Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Issues such as the convertibility of paper currency to gold and the viability of modern monetary theory (MMT) were addressed more than 200 years ago by England, soon after the U.S. became independent.

On February 22, 1797, the Black Legion – 46 officers and 1,178 soldiers of France’s Revolutionary Army – landed in Wales, near the port of Fishguard. La Seconde Légion des Francs had acquired its nickname from the dark brown cloth of uniforms. They had been dyed to cover up their original colors – the red, white, green, yellow, blue and orange threads that were in the various weaves worn by the Scottish, Yorkshire and Somersetshire regiments of Foot and Irish Dragoon guards. Those men had been forced to leave behind their spare uniforms, along with most of their muskets and cannon, when the 1795 English-French Royalist attack on the Quiberon Peninsula had failed. The Black Legion’s landing was equally unsuccessful. Two days after coming ashore, the Black Legion would surrender to the local Welsh militia.

That same evening the first bits of information about the events around Fishguard would begin to arrive in London and become the news. On the following day, Saturday, February 25, the Morning Chronicle and the Morning Herald would publish the story: England invaded by Revolutionary France! When the Bank of England opened for business, a number of its account and note holders politely but firmly pressed their way towards the cashiers’ windows to demand exchanges of paper into coin. By the end of the day, nearly half of the bank’s gold coin had been paid out in redemptions. (The bank held no reserves of silver; ever since Isaac Newton’s recoinage had set silver coins’ official denominations below their exchange price, the country had been drained of the metal. To supply even a minimum amount of sterling, the Royal Mint had resorted to restriking the Mexican and very few American silver dollars it got its hands on.) On Sunday, the bank's doors remained closed, as usual; but there was one bit of business that did occur on the Church of England’s official day of Sabbath. A printed notice appeared on the bank’s front door: by parliamentary order, all redemptions were suspended until further notice.

In the week that followed, the full details of what happened in Wales would arrive in London, but the county militia’s success in defeating the invasion would not bring any reversal of government policy. The Bank of England was going to hoard whatever gold coin it still held. Parliament’s fear was that the private holders of specie, unlike the Bank of England, would not provide the coin the Exchequer needed for bribes to England’s continental allies against the French. For the depositors and note holders who had exchanged paper for coin, the fear was that the government itself would be overthrown. The strength of the Bank of England itself was not in question. How could it be? For most of the 18th century, the Bank of England’s notes had not been merely a convenient substitute for coin; for the capital markets they had become the form of England’s money. They had to be. The Royal Mint’s production problems left it unable to provide the country with sufficient coinage in any denomination – large or small. Necessity had led to the common law making the Bank of England’s notes lawful tender for payment of judgments. In the absence of a uniform coinage, only Bank of England notes were accepted for the clearing of net balances owing from trades of private bills of credit, the notes of country banks, bonds funded by the commitment of specific tax revenues (funded debt) and the short-term borrowings by the Exchequer (unfunded debt).

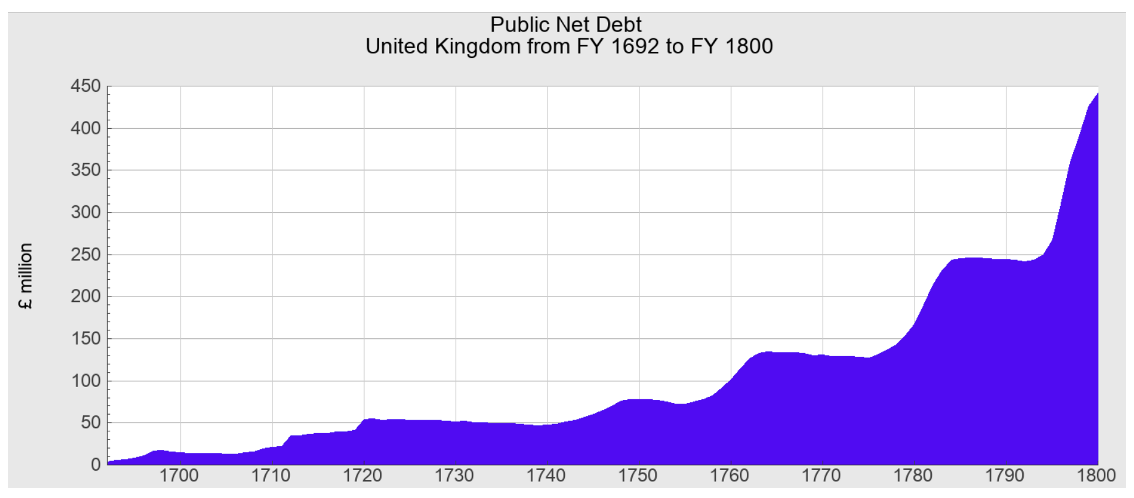

In suspending note holders’ rights to redeem paper for coin, Parliament was not cancelling its promise that the pound sterling issued by the Bank of England would be the country’s official store of value. The sovereign legal monopoly over money was unchanged. As with the present law for Federal Reserve notes in the U.S., it was, in 1797 in England, a criminal offense to refuse acceptance of the denominated IOUs of England’s national bank as full and complete payment. The denominations of the credit currency of the Bank of England were full and complete lawful tender, to be accepted at face value in all domestic exchanges. It was a century too late to worry about England’s central bank printing money. The big bang of the Glorious Revolution had powered a cosmological inflation of credit, and the sovereign authority of Parliament had been the assurance that English public debt was the safest of all possible investments. The 109-fold increase in public debt from 1692 to 1797 had established London as the center of European and American finance.

Unlike the Bank of England, the Bank of the United States had no monopoly authority. Its demand notes, like all those issued in the country, were legally required to be redeemed at par for coin when presented for exchange; but the notes themselves were not legal tender. Yet, the country’s banking system had been able to continue honoring its promise to pay out gold for paper. The explanation for the difference between the United Kingdom and the United States was simple. American banks system operated under a system of open deposit and exchange; England’s banks did not. Under state and federal law, banks and their note and account holders were legally free to waive the requirements for immediate redemption by agreeing to exchange demand notes for those bearing interest and having a “post” date of redemption. Promises of redemption could be serially postponed. In the transactions between the Bank of the United States, the private and state-chartered banks and their customers, counterparties were free to “break the buck.”

In 1791, when the details of the new American financial system adopted by Congress and President Washington were disclosed, Parliament and the City of London had been quick to ridicule the former colonists’ plans for a banking system that allowed deposit and exchange at a discount. William Pitt had declared to Parliament: “Let the Americans adopt their funding system and go into their banking institutions and their boasted independence will be a mere phantom.” If one insisted that a country’s money must carry the promise of being a reliable and unchanging store of value, Pitt’s criticism of the American rules for money and banking had been completely justified. By allowing the active discounting of all exchanges of money and credit, the law of the United States had surrendered a fundamental part of government’s sovereign authority – the power to assign the price for a country’s legal tender. In addition to suspending redemption by the Bank of England, Parliament had made melting of coins into bullion and the export of gold in any form illegal. Technically, it was still within the law for people to use coin; but anyone buying or selling specie was automatically suspected of being a smuggler and a traitor. It would take the government of the United States another 140 years to exercise the same final authority over international exchange with the American Emergency Banking Act of March 1933.

In 1797 neither the federal government nor the governments of the states had the power to mandate the prices and terms for international financial promises. Under Article I of the new Constitution, Congress only had the authority, “to coin Money, regulate the Value thereof, and of foreign Coin”; and there was no automatic equivalence between national bank paper and coin. The American system of finance had no specie standard for money; amounts of gold, silver and copper were the currency. Everything else, including bank notes, was credit. Ideally, all commerce, taxes and government spending would be done in cash. John Adams, Thomas Jefferson and Alexander Hamilton shared that belief. Evan as they disagreed about the federal government having its own bank, they were unanimous in thinking that American banks, like everyone else, should only deal in money. Yet, thanks to George Washington and Thomas Willing, the country would establish a financial system founded on nothing but continuously discounted promises to pay.

In the last decade of the 18th century, George Washington and Thomas Willing were two of the very few genuinely wealthy men in the United States of America. Washington’s fortune had come from his successful efforts to improve his wife’s immense wealth; Willing’s wealth had come through his enterprise and use of family connections. Neither man had ever been broke nor come even remotely close to being poor, but they had the shared experience of working their way up the financial ladder from an early age. Their first experiences in dealing with the English rules for wealth and political power in the colonial world had been as outsiders looking in. As men who believed in the superior justice of representative republican governments in an age of elite nobilities and monarchies, they were genuine political rebels. They shared Thomas Paine’s belief in civil equality and were pleased that the American Constitution had outlawed “titles of nobility.” The two men did not share Paine’s faith in economic radicalism; they were not, in any sense of the word, economic revolutionaries. In making the national rules for money and credit, they had no hopes or desires for the United States somehow to escape the tyranny of international finance.

Both men were proud of their country’s democratically elected forms of government, both state and national; but they had no belief that the people and their representatives would bring any special financial wisdom to public affairs. They had consciously designed a banking system that would offer the American people unprecedented access to credit; but they had no expectations that any system of finance could change the distribution of wealth. On the contrary, their greatest concern was that American governments would, like all others in history, believe that the laws for money and credit could magically create wealth. Whether a country had a monarchy and parliament, a president and congress, or a direct democratic assembly, the people in office could be expected to commit the folly of all governments. They would presume that they should be the final authority on all subjects, especially those for the country’s money and credit.

Parliament had no doubt about its ultimate sovereignty; under the country’s common law constitution, it ruled as “the King in Parliament”. Unlike the Americans whose representative government was already being overrun by lawyers, the members of Parliament had the practical sense to understand that even absolute monarchies only achieved enduring success in collecting taxes and borrowing money for public spending when they allowed prices to remain ungoverned. The Bank Restriction Act and other wartime financial rules in England had continued the English system of prohibition against any discounting of legal tender; but Parliament had not seriously attempted to fix the other prices in the English political economy. They had even allowed the prices of the Exchequer’s debts to fluctuate. Parliament accepted the market’s purchases of the Exchequer’s loans at prices below par. There were no Napoleonic rules that threatened severe punishment to bank account and note holders from incorporating foreign exchange rates into their domestic pricing calculations. Neither the Crown nor Pitt’s Ministry had acted to prevent people from knowing the different prices for things depending on whether they were purchased abroad using gold coins or in England using the central bank’s five-pound notes.

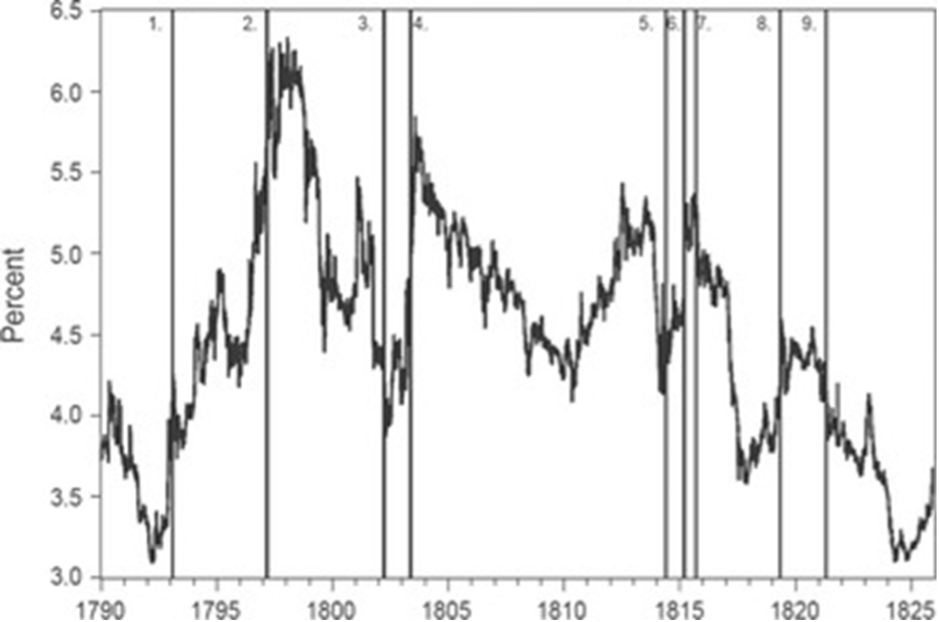

By accepting the implicit discounting of national credit currency against the prices set by international money, England was able to survive both suspension and war spending. A national financial system with an unobserved exchange standard was able to survive under a fatal weight of further borrowing. From 1797 to 1815, England’s already massive government indebtedness would triple, yet the interest rate on government debt would decline. From the date of suspension – line 2 in the chart below – to resumption – line 9 – the interest rate on Consols would fall from over 6%% to 4%.

From February 27, 1797, until May 1, 1821, all exchanges of bank notes and all uses of coin were subject to the terms of Parliament’s Bank Restriction Act; the only limits on the issues of notes by the Bank of England were the authorizations of Parliament. If you believe, as Henry Clay did, that the Congress could make whatever money it needed, then England’s money printing by its central bank during the wars against France could be taken as empirical evidence that MMT does work. Thomas Willing’s success in managing the overhang of America’s federal debt can also be taken as proof that public finance can work even when governments live only through central bank credit. The Bank of the United States was able to establish regular and reliable exchange of the Treasury’s debt before the U.S. Mint had even begun producing coin. (The $5 half eagle was first minted in 1795; the $10 eagle and $2.50 quarter eagle in 1796.) In both countries, for nearly a quarter century, there was no relation between national bank reserves of coin and the amounts of bank notes in circulation. What was the means of payment and where it came from did not seem to matter.

There was one great financial difference between our current world and the 1800 in England and the United States. When Parliament suspended redemption by the Bank of England, it did not replace specie as the international currency; international exchanges that could not be financed continued to be paid in gold and silver. In the domestic commerce of England and the U.S. the printed five-pound note and single-paper dollar were sufficient payment; for sending money between nations, only coin would do. The unit of account for any transaction in international commerce, including bribery, was not a national currency or an agency drawing right; it was a physical currency of scarce metal unregulated by any government authority. Neither England nor the United States nor any other country set the terms for the international exchange of their denominated national money. To be able to sell foreigners on the opportunity to invest in their national debts, both England and the United States had to use as their financial yardstick the international money whose supply was not under anyone’s control. To sustain their creditworthiness, the federal Treasury and the Exchequer had to pay the interest on their IOUs in amounts of gold, not denominations of credit currency. For the United Kingdom to be able to pay subsidies to its European allies against Napoleon, England had to have an inventory of gold and silver coin on hand – not as bank reserves but as metal to be shipped abroad.

By accepting the right of its creditors to discount its sovereign financial authority, Parliament was able to borrow and spend and borrow more in amounts that the world had never seen. But there was never a moment during and after the final war against France when the majority of the representatives in the English government were happy with success of open pricing. Both before and after the Restriction Act the fundamental premise of the English system of finance had been that the government’s pet bank would be the official referee for all financial intermediations, including international ones. The money supply, like the Royal Navy’s inventory of cannon, would be controlled by the sovereign and deployed according to the sovereign’s judgment. There had to be an absolute equivalence between the Bank of England’s notes and coined metal so that terms of its imperial trade had the United Kingdom being paid in pounds sterling for its exports. Having the Bank of England to print unredeemable currency had been a wartime necessity; but any final acceptance of open-ended credit exchange and financial discounting would subject a future Great Britain to the never-ending anarchy of its trading partners’ opinions about the value of English money. Parliament could not accept the continuation of any system that allowed prices in paper pounds allowed to go up while those in gold stayed unchanged or went down.

Under the final version of the Treaty of Paris – the one ratified after Waterloo – England’s share of the war reparations to be paid by the restored monarchy in France was a wonderful amount of international money. Measured by Parliament’s current rule for the price of its currency in gold, the Exchequer was to receive 16,000 pounds sterling each day for five years. France would also be liable for the costs that guaranteed payment – the feeding, pay and billeting of an allied army of occupation. For the first time in its history, the Royal Mint would be able to produce pound sterling coins in volume even as all restrictions on the export and import of specie were discarded. In 1818, 2,347,230 coins were minted. The result was as unexpected as the success of England’s wartime borrowing. The demand for specie in England literally collapsed. In 1819, the Mint would produce only 3,574 pound-sterling coins. Given a choice Bank of England notes, valued at par, and actual pounds sterling, the English continued to use paper. Even worse, it had become obvious to anyone who cared to look that the largest share of the Mint’s production had been exported to France so that it could be melted down and recast as bullion for the payment of reparations. In the year and a half that would remain before formal resumption the speeches in Parliament about finance would not debate whether or not the Bank of England could withstand another surge in demand for coin. The question that would be raised was how much freedom the Bank of England and other banks would have to continue issuing notes. “It is presumed,” Henry Boase had argued, “that …. the daily continued issues of new notes must inevitably grow to excess. If the Bank were not also daily occupied in retiring and cancelling its notes, this would be the case: but the first symptom of depreciation would naturally prompt the holders of Bank notes to hasten to get rid of an unprofitable and declining article; and the return of notes to the Bank must be always in the ratio of their superabundance or of their discredit.” If the effects on prices of two decades of war spending could not be blamed entirely on the number of bank notes in circulation, then the Americans’ system of discount could be continued. “If, therefore, Bank notes, though not convertible into specie, on demand, are convertible at will into gold or silver, or any other commodities, on equal terms with specie, there is exactly the same inducement to return the surplus to the Bank, as there was, when payment might be demanded in specie.” (Henry Boase, Remarks on the New Doctrine Concerning the Supposed Depreciation of Our Currency)

In discarding the belief that governments could hold money to a constant value, George Washington and Thomas Willing had established rules for American finance that were far more radically populist than Thomas Paine’s or any other advocate of revolutionary equality. People and banks should be free to gamble on each other’s credit in even the smallest amounts. A country’s internal economy could successfully grow using the exchanges of even the flimsiest of credit promises as long as people were free to price them. The cost of such a system was that no one, not even the sovereign government would be exempt from the unpredictable fluctuations of pricing. The Bank of England could set its rate of discount; but no sovereign authority could hold its money to a constant value. Even pure money exchanges would have a price risk. A bank could accept specie from a customer and be ready, willing and able to return the money when requested; but the bank’s flawless performance could not guarantee that the specie was worth what it had been when deposited with the bank. Under the Washington and Willing system of open exchange and discount there would be no protections against the unceasing fluctuation of the markets for money and credit. That would be the price of having the freedom to use whatever financial terms one chose. Individually, people would continue to be foolish, cowardly, dishonest, rash and stupid about money. Collectively, their judgment through continued open exchange would always prove wiser than any expert regulation.

For the policy majority in the government of the United Kingdom the success of the open pricing during the period of restriction was never going to be sufficient compensation for the loss of sovereign authority. There was one way to try to put an end to such financial anarchy. Issues of paper money and bank extensions of credit could be officially rationed. The central bank and the other banks in the financial system could limit the total supply of currency and credit to the amount that would keep prices unchanged. The sum total of finance for a political economy could always be properly governed by the setting of the correct level of required reserves and a universal price for all discounts.

To the relief of David Ricardo, William Huskisson and others, the arguments against their bullionist monetarism were rejected. In the name of prudence, the Bank of England and other banks would stop issuing one-pound notes. As a remedy for the Panic of 1825 five-pound notes would be withdrawn from circulation.

The full story of the misadventure of the last invasion of the British Isles is worth reading: https://military.wikia.org/wiki/Battle_of_Fishguard#23_February.)

Stefan Jovanovich manages the portfolio for The NJT Company, Inc., a family office based in Nevada.

Read more articles by Stefan Jovanovich