A Short History of Value Investing and its Implications

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

I would like to thank Andrew Cornell, Shaun Cornell, Aswath Damodaran, Richard Gerger, and Ivo Welch for helpful comments on earlier drafts of this paper.

Abstract

This paper argues that what came to be called value investing was an historical accident. It arose in large part because the influential work of Graham and Dodd preceded the development of electronic spreadsheets leading them to propose short-cut estimates of value based on accounting ratios. The demise of the value premium in the last 12 years has led to doubts regarding the efficacy of this approach to value investing and efforts to adjust the accounting ratios to make them more robust. The argument here is that these efforts are misguided. Instead, it must be recognized that value investing amounts to comparing estimates of fundamental value with price and that accounting ratios, however tweaked, are not a reasonable way to estimate value – it requires a full blown DCF analysis. The paper then goes on to address some of the implications of that assertion.

Introduction

It is the spring of 1978 and Harvard Business School student Dan Bricklin has a problem. He is sitting through yet another case discussion that requires him to produce a detailed financial forecast in the form a large matrix of rows and columns. The problem is that each time he changes one of the entries, it ripples through the entire matrix which he must recalculate with his handheld calculator. The work is incredibly tedious and time consuming. Bricklin thinks to himself, wouldn’t it be wonderful if the spreadsheet were electronic? Each cell could be a number, a label, or a formula relating cells to each other. As soon as any cell is changed the entire matrix would be recalculated instantly.

Following up on his idea, Bricklin joined with Bob Frankston to found Visicorp. The company’s first product, Visicalc, was the world’s first electronic spreadsheet which ran on the newly introduced Apple II computer. The product was an immense success. It was the first blockbuster software sensation of the personal computer revolution and was a big reason for the booming sales of the Apple II.

Unfortunately for Visicorp, the company’s interest turned to integrated software and away from improving Visicalc and porting it to the upcoming IBM-PC. When the IBM-PC was introduced in 1981, Mitch Kapor was ready to pounce with a new spreadsheet product called 1-2-3. 1-2-3 became a huge hit. So much so that it was rumored that Bill Gates made on offer to merge Microsoft with Kapor’s company, Lotus Development, on an equal basis. When Kapor rejected the offer, Gates threw the power of Microsoft behind a new product called Excel. To this day, Microsoft Excel remains the dominant spreadsheet software. Excel is remarkably powerful when combined with a modern PC. It can link numerous spreadsheets each with millions of cells. Creating a sophisticated valuation model with multiple scenarios is now a standard exercise for students of finance.

Roll back the clock further to the early 1930s. Benjamin Graham and David Dodd are at work on what will become their classic book, Security Analysis (1934). They have the idea that what are called “value stocks,” stocks of companies that offer generous payouts relative to their price, are likely to be superior investments. The problem they face is determining what is meant by a value stock. If Dan Bricklin’s invention had been available to them, the answer would have been simple. Graham and Dodd might well have conducted what came to be called a discounted cash flow, DCF, analysis which requires forecasting the future cash payouts available to investors (free cash flow) and computing their present value using a reasonable discount rate. The DCF model takes account of all future expectations, not just recent earnings, or book value. As a result, the present value is the best estimate of the fundamental value that an investor receives when buying a stock. That value can then be compared to the price of stock when making an investment decision.

Unfortunately for Graham and Dodd, Dan Bricklin’s idea was still decades away. For them constructing DCF models by hand would have been a huge undertaking. More importantly, it would be nearly impossible to stress test the models by running different scenarios with changed assumptions. Each time an assumption was changed the entire model would have to be recalculated by hand. At that juncture even handheld calculators were not available.

It is no surprise that to assess “value” Graham and Dodd turned to simpler metrics that could be calculated and compared quickly. Measures like price/earnings and price/book, which bore some relation to price/value, were easy to compute and compare across companies. In a follow up book, The Intelligent Investor, Graham (1949) elaborated on ten screens for selecting value stocks.[1] They included items like Price < Two-thirds of Tangible Book Value and Debt < Twice Net Current Assets. Once again, the focus was on using accounting data and ratios to identify stocks whose value exceed the price. The influence of Graham and Dodd was widespread. As a result of their influence, value stocks became synonymous with companies that had low ratios of measures such as price/earnings and price/book.

To further promote the spread of value investing, two other innovations, one academic and one practical, were required. The academic innovation was the influential work Basu (1977). Basu published the first modern empirical study of the value effect. In his paper, value was measured by price-earnings (P/E) ratios. Basu found that value stocks, that is those with low P/E ratios, earned superior returns even after adjusting for risk using the CAPM. Basu’s work set off an avalanche of academic studies related the value effect, the most widely noted being the three-factor asset pricing model developed by Fama and French (1992). One of the three factors was a portfolio based on the value which Fama and French measured by the ratio of price to book rather than price to earnings as Basu had done.

The practical innovation was the rise of Warren Buffett, who was on his way to being universally hailed as the world’s greatest investor. Buffett was a student of Ben Graham’s and an advocate for his methods. In his now famous shareholder letters Buffett lauded both Graham and value investing. By the time Basu’s article was published Buffett’s investment success was beginning to be recognized. Over the succeeding decades, it grew to the point where he became an icon.

The result of these two innovations was a dramatic rise in the interest in value investing. In most all of the academic work and practical applications value stocks continued to be defined by valuation ratios similar to those proposed by Graham and Dodd. Although more sophisticated ratios were developed, such as Shiller CAPE ratio, and tweaked versions of price/book and price/earnings ratios that took account of the rising importance of intangible assets, the basic valuation ratio approach remained intact.

Now roll the clock forward to 2007. By that time, Mr. Buffett had become a legend, but advances in computing, data storage, and data transmission were dramatically altering the investment landscape. The data necessary to screen stocks according to valuation ratios such as price/earnings and price/stocks was widely available online. Firms such as Charles Schwab were providing automated screeners free of charge to retail investors. More elaborate data services allowed computation of sophisticated ratios that include possible accounting adjustments. Those services were also making available statistical models that could be used to construct combinations of the ratios. In this environment, it stretches credulity to think that such information could serve as the basis of a superior investment strategy. It also raises a more fundamental question – if the goal of value investing is to compare price with the best estimate of intrinsic value why rely on such ratios in the first place? Furthermore, why is growth an alternative to value? From the standpoint of the comparison of intrinsic value with price, stocks of rapidly growing companies are as likely to be “value” stocks as those of more mature, slowly growing companies. Given his background, Ben Graham tended to associate value with mature companies that had predictable cash flows, but this was a decision he made, in part due to of his experience with bond investing, it is not a prerequisite for value investing. There is no a priori reason why mature, slowly growing companies should have greater intrinsic value, relative to price, than more rapidly growing companies. It depends on a comparison of discounted present value of expected futures cash flows with price. Defining value stocks in terms of DCF estimates of fundamental value also eliminates the need to attempt to adjust accounting numbers for things like intangibles. Because valuation is based on expectations of future cash flows, not accounting numbers, there is no need for additional adjustments.

But there is a hiccup. Estimating fundamental value using discounted cash flow analysis requires at least five years, and in many cases ten years, of cash flow projections as well as an estimate of the terminal value. Attempting to forecast all those numbers, compared with computing ratios based on current data, is often criticized as speculative. But such projections, and the associated need to understand the business in order to make them, is required to meaningfully estimate intrinsic value. The fact that it is difficult to achieve sufficient understanding of a business to forecast its financial outlook is exactly why it is challenging to be a value investor. [2] However, the difficulty should not be interpreted to imply that future projections should be cast aside in favor of using ratios based on current data. It is hard to see how ignoring the long-run projections necessary to value a business properly, and instead relying on incomplete current data on the grounds that it is less speculative, could be the basis for a value investing strategy.

The fact that DCF valuations are based on projections makes them idiosyncratic in two senses. First, the projections are investor specific. One investor may have an optimistic projection regarding Apple’s future cash flow and conclude on that basis Apple is a value stock. Another more pessimistic investor is likely to reach the opposite conclusion. This makes it virtually impossible to design systematic tests of value investing, because the definition of what is a value stock is investor dependent.

Second, the ability of an investor to accurately assess value is likely to be company specific. To illustrate, suppose an investor holds both Apple and Facebook on the grounds that they are value stocks given the investor’s projections. It may be that the investor has an in depth understanding of Apple that can be used to earn superior risk adjusted returns, but, unknown to the investor, he or she has little knowledge regarding Facebook that is not already incorporated in the market price.

The foregoing idiosyncrasies make testing “value investing” a non sequitur because unlike the situation in which accounting ratios are used to define what is meant by a value stock, with the DCF definition the identification of a value stock depends on the investor. All that can be tested, therefore, is the value investor’s information and understanding regarding the business outlook, on average, for the companies in his or her portfolio. That may be an interesting question to ask in the case of someone like Mr. Buffett, but it is not a test of value investing per se. It is a test of whether Mr. Buffett’s assessments of future cash flow are more accurate, on average for the stocks of the companies in which he invested, than the expectations impounded in the market price at the time he made the investment.

The investor specific and company specific nature of investing based on DCF estimates of intrinsic value also means that it is extraordinarily difficult to reduce value investing to algorithms. This does not mean that algorithms cannot be written to forecast future cash flows and compute present values for a large sample of businesses, websites like Finbox.io do exactly that. But Finbox basically plugs in projections from analysts and other public sources to compute the DCF values. It is hard to call that value investing unless Finbox incorporates new information or insights into the cash flow forecasts.

Traditional value investing: The track record

To sum up this far, the claim here is that what came to be called value investing was an historical accident, the result of the fact the Graham and Dodd, among others, did not have access to Bricklin’s technology and were forced to use shortcuts to assess value. That does not mean that value investing as traditionally defined cannot work. Whether it does so is an empirical question and one that has attracted a vast amount of academic attention since Basu’s original study. It is also one that has produced an ongoing debate. The debate arose because prior to 2007 most research studies found statistically significant evidence of a value premium. For instance, Dimson, Marsh and Staunton (2020), in their comprehensive annual update on global market returns, note that the value premium (the premium earned by low price to book stocks, relative to the market) has been positive in 16 of the 24 countries that have returns for more than a century and amounted to an annual excess return of 1.8%, on a global basis. The debate focused on the question of whether that premium was evidence of mispricing or an indication that asset pricing models needed to be adjusted to account for theretofore unappreciated risks. Though the literature addressing the debate is vast, the most noted papers were Fama and French (1992) who argued that the value premium reflected a risk premium and Lakonishok, Shleifer, and Vishny (1994) who claimed it was evidence of behavioral based mispricing.

The debate over the source of the value premium has been muted by the fact that beginning in 2007 the premium disappeared. The extent of value’s demise depends on how it is measured, though all measures produce the same general picture. One common metric is the return on the HML (high book to market minus low book to market) portfolio originally constructed by Fama and French (1992) and regularly updated by Prof. French on his website. Exhibit 1 plots the path of wealth (POW) derived from the HML portfolio returns from January 1963 through December 2020. Except for a dip during the dot.com bubble, it shows the inexorable rise in the POW resulting from a continuing value premium until about 2007. At that point, a volatile decline begins, and the POW drops to less than half of its 2007 maximum.

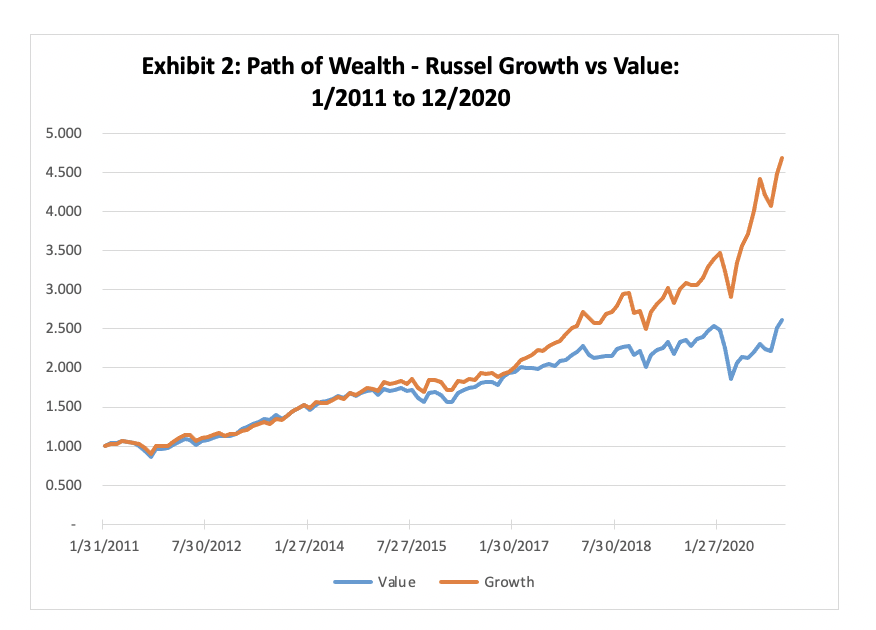

Another useful way to depict the demise of the value premium is to compare the performance of value focused portfolios with growth portfolios. As one example, Exhibit 2 plots the path of wealth for IWD, the ETF tracking the Russell value index, and IWF, the EFT tracking the Russell growth index, over the period from January 2011 through December 2020. Interestingly, the two POWs track each other closely through mid-2014. At that point, a gap starts to emerge and grows at an acerating rate, particularly in 2020.

Exhibit 2 confirms the underperformance of traditional value stocks relative to growth stocks, but it also demonstrates that the demise of the value effect is not absolute. The compound rate of return on the value index over the full period is 10.15%. At the beginning of the period, the 10-year Treasury rate was about 3.5%. Adding an equity risk premium of 5.5% gives a ballpark estimate of 9% for a fair expected rate of return. On that basis, an investor told at the start that he or she would earn a compound rate of return of 10.15% over the next decade on the value portfolio would have been delighted. The return only looks anemic when compared against the 16.85% compound return provided by the growth portfolio.

The new definition of a value stock and its Implications

The demise of the value premium beginning in 2007 sparked a new round of research searching for explanations. Current papers that examine the investment performance of value versus growth, such as Arnott, Harvey, Kalesnik, and Linnainmaa, (2020) Asness, Frazzini, Israel, and Moskowitz (2015) and Israel, Laursen, and Richardson (2020), all use the traditional valuation ratios to define value and growth stocks. These, and many other papers the authors reference, document the fact that since 2007 growth stocks, particularly the stocks of large technology companies such as the FAANGs have dramatically outperformed traditionally defined value stocks.

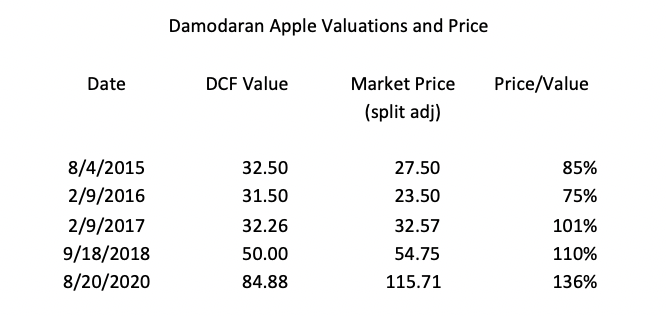

Of course, the foregoing conclusion depends on the definition of a value stock. If a value stock is defined by the ratio of fundamental DCF value to current market price, then some of the FAANGs may well have been value stocks, at least at times during the last twelve years. As a specific example, consider the case of Apple. In his blog, Professor Aswath Damodaran posted five fundamental DCF valuations of Apple which are reproduced in Exhibit 3. Of course, these valuations reflect Prof. Damodaran’s personal forecasts for Apple’s future cash flows. The exhibit shows that early on Apple was a value stock in Prof. Damodaran’s opinion (he ascribes to the DCF definition of a value stock), then later it was fairly valued, and finally it lost its “value” status in his view. That does not mean it became a growth stock – it was just no longer a value stock. To reiterate, using the DCF criterion there is not a distinction between value and growth, both slow growing and rapidly growing companies can be value stocks.

Damodaran Apple Valuations and Price

Although the DCF approach to value does not differentiate between value and growth stocks in the traditional sense, it is possible to distinguish between sources of value. Using the residual earnings version of the DCF valuation model developed by Olson (1995) and Penman (2010), the total estimated value can be divided into two parts: the first commonly referred to as assets in place and second as growth options. The exact breakdown between the two components depends on how the model is used to make the division.

Israel, Laursen, and Richardson (2020) propose a simple procedure for calculating the breakdown, adopted here, that limits the forecasting horizon to next two fiscal years. This approach divides the DCF value of the firm into two components. The first component, here called the “current observables,” equals the book value per share, B, plus the present value of forecasts of residual income, X𝑡+1−𝑟𝐵𝑡, during the next two years. The second component, long-term speculative portion of value, equals the market price of the security less the value of the current observables. More precisely the division is given by the equation:

In equation (1), the first term, the book value, is observable from the current balance sheet. The second term, the forecast residual income in year one, is discounted back one year at the cost of equity capital, r. The third term, the forecast residual income in year two, is also discounted back one year, but in perpetuity. The discount factor is not the standard r-g Gordon constant-growth model variety. Israel, Laursen, and Richardson make this choice because they argue that growth is mean reverting and they do not want the near-term forecasts corrupted by overly optimistic (or pessimistic) views of longer-term growth. The value of the speculative component, labelled Spec in equation (1) is then equal to the market price of the stock minus the sum of the first three terms (the current observables).

The distinction between currently observable value and long-term speculative value is related to the traditional distinction between value and growth stocks, but it is not the same thing. Rather than relying on accounting ratios, it is based on a division of the DCF value of the firm. In that sense, it is consistent with the definition of a value stock proposed here in that companies with high speculative values could still be value companies, depending on the investor’s projections. Using the breakdown given by equation (1), it is possible to investigate whether the cross-section of observed stock returns is related to the fraction of value accounted for by the speculative component.

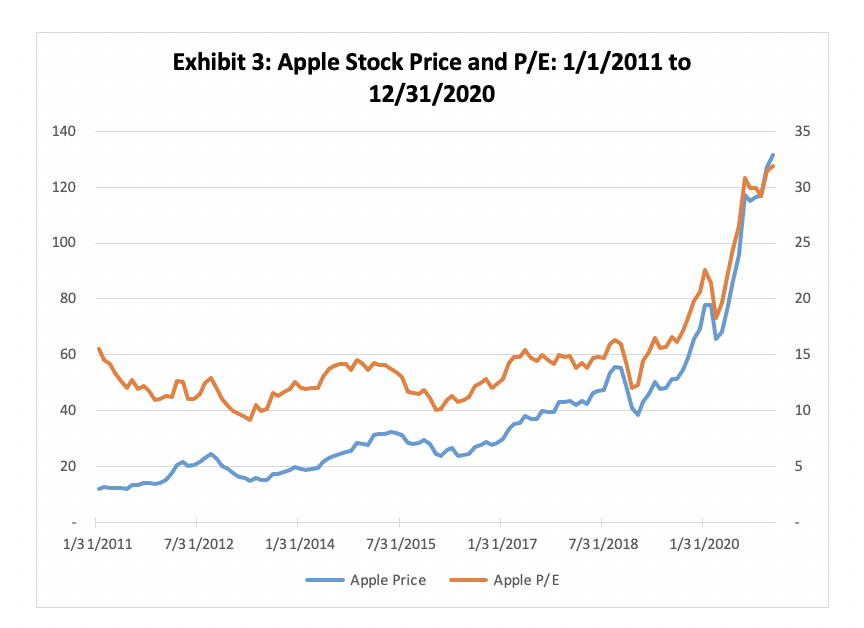

To provide some preliminary and suggestive data. Exhibit 4 plots both the split adjusted Apple stock price and the P/E ratio from January 2011 through December 2020. The first thing to note is the mean reverting nature of the P/E ratio is up through mid-2019. Although there is some volatility, the P/E bounces around its average of 14. As a result, the upward trend in the stock price reflects the growth in Apple’s earnings.

That all changed in early 2019 when the stock began a meteoritic rise, that saw it increase by 340% between January 2019 and December 2020. As Exhibit 4 shows, that increase was driven almost entirely by expansion of the P/E ratio. In terms of the valuation breakdown, this implies that almost all the increase was due to expansion of the speculative term in comparison to the near-term observables. It is interesting to note that one would have expected the relative speculative component of value to have been larger for Apple back in 2015 when the iPhone was less mature, but the reverse is true.

To provide a more formal test of the relation between the fraction of speculative value and subsequent stock price performance, the following procedure was employed.

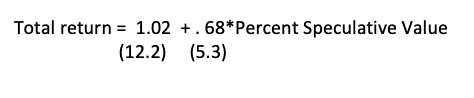

As a first, step the breakdown into current observable value and speculative value was calculated for a sample of companies with market capitalization in excess of $25 billion as of March 5, 2020. Large cap companies were chosen because they have better analyst forecast data available and because using them eliminates small cap outliers that could artificially drive the results. In the second step, the total return on each stock over the period from March 5, 2020 through December 31, 2020 was regressed on the fraction of the March 5 value accounted for the by speculative component. The regressions results, with the t-statistics in parentheses were:

The results show that those companies that had a greater fraction of speculative value at the start experienced a much greater appreciation as the market rose between March and the end of the year.

As an example of how far things have moved in the direction attaching value to the long-term speculative component, Goldman Sachs recently introduced a Non-profitable Technology Index. Not surprisingly, most of the companies in the index had a speculative component close to or exceeding 100% of the market capitalization. Exhibit 5 presents a snapshot of the index. In 2020, its performance was spectacular with the index rising about 400%.

The results are another nail in the coffin of what has come to be called “short-termism.” As summarized by Bebchuk (2012), the major premise of short-termism is that markets systematically under value long-term investments, which are consequently not fully reflected in stock prices. The rising fraction of value accounted for by the long-term speculative component of value indicates just reverse is true. In fact, the proportion of value attributed to the long-term speculative component is currently so large that it gives one pause.

In terms of the analysis presented here the best way to understand these results is not by saying they represent the demise of value. As was stressed earlier, in the context of a DCF analysis a stock with a large speculative value can still be a “value stock.” The remarkable thing about the recent performance of the stock market is the increasing value that has been attributed to the long-term speculative component.

Conclusion

This paper has argued that what came to be called value investing was an historical accident. It arose due to a combination of the three factors. The first was the fact that the influential work of Graham and Dodd preceded the development of electronic spreadsheets leading them to propose short-cut estimates of value. Second, that academic research found evidence for the existence of a value premium, when value was defined using ratios such as those proposed by Graham and Dodd. The third was the rise of Warren Buffett as a value investing legend.

The demise of the value premium in the last twelve years has led to doubts regarding the efficacy of traditional value investing based on accounting ratios and efforts to adjust those ratios. The argument here is that such efforts are misguided. Instead, it must be recognized that value investing amounts to comparing estimates of fundamental value with price and that accounting ratios, however tweaked, are not a reasonable way to estimate value – it requires a full blown DCF analysis. When that criterion is employed many rapidly growing companies can turn out to be “value” stocks. Of course, this definition has the problem that value is then in the eye of the beholder, because it depends on the forecasts of the analyst. Unfortunately, that is an unavoidable fact of estimating value.

There is a way in which the proposed new definition of a value stock is related to the traditional, ratio based, distinction between value and growth. Using the DCF model the market value of a stock and be decomposed into two components: one focused on near-term observables and the other reflecting long-term speculative value. Stocks with a relatively high long-term speculative value can be thought of as comparable to growth, but the definition depends on valuation, not accounting ratios. Initial empirical results do show that stocks with high speculative values at the start ran up more as the market appreciated in 2020. In this context, the critical question for value investors, interpreted as investors who make decisions by comparing with DCF values with price, is whether the expectations for distant cash flows impounded in market prices have become exaggerated. That is not an issue of value versus growth, but a question of whether assessments of future growth are reasonable.

Bradford Cornell is a Professor of Finance at the Anderson Graduate School of Management, UCLA, and a senior advisor, Cornell Capital Group.

References

Arnott, Robert D, Campbell R. Harvey, Vitali Kalesnik, Juhani T. Linnainmaa, 2020, Reports of value’s death may be greatly exaggerated, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3488748.

Asness, Clifford, Tobias Moskowitz, and Lasse H. Pedersen, 2013, Value and momentum everywhere, Journal of Finance, 68 (3) 929-965.

Asness, Clifford, Andrea Frazzini, Ronen Israel, and Tobias Moskowitz, 2015, Fact, fiction, and value investing, Journal of Portfolio Management, 26, 50-60.

Basu, Sanjoy. (1977) Investment performance of common stocks in relation to their price-earnings ratios: A test of the efficient market hypothesis, Journal Finance, 32 (3), 663-682.

Bebchuk, Lucian, A, 2021, Don’t let the short-termism bogeyman scare you, Harvard Business Review Magazine, Jan-Feb.

Cornell, Bradford, and Aswath Damodaran, 2021, Value Investing: Requiem, Rebirth or Reincarnation? https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3779481.

Dimson, Elroy P., Paul Marsh and Michael Staunton, 2020, Credit Suisse Global Investment Returns Yearbook, Credit Suisse/London Business School.

Easton, Peter, and Greg Sommers, 2007, Effect of Analysts’ Optimism on Estimates of Expected Returns Implied by Earnings Forecasts, Journal of Accounting Research, 45 (5), 983-1015.

Fama, Eugene and Kenneth R. French, 1992, The cross-section of expected returns, Journal of Finance, 47 (2), 427-465.

Graham, Benjamin, and David Dodd, 1934, Security Analysis, McGraw-Hill, New York.

Graham, Benjamin, 1949, The Intelligent Investor, Harper & Brothers, New York, NY.

Holthausen, Robert W. and Mark E. Zmijewski, 2020, Corporate Valuation, 2nd ed., Cambridge Business Publisher, New York.

Israel, Ronen, Kristoffer Laursen, and Scott Richardson, 2020, Is (systematic) value investing dead? https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3554267.

Lev, Baruch and Anup Srivastava, 2020, Explaining the recent failure of value investing, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3442539.

Maloney, Thomas and Tobias J. Moskowitz, 2020, Value and interest rates: Are rates to blame for value’s torments, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3608155.

Olson, James, 1995, Earnings, book values, and dividends in equity valuation, Contemporary accounting research, 12, 661-687.

Penman, Stephen, 2010, Accounting for value, Columbia Business School publishing, New York.

[1] Cornell and Damodaran (2021) contains a more extensive analysis of the work of Graham and Dodd and its impact on value investing.

[2] It is interesting to note in this regard that Warren Buffett often states that he only invests in businesses that he “understands.” Unfortunately, Mr. Buffett never defines exactly what he means by the word understands. In the context of the current analysis, it can be interpreted to mean that Mr. Buffett believes he “understands” businesses for which he can forecast future cash flows more accurately than the market consensus.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All