The Lost Elements of Financial Planning

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Are you missing opportunities to deepen your client relationships or losing business opportunities in your planning process?

Many financial advisors and planners provide a comprehensive experience. However, I see cases where their primary focus is on answering the single question, “Do I have enough?” As we know, this generally means whether one can support their lifestyle until they die in a reasonable form with their financial resources. “Enough” is a separate discussion. This article is about the need to discuss the “what ifs” before they become “what nows.”

Often, the answer refers to a household situation where there is a couple in their 50s, 60s, or 70s and we are mapping their anticipated financial needs assuming conditions as they exist today:

- A couple;

- Reasonable health; and

- Good knowledge of their inflows and outflows.

But there are at least six “what ifs” that need to be part of the planning conversation before they become “what nows.” Asset-Map calls them “the six L’s” that summarize the events that commonly change the course of financial well-being:

- Liquidity needs

- Long-term disability events

- Loss of life

- Long-term care events

- Longevity (long-term cash flows)

- Legal/liability

Your financial planning process must include initial and on-going conversations with clients to discover their plans and approaches to dealing with significant events that are tied to their well-being.

You need to help clients answer the question, “What is your household plan in the event of ______?” That is the “what ifs” before they become “what nows.”

For example, the purpose of having funds available for emergency needs is to avoid having to take more costly options like selling securities when markets are down or borrowing money. While having even $100,000 cash on hand (in a bank) will not produce significant interest, having to sell securities to cover short-term needs or borrow funds can be more costly.

Much of the material in this article is based on what I have learned by attending Asset-Map’s boot camp, developing maps, and reading some of the vast amount of support material available in the firm’s support library in addition to discussions with their staff. The information about the 6Ls is supported by other material including:

- Worksheets

- Fact finders

- Templates

- Target maps to support the 6 Ls:

- Long-term disability events

- Loss of life events

- Long-term care needs

- Liquidity needs and longevity needs are essentially addressed by a retirement funding target map

- Education funding target maps are also supported in addition to any number of custom maps

- Preference selections to customize your “target maps”

Let’s first define “target maps”:

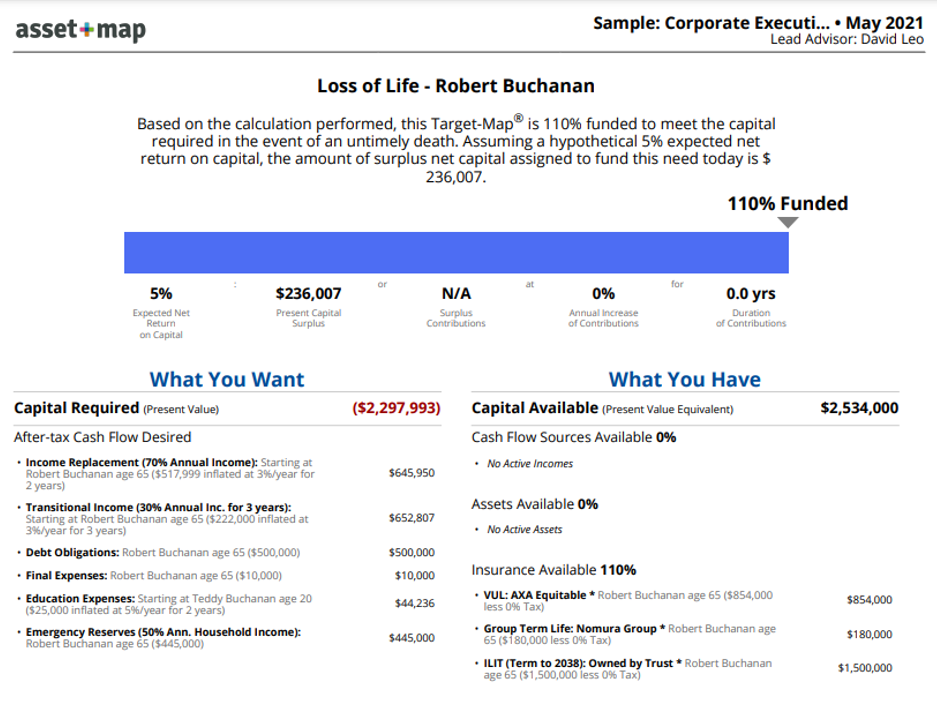

You can see this is a sample for report for Robert Buchanan, a hypothetical corporate executive. The report indicates:

- What the client wants – The amount of capital required to support his surviving spouse until her demise when Robert dies based on the anticipated after-tax cash flow desired which is a function of:

-

- The income that will be needed

- Pay off his debts

- Pay his final expenses

- Keep his education funding commitments

- Provide emergency reserve funds

- What the client has – The amount of:

-

- Anticipated cash flow after death

- Assets available

- Insurance available

- What It means – As the report indicates, the loss of Robert’s life shows, “Based on the calculation performed, this Target-Map® is 110% funded to meet the capital required in the event of an untimely death. Assuming a hypothetical 5% expected net return on capital, the amount of surplus net capital assigned to fund this need today is $236,007.”

Good news, though not for Robert, other than that he is hopefully pleased his wishes for his spouse’s financial well-being will be met.

Target-Map templates can quickly create funding goals by providing you with pre-set capital requirements for loss of life, retirement, and others. (Capital requirements in Target-Maps are called "What you Want").

You can also make your own custom Target-Map to define capital requirements. In effect, you define "what you want" and apply "what you have" working together with the client. One of the benefits of Asset-Map is that it creates many opportunities for conversation so you can deepen your client relationships as well as helping ensure your client’s planning process is truly comprehensive.

Let’s review the 6Ls:

- Liquidity needs

Determine your client’s liquidity needs by comparing two analyses. Traditionally, the emotional comfort number (B) for how much liquidity a household needs will “override” the planner recommendation to have a multiple of monthly expenses (A).

Calculation A

- Estimate the household monthly expenses

- Multiply monthly expenses amount by the determined number of months as desired by the client appropriate.

- The suggested monthly multiplier is 3-6 months. Personally, I prefer 12 months of liquidity for primary expenses of food, shelter, healthcare, and utilities.

Calculation B

- Enter the comfort liquidity reserve amount. In other words, enter the amount that the clients believe they would need or want to have available for liquidity to “sleep at night”.

The Household target liquidity amount is the greater of the two numbers.

Conservative individuals may even keep 12 months expenses in short term, highly liquid assets including bank deposits.

- Long-term disability

Determine your client’s LTD needs analysis by considering monthly and one-time capital expenses incurred if a household member loses their income. Several examples are included to remind the family that these events do not exclusively deal with income loss. Oftentimes additional loss of retirement plan matches, benefits, Social Security accruals and additional medical living expenses can be involved.

Monthly expenses will include items such as living expenses, lost retirement savings, business expenses, and catastrophic events.

Capital expenses can include items such as education funding, home modifications, and emergency reserves.

As disability insurance has many considerations, costs, benefits, term, and other factors, it’s a subject that should be discussed with clients in detail.

The article, “How Much Does Disability Insurance Cost Per Month?” states, “The cost of disability insurance depends on a number of personal factors, such as health history and job occupation, and policy choices, such as benefit amount and waiting period. The average cost of disability insurance is typically between 1 percent and 4 percent of your annual income. Another rule of thumb is that you should expect to pay between 2 percent and 6 percent of your policy’s monthly benefit amount in premium. Of course, you may pay more or less than these ranges depending on personal factors, job occupation, and policy choices.

Long-term disability is an important – but often overlooked – employee benefit. Most workers don’t think they’ll ever become disabled and need income replacement. Unfortunately, more than one in four 20-year-olds will become disabled before they reach retirement.

Long-term disability insurance picks up where short-term disability leaves off, typically after three to six months. It usually pays 50-60% of an employee’s salary until he or she can return to work. In some cases, long-term disability will pay an employee up to retirement.

- Loss of life

Determine the individuals in the household’s survivorship needs analysis by considering how the loss of that person would impact debt repayment, capital expenses, and income replacement.

Debt repayment includes debt amounts owed by the deceased household entity. This will include items such as mortgage, credit card debt, and loans.

Capital expenses will include such items as final expenses, education funding, and emergency reserves. Some households will also include minimum legacy goals and charitable bequests.

Income replacement includes amounts determined to cover the loss of previous Lifetime Income of the deceased and/or transitional income. The Target-Map assumes a gross income replacement (pre-tax).

- Long-term care

Determine a household member’s long-term care needs by considering daily expenses needed and capital expenses. Traditionally it is recommended that households approximate a reasonable or average event duration (in years), and daily expense for care in a facility or home.

Daily expenses will include items such as facility expenses and/or in-home care costs.

Capital expenses will include items such as home modifications, caregiver training, and care coordination.

Genworth has a “cost of care survey” where you can calculate the cost of care in your area. At the My Life site, it states, “the odds of needing assisted living…(is) somewhere between 50-70% of people over the age of 65 will require fairly significant long-term care services at some point in their life. They further report, “the average length of stay for residents in an assisted living facility is about 28 months.”

Given the monthly median costs nationally (2020) for an assisted living facility of $4,300 and 28 months, the total costs would be $120,400.

For a nursing home – semi-private room, monthly median costs: national (2020) are $7,756. With a 28-month length of stay, total costs would be $217,168.

I looked up Portland, Maine and found there are five cities named Portland in our country, Maine, Oregon, Connecticut, Pennsylvania, and Tennessee. I averaged the cost multiplied by 28 and found total costs for assisted living facility and nursing home – semi-private room,” respectively at $143,315 and $296,677. These are obviously higher than the national averages. I also looked at total costs for assisted living facility and nursing home – semi-private room,” for the five largest cities in the U.S. (NYC, LA, Chicago, Houston, and Phoenix) and found respectively they were $136,590 and $239,574.

- Longevity

Determine the future cash-flow projections for client-specific situations that will include retirement cash-flows, education funding, and any other custom future expense impacted by growth, tax and/or inflation rate.

Custom expenses should be included to fit the specific, future needs of households. Amounts and durations should be included as well. i.e., $25,000 until age 65 or$25,000 until year 2022.

Annual expenses (after-tax) include such items as living, medical, and travel expenses as well as education funding.

Capital expenses will include items such as education funding, home modifications, and emergency reserves.

- Legal/Liability

There are many legal and liability checklists such as the that for purchasers of professional liability insurance on the ABA website that can assist you to indicate important legal documents completed and situations that can affect a household’s financial plans. These can include whether the household has implemented wills, trusts, and business agreements, has special needs members, and/or is concerned about asset-protection.

Elements 1-5 of the six Ls can be used to create visual Target-Maps in the Asset-Map® platform. Enter the needs and expenses as well as the financial elements available into the household’s appropriate Target-Map to help them determine their current funding level towards meeting their specific goals.

Summary

The key to client relationships, engagement, client loyalty or advocacy all revolve around communications. Discussion of the 6 Ls with your clients will give you many opportunities repeatedly to have meaningful communications with them. I am often asked, ”What is there to talk about in our check-in calls?” Of course, there are many topics of inquiry into the general well-being of your client and her family, both nuclear and extended. There are always things happening in their lives every month or two at most.

You always listen for client wisdom, e.g., changes in personal lives, preferences, sports, hobbies, as well as their fears, concerns, what makes them happy, etc. There are vacation and holiday plans and/or recent experiences. There are children in schools perhaps. What would you talk to your friends about? And there’s always the markets, economy, and portfolios and the need for actions or inactions.

Now you have six more areas of great importance to check in on. With your best clients there should be no question as to what to talk about. And adding depth to the next tiers of clients and improving those relationships over time can create some exciting possibilities by having enriched conversations, whether a 10-minute quarterly call or a 90-minute strategic alignment meeting with a top client.

David Leo is founder of Street Smart Research Group LLC. He is an author, speaker, coach, consultant, and trainer to financial professionals. David is an experienced business manager who works solely with Financial Advisors, Planners and firms who want to organize, structure & grow their businesses by attracting, servicing, and retaining affluent clients.

If you have questions or would like assistance in personalizing and implementing approaches from The Financial Advisor’s Success Manual, schedule a free 45 Minute Strategy Session at https://calendly.com/davidileo or contact me at [email protected] or visit my website at www.CoachDavidLeo.com

My book is available at Amazon at https://www.amazon.com/Financial-Advisors-Success-Manual-Structure/dp/0814439136.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All