Experts Play with the Forms of Money

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

To understand the process by which physical coins became accepted tender in the 19th century, one should start with the wisdom of Yogi Berra and Niels Bohr.

Yogi Berra usually gets credit for the saying, “It is difficult to make predictions, especially about the future.” But this insight was first expressed in a modern vernacular by the physicist Niels Bohr. In the same interview where he commented on the probabilities for successful estimation, Bohr was also asked how he had become such an expert about the difficult subject of quantum physics. The answer, Bohr said, was simple: An “expert is someone who has made all the mistakes that can be made in a very narrow field.”

For the mechanics, bank clerks and tradesmen who founded Philadelphia’s Olympic Base Ball Club in 1835, the business of predicting the future was as difficult as always. As the pioneers in a new sport, they were still inventing the rules; as Americans who lived in a world of acquiring and spending, the Olympians considered themselves to be well on their way to being experts about money.

By accident and design, in its first half century as a constitutional republic, the United States of America had developed a political economy in which local bank credit paper was the general medium of exchange. The printed notes of state-chartered banks had become the nearly universal substitute for actual money. By the end of 1836, the accounts for those banks showed $145 million outstanding and in circulation. To win the wars against the U.S. colonies and Napoleonic France, the United Kingdom had adopted a similar expedient. Parliament had allowed the notes of the Bank of England to circulate freely as money without any promise of redemption. But, under its central bank system, the English had been determined to return their national currency to coin. The goal of resumption was not to reassure note holders that England’s money was worth something; it was to subordinate credit issuance in general to the limits of specie reserves so that all risks of inflation could be avoided. Even as colonial Americans had taken a different monetary path, they had chosen to use credit for exchanges and have prices inflate and deflate against the standard set by the coin they did not have. Their first national bank had issued notes that were not legal tender; their first banking laws had defined bank capital requirements but left the level of mandatory specie reserves unspecified. Congress and President Madison had given the second Bank of the United States the authority of a central bank. but, during its 20-year term, it had rarely been unable to exercise the Bank of England’s sovereign control. In 1836, against the $145 million in state-chartered bank notes, the Bank of the United States had only $16.4 million of its notes in circulation.

Nearly everyone in the United States who could vote thought that the American financial system needed fixing. Andrew Jackson’s Democrats were pleased to have destroyed the United States’ own copy of the Bank of England, but they were troubled by the extraordinary spread of popular credit. The Specie Circular had guaranteed that the federal government would stand apart from all exchanges of bank notes and their discounting; the Treasury would only deal in coin. Once the Independent Treasury was established, the specie would be kept in its own federal vaults. The Whigs were not willing to give up on their hopes of restoring a national bank, but they could compromise with President Jackson on the question of the distribution of the federal government’s surplus gold. In the absence of any federal debt and with an end to the excess spending for the Seminole Wars, the Treasury was in the position to send coin to the states. The Distribution Act, to take effect January 1, 1837, would have the virtue of restraining the issue of wildcat bank notes. To qualify as “good,” bank eligible to receive its part of a state’s share of the surplus, a state-chartered bank would have to end all issues of demand notes in denominations of less than $5.

At least the problem of scarce coin had been resolved. The Currency Act passed in 1834 had changed the ratio of the weights of coins from 16-to-1 silver to gold to 15-to-1, making silver the precious metal whose coins were worth more as bullion than they were as money. All the gold that had been hoarded or shipped abroad came into circulation. Mexican silver dollars, which had been the only form of coined money in broad supply, disappeared from circulation. Pieces of eight were replaced by U.S. Mint production of half dollars, quarters, dimes and half-dimes; the market value of the metal in the new coins was sufficiently less than their denominations, such that melting them down for bullion became permanently unprofitable. Thanks to Franklin Peale’s new steam press, the U. S. Mint was able to produce record amounts of currency. In 1837, it would produce a total of $2,477,500 in secondary coinage: 2.3 million half dimes, 1 million dimes, .25 million quarters and 3.6 million half dollars.

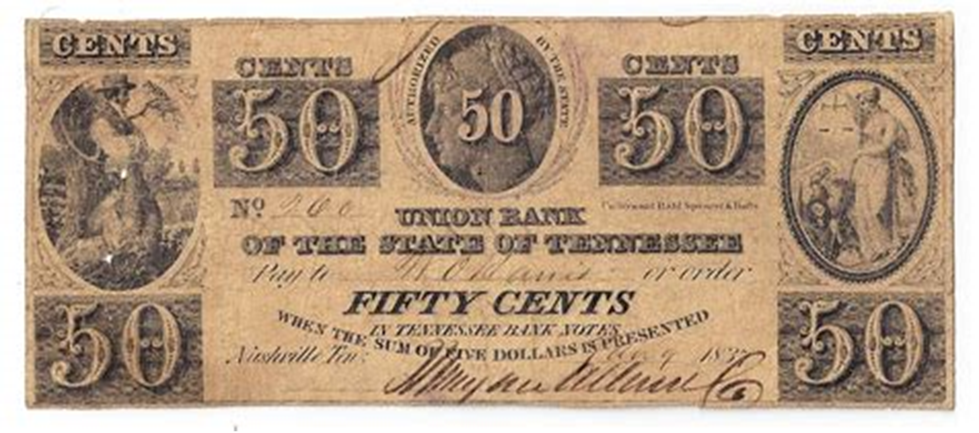

Yet, in spite of the near unanimous belief in real money and its greatly increased supply, metallic currency remained the secondary medium of exchange. Americans lived in an economic world whose retail transactions were almost all exchanges of goods and services for notes printed and issued by banks. Even after the Distribution Act took effect, the Union Bank of Nashville, along with other local banks, found it profitable to continue to issue and exchange bank notes denominated in pennies. By using a two-step exchange for its small change notes, the Union Bank of Nashville and other state-chartered banks could qualify as “good” banks under the terms of the Distribution Act and continue in the retail credit business. The Union Bank of Tennessee in Nashville would issue fifty cent notes in 1837 with the promise that they could be bundled together and become exchangeable for bank notes. Customers simply needed to collect five dollars’ worth of the less than $5 paper, and they could exchange it for a proper demand note.

There are very few surviving records that offer any details about the volume of retail credit business done by the Union Bank of Nashville and other state-chartered banks. We do know that the state-chartered banks in the western half of the U.S. had become sufficiently profitable that, by New Year’s Day 1837, they were net lenders to their eastern counterparts. The booming demand for the purchase of federal land in the states and territories did not entirely end when payments could only be made in specie. Exporters to the United States and their American counterparts had dealt with the requirement of paying only coin since the passage of the Tariff and Collection Acts of 1789. There were the legal and semi-legal workarounds, and the banks in the west and southwest could call their correspondents in the money centers in the East to provide the extra specie needed.

The difficulty for the eastern banks outside of New England was that they did not have enough gold coin to cover both the demands from their “country” correspondents and the political worries of their own depositors that Martin Van Buren’s independent Treasury would swallow up the country’s entire gold reserve. The eastern money center bankers had been suspicious of the ease with which states in the old Northwest and South continued to create credit out of nothing but mutual promises to pay, but they had also been envious. They had joined Nicholas Biddle in following the example set by the Bank of England and restricted their note issues and discounts to already well-established accounts. They found themselves looking back at year after year of defending the Bank of the United States and its policies in favor of “sound” money with only reduced earnings to show for it. Whether “sound” or not, a bank made its money by having its notes in circulation. In 1829 Biddle’s bank alone had in circulation three eighths of the outstanding bank notes in the country; seven years later that amount was virtually unchanged ($15.8 to $16.4 million) and were one tenth of the total in circulation. Unlike the “wildcat” banks in the South and Old Northwest and the Suffolk system banks in New England, the money center banks had drawn back from any opportunities for retail credit. They had left that to the merchants like A. T. Stewart. In the view of their correspondents in England, it would have been scandalous for the Bank of the United States (now chartered as a Pennsylvania state bank) and its respectable colleagues to have issued penny-denominated notes. Having thoroughly missed out on the expansions of the towns in the South and Old Northwest, the mid-Atlantic banks now found themselves dealing with correspondents who wanted redemptions, not further extensions of credit. When they failed to persuade the new president to suspend enforcement of the Specie Circular, the established firms in the Philadelphia and New York suspended their own part in the compliance. In late spring 1837 they stopped all redemptions.

The money center banks would resume in the fall. By then, the fall-off in the demand for public lands had taken hold. In 1836, Federal revenues from the sale of public lands had been $24,877,000; in 1837 they were $6,776,000, with two-thirds of that amount being collected in the first two quarters of the year. The question for the Treasury, which now did business only in coin, was whether it could stay in business. Apparently, it was possible for the country to have enough gold even as the government went bust. Customs collections would decline from $23,410,000 in 1836 to $11,169,000 in 1837. From November 1, 1836, to August 15, 1837, the U.S. Treasury’s specie balances went from $45.06 million to $12.94 million. By year-end, all distributions to the states of its surplus had been suspended. Yet, more than a year into the panic, after the money center banks had suspended and resumed redemption, the country was still a net recipient in the flows of international money. For the fiscal year ending September 30, 1838, the United States would take in $13.2 million more in specie than it would send abroad. Even into the following year there was still a general presumption that the panic had been an unfortunate consequence of the failure of some Americans to accept the sensible rules that went with central banking. Nicholas Biddle had served as president of the Bank of the United States from January 1823 until its charter expired in 1836. He continued as president of the firm after it had been state-chartered as the United States Bank of Pennsylvania. In 1837, before the panic, the bank’s shares had sold at $137. In March 1839 when Biddle resigned as president, they were quoted at $111. By 1843 the bid was 1 7/8.

Stefan Jovanovich manages the portfolio for The NJT Company, Inc., a family office based in Nevada.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All