Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisors can use their CRMs for various workflows and notifications to increase client touchpoints. Those who are involved in key life events have set up a Medicare-related notification for clients who are approaching their initial eligibility period. This is an important time for clients as they will be making a decision on how to configure their health insurance for the rest of their life.

But Medicare isn’t a “one-and-done” deal. You need to revisit the conversation regularly depending on the time of year or certain events to ensure it is still in line with your clients’ needs and budgets. Here are a few key examples.

Part D coverage during open enrollment

The first and most applicable opportunity to revisit clients’ coverage is during the open enrollment period from October 15 to December 7 every year. During this time, you can revisit drug coverage (Part D) and change plans, effective the first day of the following year.

This is important for a number of reasons. If you aren’t on any medications when first enrolling in Medicare, you can opt for the drug plan with the lowest possible monthly premium. If you take a few generic brands, you can determine the most cost-effective plan either directly on Medicare.gov or by working with a professional. As you age, it is likely that your medication list will grow and certain drugs on that list will be expensive. This is where revisiting Part D coverage comes in handy. Clients can find a new plan every fall that better fits their needs for the upcoming year.

You can set a notification for this time of year for all clients that have prescription drug coverage through original Medicare (Part D) or Medicare Advantage. This is especially applicable for clients who have had new or growing health issues in the last year. Revisiting their coverage and looking for better suited options could go a long way in your relationship with them.

As an aside, I’ve been in the middle between advisors and clients who have received bad advice in the past and chose not to enroll in Part D for a variety of reasons. It is mandatory without another source of creditable drug coverage; you should ensure clients don’t pass on their initial enrollment opportunity to sign up, which is usually at age 65 or within two months of their last month of employment. They will otherwise be subject to a penalty for the months they were not enrolled. Plans can run as low as $7 per month, so it is cheap in comparison to a lifelong penalty if drug coverage is needed down the line.

The “trial right”

It’s always nice to be able to give something a test drive before committing to it long term. This is luckily the case for you if are in your first year of a Medicare Advantage plan.

There are key differences between original Medicare and Medicare Advantage – that’s an article for another time – and it is possible that clients may not like their Advantage plan, which replaces their medical coverage with a commercial carrier, and want to switch to original Medicare, which involves Medigap and Part D.

The “trial right” applies in two cases:

- If you have joined a Medicare Advantage plan when you were first eligible for Medicare Part A at 65, and within the first year of joining you decide you want to switch to Original Medicare; and

- If you dropped a Medigap policy to join a Medicare Advantage plan for the first time, you’ve been in that plan for less than a year, and you want to switch back.

In both cases, you have what is called “guaranteed issue rights” to a Medigap policy. Insurance carriers must sell you the policy, cover pre-existing conditions, and can’t charge you more because of past or present health conditions. You can make the switch as early as 60 calendar days before the date your coverage will end and no later than 63 calendar days after your coverage ends.

There is a small subtlety between the two use cases. In the first case, you have the right to buy any Medigap policy that’s sold by any insurance company in your state. For the second case, however, you must join the same Medigap policy you had previously, but if that isn’t available through that insurance company anymore, then you can buy any lettered plan.

Set a notification that reminds you to check in around nine months into a client’s first year being enrolled in a Medicare Advantage plan to ensure it is filling their needs from a health care and budget standpoint. This will increase your engagement with clients on a very important topic and an area of increasing expense as they age. There are even states that have this trial right annually, such as Missouri, New York and Washington, which can add further client touchpoints.

The birthday or anniversary rule in California, Oregon and Missouri

Depending on where your clients live, there could be additional opportunities for additional client touch points that you haven’t yet considered.

The “birthday rule,” which is not to be confused with an identical term referring to which parent’s health plan will be designated as the primary plan for a newborn, is applicable to California and Oregon residents. In those two states, you can switch your Medicare Supplement (Medigap) plan within a 60-day window surrounding your birthday every single year without medical underwriting. Similarly, a law in Missouri called the “anniversary rule” allows for you to change your Medigap plan 30 days before or 30 days after your policy’s annual renewal date.

But this is healthcare, after all, so there are nuances.

To qualify, you must switch to a plan of equal or lesser benefits. All lettered plans are created equal, meaning that every Plan G provides the same benefits no matter who the commercial carrier is. That means that you could switch from a Plan G insured through Cigna to Humana, for instance, and not experience any change in benefits.

Those who reside in those states can shop around every year to see if there is the same lettered plan available to reduce the costs of their monthly premiums, especially if they are unsatisfied with their current carrier. Plan Gs in California currently run from $138 to $205 – again, even though the benefits are identical on all plans – so there are certainly opportunities available to save on premiums.

Interestingly, I learned firsthand through conversations with both Medicare and the California Department of Insurance that you can also freely switch back and forth between a Plan G and a high-deductible Plan G. These plans are of equal benefits, even though there is a difference in the deductible and, as a result, the monthly premium. For low healthcare utilizers, they could save thousands on a high-deductible Plan G and then switch to a Plan G as utilization starts to increase with age. This is also applicable to those who may still have access to Plan F and its high deductible version.

In other states, those with a Medigap plan who want to make a switch to a better-priced competitor during Medicare’s open enrollment period from October 15 to December 7 every year must go through medical underwriting, meaning they must fill out an application and disclose details about their health status to be approved. They could be denied coverage if they have any pre-existing conditions.

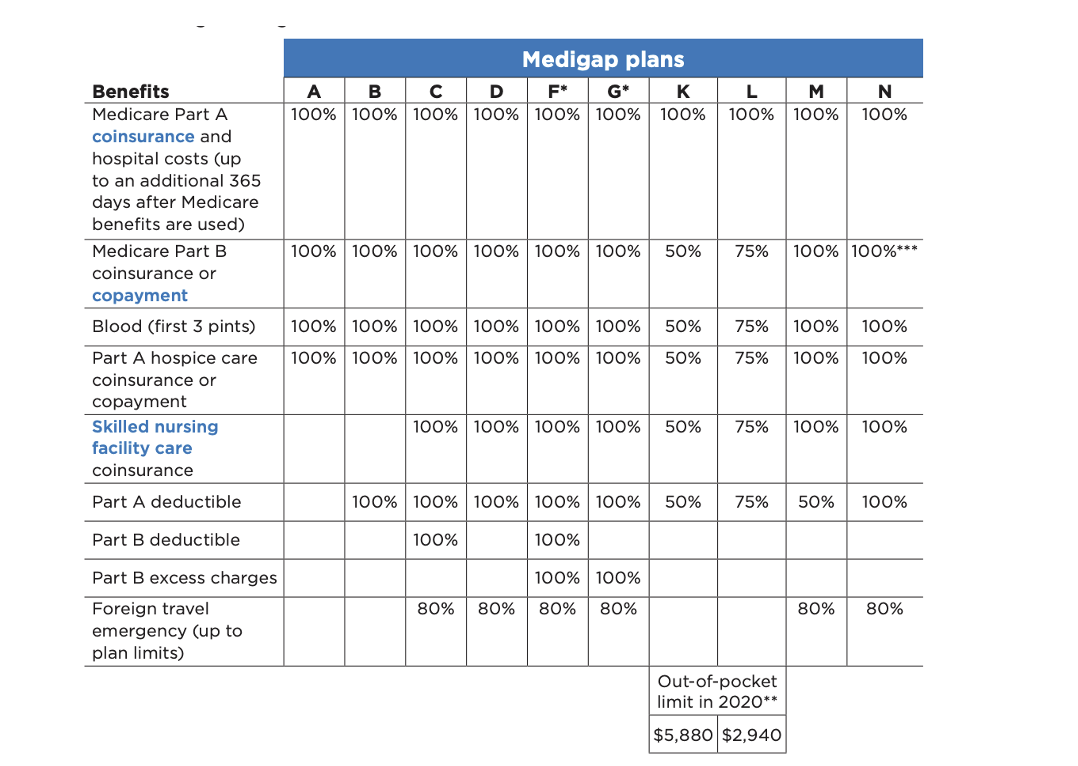

As mentioned, you can also switch your Medigap plan to a lettered plan with lesser benefits, meaning the new plan would be to the left of the previous plan on the chart below. Caution should be exercised when switching to plans with lesser benefits as it can be easy to look for a lower cost alternative but hard to understand the differences in benefits. Consult with a professional if clients are looking to make a switch like this.

Table demonstrating the various Medigap plan letters and their benefits taken from the Medicare and You Handbook 2021.

Set a reminder in your CRM for these dates annually to ask clients how satisfied they are with their current plan and if they want to explore making changes. Be sure to wish those in CA or OR a happy birthday while you’re at it!

Christine Simone is a co-founder of Caribou, a healthcare planning and navigation solution for financial advisors. She often writes on the topics of healthcare and women in tech. Caribou is a proud sponsor of the upcoming Alliance of Comprehensive Planners Conference in October 2021.

Read more articles by Christine Simone

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.