Five Tax Planning Strategies for the Ultra-Wealthy

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Investing is simple, but taxes and estate planning are not. With the many tax proposals pending, they will get less simple. Though those proposals don’t have much impact on the merely wealthy, with say a $10 million net worth and income below $1 million, some changes would have huge consequences for the very wealthy.

Investing is simple, but taxes and estate planning are not. With the many tax proposals pending, they will get less simple. Though those proposals don’t have much impact on the merely wealthy, with say a $10 million net worth and income below $1 million, some changes would have huge consequences for the very wealthy.

A few of the major proposed changes are:

1. Increase ordinary income tax rates to 39.6%.

2. Long-term capital gains (LTCG) tax rates to be set to ordinary income rates for those with over $1 million income, possibly retroactively.

3. Elimination of the step-up basis on inherited assets for over $1 million per person.

4. Lowering the estate and gift tax exemptions to $3.5 million and $1 million, respectively, from the current $11.7 million per person, with potential corresponding rate increases.

5. Eliminating grantor trust benefits and/or forcing income tax recognition on certain events or at certain intervals (e.g., assets transferred by gift and at death will be deemed sales).

Typically, a client with a taxable estate comes to me with some tax planning vehicles like grantor trusts or family limited partnerships, but those vary wildly. To illustrate planning strategies and associated pitfalls, I created a case-study of an aggregate of many wealthy clients. In this example, however, the client hasn’t yet created those estate planning vehicles.

Case study example

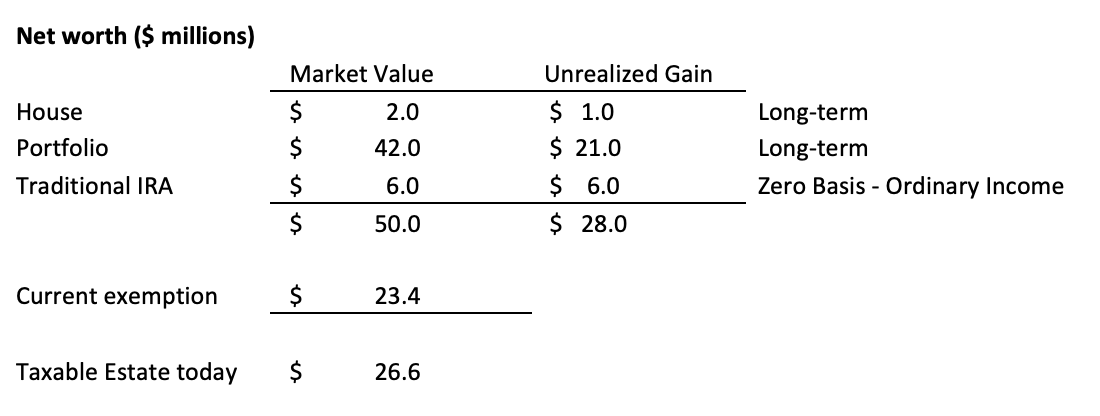

Consider a married couple with three children both age 65 and in reasonable health. They have a $50 million net worth and live below their means needing about $200,000 a year. They have no debt and their balance sheet is as follows:

Under the current laws, their taxable estate would be about $26.6 million, subject to federal estate tax at a 40% tax rate. In addition, some states have estate taxes. Also under current law, beginning January 1, 2026, the current exemption, which rises with inflation until then, will be cut in half. In today’s dollars, the $23.4 million exemption (for a couple) would be cut by $11.7 million.

Because they are relatively young, let’s assume the husband and wife live until at least 2026. At their current net worth, they would have the following consequences at the second-to-die of the husband and wife:

- IRA going to the kids after the death of both spouses which must be withdrawn over 10 years at ordinary income tax rates.

- A taxable estate of $38.3 million with a 40% estate tax or $15.3 million due.

- A full step-up basis on the $22 million of long-term gains.

While it’s an unlikely scenario, if all of these five proposals were enacted, upon death, the couple’s estate would owe about $24.9 million between the lower estate tax exemption and the previously unrealized gains above $2 million, which will be taxed as ordinary income. That takes an additional $9.7 million from the estate with half of their net worth going to taxes.

To make matters worse, the couple’s children would have to pay ordinary income taxes on the $6 million inherited IRA. And, before their death, the couple could be paying an ordinary income tax rate on long-term capital gains, depending upon both their income and how much gain they recognize each year.

Like most financial planners, I’m not licensed to practice law, so I work with my clients’ estate planning attorneys in developing strategies. For this case, I turned to Sarah Robinson, a partner specializing in estate and wealth transfer planning with the international law firm of McDermott Will & Emery. We discussed potential strategies and pitfalls.

Robinson agreed that it’s very difficult to predict what Congress will do, and that it is very unlikely that all of the proposed changes will be enacted. She did state it’s unlikely that any increase in the long-term capital gains rate will be enacted on a retroactive basis (despite Biden’s current proposal), due to the logistical challenges related to the IRS’s enforcement of a mid-year change. She expects that eliminating the unlimited step-up in basis will also face considerable opposition in Congress – it too has logistical challenges, as it is nearly impossible to determine the cost basis for assets acquired decades earlier, and many congressional members are wealthy and want their assets to pass on with a stepped-up basis.

She also noted that the younger the couple, the more flexible the estate plan should be. The possible moves to be discussed for this 65-year-old couple would be very different for a 40- or 90-year-old couple.

Here are some strategies – they are not mutually exclusive, and several can be enacted simultaneously.

Strategy 1: Intentionally defective grantor trust

Since the couple has adequate resources beyond their life expectancy, Robinson’s first suggestion was to create an intentionally defective grantor trust for $23.4 million to use up the full current exemption of $11.7 million each. If the couple did not want to give that much away, then one of them should use up their full exemption. Robinson advised against splitting the exemption because the lower exemption would apply to both.

The defect in the grantor trust allows the husband or wife (whoever creates the trust) to continue to pay the income taxes on those assets in the trust, which essentially allows for more tax-free gifting since the trust or the beneficiaries (the children) aren’t paying the taxes. The trust assets and the assets used to pay income taxes are out of the client’s estate. In general, one would use assets with a lower unrealized gain, since the step-up in basis is not available for irrevocable trusts like these. If done properly, the client could always swap assets between the couple’s personal holdings and that of the trust to optimize income tax planning.

Strategy 2: Discounting through a family limited partnership

The couple could create a family limited partnership and contribute, for example, $10 million in assets to it. If the partnership has a valid purpose and if certain formalities related to the partnership are respected, this allows the assets in the partnership to be discounted. For example, discounting the partnership by 30% would lower the couples’ estate by $3 million. If the couple were comfortable giving away a bit more, they could eventually gift a minority interest to the children, i.e., 10%, at a discounted value. Yet the couple could own 90% of the partnership so they still have the use of the majority of the partnership’s assets.

Strategy 3: Grantor retained annuity trust (GRAT)

With this strategy, the husband or wife creates a trust that pays them an annuity. An example would be that the client funds $2 million in a GRAT, which pays them approximately $400,000 a year for five years. They fund it with assets most likely to have higher appreciation such as high-growth stocks. Any gain above 120% of the applicable federal midterm rate (1.02% for June 2021) would go to the beneficiaries. If the portfolio gains 10% a year, the additional 8.8% (10% less 1.2%) appreciation passes through to the children transfer tax-free at the end of the five-year term. If the stock goes down in value, the couple is no worse off.

Strategy 4: Convert the IRA to a Roth

As mentioned, the $6 million in the IRA is problematic, even with no tax law changes. The estate would be taxed 40% based on the full $6 million and then the children would have to pay ordinary income tax on the full amount over the next 10 years. If the clients’ marginal tax rate (federal and state) were at 45%, this $6 million is only worth $3.3 million as the other $2.7 million belongs to the federal and state governments.

If they converted to a Roth, it solves two problems. It lowers the estate by $2.7 million, thus saving $1.08 million in estate taxes. The money passes on to the children in a far more valuable vehicle where they can let it grow for 10 years tax-free. Converting now would be beneficial if marginal rates on ordinary income later increase.

An alternative to this strategy is to have the IRA assets go to charity if the clients or their children have a charitable intent), which enables the IRA assets to escape both estate tax and income tax.

Strategy 5 – Tax-gain harvesting

The goal here is to recognize long-term capital gains at a 23.8% rate sooner than a 43.4% later. This could backfire if the tax increase is enacted retroactively (unlikely), the higher long-term capital gains tax is never enacted, or the unlimited step-up in basis remains intact. Robinson recommended caution with this approach, though she noted if one were planning on recognizing the gain soon irrespective of these proposed changes, now might be a good time to do so.

Summing it up

Robinson succinctly described the complexities involved in estate planning for the ultra-wealthy. She said that not only must one predict what tax laws will change soon, one must speculate on what laws will change years or decades later. In addition, we don’t know whether the assets will appreciate wildly or plunge. Every strategy can backfire, which is why Robinson generally recommends keeping estate planning more flexible for younger people.

As far as when to act, Robinson stated we may have more clarity as the year goes on. Unfortunately, every estate planning attorney is likely to be swamped by the fourth quarter, reacting to the new laws. She recommended a couple of strategies:

- Talk to the client’s estate planning attorney now to plan for these scenarios, including creating trusts or family limited partnerships, but waiting until later in the year to fund.

- Make a gift now using a method that allows for mitigation of tax in the event of tax reform, such as funding a trust with disclaimer provisions, such that if assets are disclaimed, they revert to the donor, effectively undoing the gift.

I’ve only given high level summaries of these strategies. The complexities are far greater than I’ve described. A far more detailed description of some of these strategies can be found in this McDermott Will & Emery presentation. It includes some of those “free look” strategies.

I have not considered the implications of a “wealth tax,” such as that proposed by Elizabeth Warren (D-MA) and Bernie Sanders (I-VT). That adds further complexities for those with wealth greater than $50 million.

Taxes and estate planning for the ultra-wealthy are complex. A financial planner’s role is to work with their client’s estate planning attorney and CPA to develop the right strategy for them. With the sands of tax law shifting once again, now is a good time to discuss these strategies with your clients’ teams.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies and has consulted with many others while at McKinsey & Company.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All