s. The problem Tesla faces is that in a competitive, capital intensive, industry, market disruption may benefits society at large, but not necessarily the disrupters, who are often disrupted themselves in due course.

To explain the jump in Tesla’s price on the basis of industry domination, there must have been positive news between December 2 and April 30 regarding Tesla’s competitive position in the automotive industry. The problem is that just the reverse was the case. Between those two dates, there dozens of announcements of EV plans from both traditional automakers and new EV startups. Activity was particularly pronounced in China where both Nio and XPeng ramped up production and several new startups entered the space including electronics giant Xiaomi. In Europe, VW began selling two new electric cars and soon surpassed Tesla to become the best seller of EVs in Europe. VW said it expects to have 70 EV models by 2028. Porsche began shipping its electric Taycan. Audi expanded its line of EVs, including competitors to both Tesla’s Model S and X. In Japan, Toyota said it is targeting cumulative sales of 5.5 million electric vehicles by 2025. In South Korea, Hyundai plans to invest $87 billion to finance electrification of its vehicles by 2025. Finally, in the United States Ford introduced the Mustang Mach E to compete with the Model 3 and Model Y, promised an electric F150 pickup truck, and partnered with electric truck startup Rivian. Not to be denied, Mary Barra stated that GM would have 20 EV-models available by 2023. The company also introduced a new electric Cadillac sedan, an electric Hummer, and updated the Bolt to better compete with the Model 3 and Model Y. And all of this was just a part of the activity. In short, there was a huge surge of competition in the EV space.

One odd thing is that during the period between December 2 and April 30, the stock prices of virtually all the EV specialists shot up. No one gained anything like the $600 billion increase in market cap experienced by Tesla, but Arnott, Cornell and Wu (2021) report that during approximately the same time interval the market capitalization of EV specialists other than Tesla rose $250 billion. Even the prices of traditional manufacturers rose when they started announcing their EV plans. Arnott, Cornell and Wu argue that the experience of the EV market is an example of what Cornell and Damodaran (2020) call the big market delusion. The hallmark of a big market delusion is when all the firms in an evolving industry rise together even though they are often direct competitors. Investors become so enthusiastic that each firm is priced as if it will be a major winner in the developing big market despite the fact that this is a fallacy of composition: the sum of the parts cannot be greater than the whole.

Unfortunately, the big market delusion does not provide a fundamental explanation for the Tesla run-up, it simply suggests that that whatever force was driving Tesla up may have affected other EV specialists as well. We return to this issue below.

Company specific information

It is hard to justify any abnormal upward movement in the price of Tesla stock during the sample period, let alone an increase of 10x, based on the company specific information that became available during the sample period. At the start of 2020, the company projected that vehicle deliveries would comfortably exceed 500,000 during the year. Actual deliveries were 499,000. The company also predicted it would be self funding in 2020. In fact, there were three equity sales in February, September, and December which raised $12 billion.

With regard the company’s products, the Model S and X were both getting long in the tooth and sales were falling. The majority of sales during the sample period were of the Model 3 which was launched in July 2017. Next in line was the Model Y for which deliveries began in March of 2020. At the beginning of the year, Tesla had said that the Semi truck would be in limited production by the end of 2020. By the end of the year, the limited production date had been moved back to late 2021. Tesla’s newest product was the Cybertruck which was unveiled just before the start of the sample period in November 2019. The Cybertruck’s design was so radical that many questioned whether it would ever be produced in volume. By the end of the sample period in April 2021, there was still no firm date for the start of production of the Cybertruck.

In 2020, Tesla announced that it would be opening two new factories. One in Austin, Texas and the other outside Berlin in Germany. Neither announcement was much of a surprise other than the locations. It was clear that to meet its production goals Tesla would need new factories in addition to its Fremont plant. If there was any surprise during the run-up period it was that the German plant was proceeding more slowly than planned because of regulatory issues.

In summary, the company specific information arriving during the period appears to be largely neutral, or even negative, compared to company statements and investor expectations at the start of the period. It is certainly not an explanation for the 10x increase in the stock price.

Fundamental valuations

As part of his ongoing research, Damodaran has regularly posted DCF valuations of Tesla on his website. In January 2020, when Tesla was priced at $116.20, Damodaran posted a DCF valuation of Tesla of $85.32.[2] Damodaran’s valuation, though below the then current market price, could hardly be called pessimistic. He projected revenue growing at 25% for the next five years before slowing over the following five years to the growth rate of the aggregate economy. As the company grew, he assumed EBIT margins would increase to 12%, near the top of the auto industry. His cost of capital, essentially equal to the cost of equity because Tesla had little debt, was 7.0% which is low for a high-tech company. Even with all these bullish assumptions, his valuation did not match the current stock price, and this was before Tesla began its rapid ascent.

By April of 2021, Damodaran had more than doubled his valuation upward to $178.19. The increase was due to a number of factors. First, he increased the starting revenue from $24.6 billion to $31.6 billion. Second, he increased the five-year revenue growth rate from 25% to 30%. Third, he reduced the cost of capital from 7.00% to a remarkably low 5.98%. Finally, the increased the sales-to-capital ratio from 5 to 3 which has the effect of reducing necessary capital expenditures. Despite all these bullish new assumptions, the increase in the fundamental valuation paled in comparison with the jump in the stock price. Whereas his valuation was 73% of the stock price at the start of the sample period, by the end of the sample it was only 25% of the price of $709.44.

The Damodaran valuations are similar to valuations produced by Cornell (2020) for the Cornell Capital Group (CCG) in November 2020. At the time, Tesla was trading at approximately $500 per share. Despite assuming rapid growth and industry leading operating margins for Tesla, the CCG base case valuation was $144.71. The valuation analysis noted that at the time Tesla’s nearest comparable in terms of market capitalization was Warren Buffett’s Berkshire Hathaway. In its previous fiscal year Berkshire had revenues of $327 billion and earnings before interest and taxes, EBIT, of $107 billion. In comparison, Tesla had revenue of $25 billion and an EBIT of negative $0.6 billion. Although not as current as Damodaran’s April valuation, the CCG analysis took account of much the new information that arrived during the sample period and still was unable to arrive at a valuation close to Tesla’s stock price.

It is worth noting, particularly in light of what follows, that both Damodaran and Cornell received strident push back on the internet, and even personal insults and threats, related to their valuations of Tesla. The people sending those personal comments had adopted a far different view of Tesla based on the notion that the company was more than an automaker. By valuing Tesla primarily as a car company, the critics argued that the Damodaran and Cornell DCF models excluded a majority of Tesla’s value.

The role of narratives

Research by Damodaran (2017) and Shiller (2019), among others, stresses the role of narratives in the pricing of equities. As Shiller puts it, the key proposition of his book is that “economic fluctuations are substantially driven by contagion of over simplified and easily transmitted variants of economic narratives.” Shiller observes that the role of narratives is particularly important in stock markets. Unlike changes in operations, which tend to be sluggish, narratives can arise and spread with remarkable speed making it possible for them to have a dramatic impact on stock prices in short periods of time. Although it is difficult to pin down precisely, the narrative involving Tesla appeared to evolve and spread during the period from December 2 to April 30, so the narrative hypothesis is worthy of consideration.

Damodaran argues to become successful, in the sense of going viral and influencing investor behavior, a narrative should have four properties.

- It has to be simple. A simple story that makes sense will leave a more lasting impression than a complex story in which it is tough to make connection.

- It has to be credible. Business stories need to be credible for investors to act on them. If the story does not hold together, investors are less likely to accept it.

- It has to inspire. Business stories are not designed to win literary awards, but to inspire the audience to buy into the premise. The more passion the better.

- It has to lead to action. Once the audience buys into the story it has to lead to action. With investment stories the proposed action is clear – buying the stock or related derivatives.

Tesla checks all the boxes and adds one as well. It is a company that has the potential to be in multiple businesses, from green energy to automobiles to software, plus it has a master storyteller in Elon Musk, who keeps investors guessing about the next turn in the story. Consequently, the range of stories that are plausible for the company is extraordinarily wide ranging, allowing for different investor to arrive at different valuations for the company, at the same point in time. This divergence in stories has always characterized the company and explains the wide swings in its stock price, and extensive run-up and run downs as one set of narratives or another takes hold. Finally, since these narratives are all about something that will happen in the distant future, it is difficult to rule out narratives as impossible. Investors are always one good news or bad news story away from a narrative shift.

The company has also attracted a following from high profile analysts and investors who became advocates for their own narratives. Perhaps the most renown Tesla advocate was fund manager Cathie Wood. Wood’s thesis was that it was a mistake to think of Tesla as a car company despite the fact that virtually all of the company’s revenues came from the sales of cars or automotive credits. Echoing statements by Tesla’s chairman Elon Musk, Wood argued that Tesla would be remembered not just as an EV company but as a renewable energy, artificial intelligence, and robotics company. In addition, Wood claimed that Tesla would also become a global leader in ride sharing, energy storage, and green energy. Based on this thesis, in February 2020 Wood put a five-year price target of $7,000 on Tesla.[3]

Wood was not alone. Adam Jonas of Morgan Stanley stated that Tesla was on the verge of a “Model-T moment” that would revolutionize the transportation industry. Along with fund manager Jed Dorsheimer, Jonas claimed that Tesla was comparable to Apple in that it would create a money-spinning ecosystem of goods and services that reinforce each other. The high margins for Tesla would not come from the vehicles, but software and connected services like maps, self-driving, and entertainment. Of course, all this was supplemented by incessant internet chatter by thousands of Tesla acolytes.

The narrative hypothesis also opens the door to a feedback between the narrative and the stock price. First, spread of the narrative drives up the stock price. Next, the rising stock price becomes evidence of the narrative’s veracity and leads to its more widespread adoption, which in turns leads to further increase in the stock price. Evidence for the feedback can be found in the trading data. The three exhibits below provide an illustration. Exhibit 4 plots Tesla stock price and dollar trading volume. Exhibit 5 plots the stock price and option trading volume. Exhibit 6 plots the stock price against the Google trend index. Although there is not a precise day-by-day correlation between the two variables in any of the three charts, there are some general relationships. Specifically, stock volume, option volume, and Google searches are all tend to be high when the stock price is rising most sharply. It is worth noting the Mr. Musk injected noise into the Google measure because some of the “Tesla” searches involved him personally or his personal relation to the company. An example is his promotion of cryptocurrencies and his decision to have Tesla invest $1.5 billion in Bitcoin.

Further evidence in support of the narrative hypothesis is provided by the behavior of Tesla’s stock price in response to the company’s stock split. On August 11, 2020 after the market closed, Tesla announced that the company would be splitting its common stock 5-for-1. It is well known that stock splits, in and of themselves, have no impact on fundamental value. Nonetheless, as soon as Mr. Musk made the announcement Tesla’s price jumped more than 6% in the after-market. The following day, on the basis of no apparent news with respect to fundamentals, the stock price went on a wild ride before closing up 13.12%. But that was not enough. The next day, despite some oscillations, it ended up another 4.26%. Over the two days the total return was 17.94%. Only a small fraction of this run-up can be attributed to the market. It is hard to explain such a large response to such an apparently value neutral event without appealing to the hypothesis that the split added fuel to the fire of the Tesla narrative.

The same is true of Tesla’s inclusion in the S&P 500. Arnott, Kalesnik and Wu (2020) report that on November 16, 2020 S&P Dow Jones Indices announced that Tesla would join the S&P 500 Index. The inclusion had been widely anticipated. Nonetheless, from the announcement date through December 7, Tesla’s stock price rose 49% as the internet lit up with enthusiasm regarding forthcoming inclusion. While part of the increase may have been due to the mechanical requirement of index funds to purchase Tesla shares, the size of the increase suggests that the narratives played an important role.

The narrative hypothesis is not an argument against intrinsic valuation but an explanation for why, even in the context of intrinsic valuation and assuming market efficiency (in the long term, at least), stock prices at Tesla embark on runs that seem to be irrational. But a conclusion that the runs are evidence of inefficiency overlooks the fact that narratives are part of information set that affects stock prices and enters into fundamental valuation. In this context, “irrationality” basically means rejecting one narrative in favor another. As many Tesla short sellers can attest, people who bet against the company’s narrative have lost immense amounts of money thus far. That said, it is a mistake to accept any price for Tesla as reasonable just because there is some narrative that produces that value in the context of a DCF model. The question in investing is whether that break even narrative, i.e., the story needed to justify the price is probable, not just plausible.

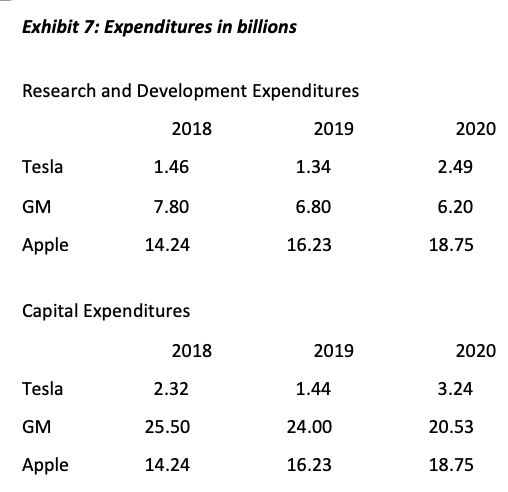

In this regard, there is one fact worth noting. The core of the narrative hypothesis is that Tesla is not just a car company, but a firm primed to enter, disrupt, and become a leader in a variety of other profitable businesses. Doing so, however, requires capital expenditures and expenditures on research and development. A natural question to ask, therefore, is whether Tesla expenditures are comparable to other automobile manufacturers and to the tech companies to which the bullish narrative compares it. Exhibit xx provides the answer. The exhibit shows that both Tesla’s capex and its research and development expenditure are both on the order of 10% of GM and Apple. It is hard to see how Tesla could come to dominate the auto industry, let alone enter, disrupt and eventually dominate new lines of business, on such a meager budget for capex and research and development.

In closing, perhaps the best support for the narrative hypothesis is that “there is no reasonable alternative.” None of the fundamental factors, nor all of them put together, could come close to explaining the 10x increase in price.

Market efficiency?

Because the 10x Tesla run-up in 17 months cannot be explained by changing company, industry, or macroeconomy developments, it is tempting to conclude that the market for the stock was inefficient. But that conclusion does not take proper account of the role of the Tesla narrative. The efficient market hypothesis states that stock prices reflect all publicly available information, and as noted above the narrative is clearly part of that information set. As a result, determining whether or not the market is efficient amounts to assessing the reasonableness of competing narratives. Damodaran and Cornell have argued that the stock is mispriced based on their DCF analyses. But that conclusion follows from the fact that those DCF valuations do not give meaningful weight to the transformative entry by Tesla into fields such as green energy, artificial intelligence, autonomous vehicles, and ride sharing envisioned by Cathie Wood and others who promote bullish narratives. Saying that the post run-up price of Tesla is evidence of market inefficiency is equivalent to saying that those narratives are wrong. Because such a conclusion will always be a matter of judgment, the question of market efficiency reduces to philosophical debate regarding narratives. Even a collapse in the price of Tesla to levels consistent with Damodaran and Cornell DCF models would not necessarily imply the market was previously inefficient. It could have been the case that information arrived, through some complicated process, that caused people to stop accepting the bullish narrative. An efficient market would then reflect that new information.

Conclusion

The bottom line is that the 10x jump in the price of Tesla stock between December 2, 2019 and April 30, 2021 cannot be explained by the arrival of fundamental information regarding the macroeconomy, the auto industry, or company specific information related to Tesla as an electric vehicle manufacturer. Based on that information, either the price was too low on December 2, too high on April 30, or some combination of the two. Discounted cash flow models produced by Damodaran and Cornell suggest the main culprit was overpricing at the later date.

The reason the Damodaran and Cornell models produces values much less than the market price is that do not incorporate what was a growing narrative during the sample period that Tesla is more than a car company. As stated by Mr. Musk, and echoed by Cathie Wood and others, Tesla is also a renewable energy, artificial intelligence, ride sharing, and robotics company. According to the narrative, it is via these other avenues, as opposed to solely the competitive auto industry, that Tesla will create much of its value. The analysis presented here suggest that a growing acceptance of this narrative is the only reasonable explanation for Tesla’s 10x run-up. Narratives have the advantage that they can blossom and replicate with little in the way of capital expenditure and improvements in operations both of which tend to have a sluggish impact on value. They also benefit from a feedback effect by which spread of the narrative drives up the stock price and the rising stock price is then interpreted as evidence for the veracity of the narrative. Of course, the spread of the narrative and the feedback effect can operate in both directions. A narrative that arises, spreads, and drives stock prices to new highs can collapse just as quickly.

Bradford Cornell is a Professor of Finance at the Anderson Graduate School of Management, UCLA, and a senior advisor, Cornell Capital Group.

References

Arnott, Rob Kalesnik and Lilian Wu, 2020, Tesla, The largest-cap stock ever to enter the S&P 500: A buy signal or a bubble, Research Affiliates, December, 1-12.

Arnott, Rob, Bradford Cornell and Lillian Wu, 2021, Big market delusion: Electric vehicles, Research Affiliates, March, 1-9.

Cornell, Bradford and Aswath Damodaran, 2020, Big market delusion: Valuation and investment implications, Financial Analysts Journal, 76, 2, 15-25.

Cornell, Bradford and Aswath Damodaran, 2014, Tesla: Anatomy of a run-up, Journal of Portfolio Management, 41,1, 139-151.

Cornell, Bradford, 2020, The Tesla stock split experiment, Journal of Asset Management, 21, 647-651.

Cornell, Bradford, 2020, Tesla unhinged, https://www.valuewalk.com/2020/11/three-valuation-scenarios-tesla-inc.

Harvey, Campbell R., Yan Liu, and Heqing Zhu, 2016, ...and the cross-section of expected returns, Review of Financial Studies, 29, 5–68.

Damodaran, Aswath, 2017, Narrative and Numbers, Columbia University Press, New York, NY.

Shiller, Robert J., 2019, Narrative Economics, Princeton University Press, Princeton, NJ.

Summers, Lawrence H., 1985, On economics and finance, Journal of Finance, 40, 3, 633-635.

[1] https://www2.deloitte.com/us/en/insights/focus/future-of-mobility/electric-vehicle-trends-2030.html.

[2] The January Damodaran valuation is available online. The January 2020 valuation is at http://aswathdamodaran.blogspot.com/2020/01/an-ode-to-luck-revisiting-my-tesla.html. The April 2020 valuation is not posted but will be supplied with a request to the author.

[3] See, https://www.cnbc.com/2020/02/05/tesla-shares-could-reach-7000-in-next-5-years-catherine-wood-says.html.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All