The Recovery will be Positive for Commodities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

It is a particularly good time to invest in the commodities markets. Global stimulus points to a post-pandemic boom in spending and economic revival. Governments are acting decisively to protect their citizens and businesses from the COVID-19 economic disruption, through tax cuts, investment incentives and helicopter money. Stimulus finances infrastructure, supports businesses and puts money in the pockets of consumers, heightening demand for commodities and the energy required to produce them, while boosting real GDP (figure 1).

Figure 1: Real GDP Growth %

The IMF expects the world economy to expand 6% this year, the fastest in IMF records since 1980i. President Biden’s $1.9 trillion economic package led economists to revise their growth forecasts. Goldman Sachs predicts the U.S. economy will be 8% larger by year end compared to last year, making it the fastest GDP growth since 1965. Goldman’s 2022 growth prediction is 5.1%.ii

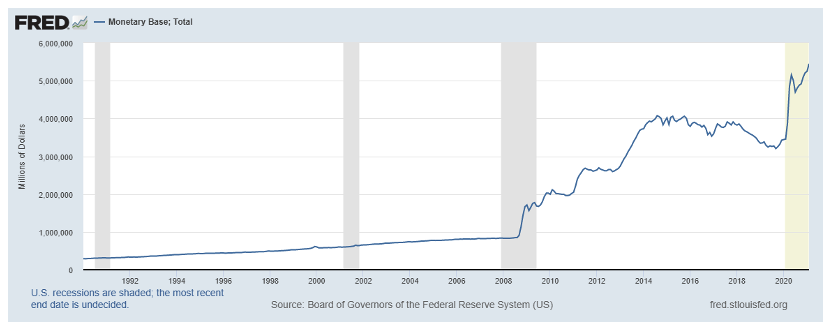

Expansionary policy can signal an inflation threat. Since 2008, the Fed has conducted aggressive monetary stimulus in the forms of zero interest rate policy and quantitative easing (QE) which, through the direct purchase of government and other bonds, has injected an unprecedented level of dollar liquidity in the economy. The U.S. monetary base increased from $850 billion in August 2008 to more than $4 trillion by year-end 2014 through three phases of QE. A fourth QE was done after the repo-market collapse in late 2019 and accelerated during the COVID financial crisis, bringing the monetary base to about $5.5 trillion and growingiii (figure 2).

Figure 2: US Monetary Base: Total

Commodity prices typically rise when inflation is accelerating as commodities offer protection from inflation effects. A good inflation indicator is the 10-2 interest rate spread – the difference between the 10-year and the two-year Treasury rates. A positive spread has historically been viewed as a precursor to inflation. The 10-2 spread peaked at 2.91% in 2011 and fell to a low of -2.41% in 1980.iv It has been climbing steadily throughout 2020 and the first quarter of 2021 (Figure 3).

Figure 3: 10-2 Year Interest Rate Spread

Source: Y-Charts

Global supply chain disruption resulted from COVID-19 heightened demand for goods and raw materials. The massive EVER GREEN containership, stuck in the Suez Canal in March, served to highlight the vulnerability of our interconnected world. The canal shutdown affected 15% of global container shipping capacity causing delays at ports worldwidev. Shipping analysts estimated the traffic jam held up nearly $10 billion in trade daily.vi Fortunately, President Biden and other world leaders are operating with the understanding that global supply chains are a source of strength.

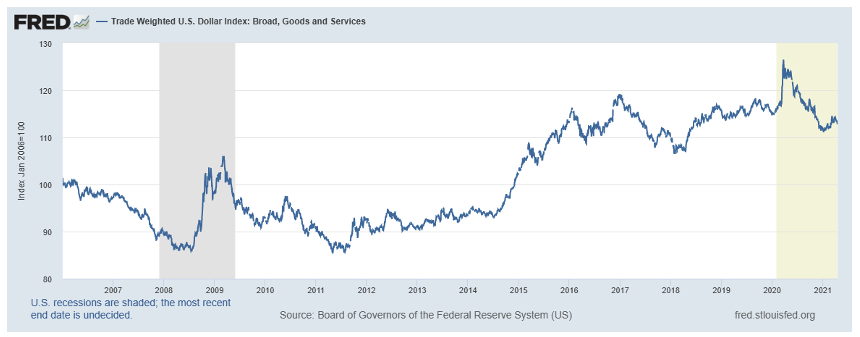

The dollar has an inverse relationship to commodity prices because most commodities are priced in dollars. When prices rally in dollar terms, demand decreases abroad, thus pressuring prices down. While the trend of the dollar index may be accelerating, the dollar is still considered relatively strong given the recent monetary shock administered by the Fed (Figure 4). Also, a rising U.S. deficit contributes to a weak dollar; the federal deficit stood at $3.1 trillion at the end of 2020 or approximately 15% of GDP – a level not seen since the height of World War II (figure 5). Unlike World War II, very little of the current budget deficit is being invested in productive assets, and instead into potentially inflationary consumption.

Figure 4: Trade Weighted U.S. Dollar Index: Broad Goods and Services

Figure 5: Federal Surplus or Deficit [-] as a Percent of GDP

The climate crisis increases the cost of production of many commodities due to stricter emissions and waste disposal standards. According to a University of Exeter study, The Impact of Weather on Commodity Prices: A Warning for the Future,vii an increase in temperatures is likely to increase commodity prices; the impact on prices is not only direct but it spills over to other exporting countries; simulating a scenario compatible with global warming is likely to lead to a substantial increase in commodity prices and spillover effects; and these effects are amplified if accounted for a contemporaneous shock to the economy.

Lastly, technology advancements in AI, machine learning, blockchain, crypto-currencies, digitization and 5G will bring added liquidity to the commodities markets.

Advantages and risks of investing

Advantages

Risks

Copper, corn and carbon credits: Ways to invest

Physical markets: One could invest directly by buying the physical raw material, but this is not suggested. One would need to store, protect and insure the commodity, which can be costly and arduous – with some exceptions in precious metals.viii

Futures and options: Only professionals or highly sophisticated investors should trade futures, options and derivatives, as they are highly complex and volatile. A holder (buyer) who is long a commodity future may be called for margin when the price drops. A similar situation can occur with a short (seller) position in rising markets.

Managed futures account: Trend following, actively managed funds are run by specialized investment managers called commodity trading advisors (CTAs). CTAs chose among different commodities in an effort to beat the benchmark. They hold positions in derivatives such as commodity futures, stock options and interest rate swaps. Some use leverage or take both long and short positions.

Commodity-producer stocks and bonds: One could invest in equity (public or private) or debt of a producer company, or in mutual funds and hedge funds that invest in those instruments. But those are not pure-play investments. Investors will be subject to idiosyncratic effects that move the price of equites and debt, independent of underlying commodity prices, such as changes in company management or market share. Additionally, market beta can cause one company’s equity or bond valuation to affect the entire sector.

Exchange traded products (ETPs) and indices: There are hundreds of commodity ETPs including funds (ETFs) and notes (ETNs) as well indices. These instruments directly track prices of commodities and thus, by default, are highly volatile. Volatility can be reduced by investing in a product holding a basket of commodities or choosing an actively managed account.

Forward curves: Understanding contango and backwardation

Contango and backwardation are terms used to define the structure of commodity forward curves. Forward curves are not forecasts; they represent the value of futures contracts for deliveries out into the future, typically governed by market sentiment. When a market is in contango, the forward price of a futures contract is greater than the spot price. Conversely, when a market is in backwardation, the forward price of the futures contract is less than the spot price. A contango can be considered an upward sloping curve while a backwardation can be considered an inverse curve.

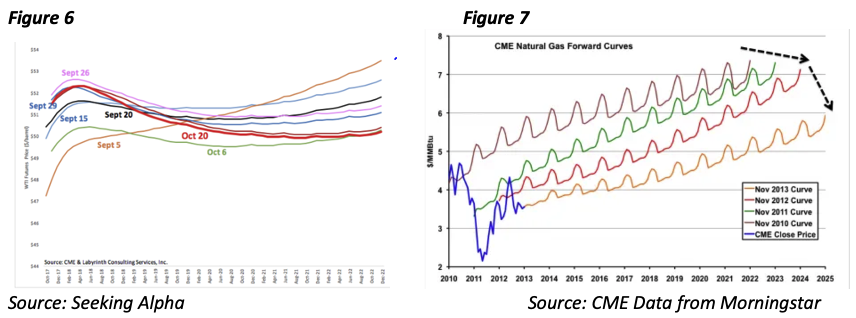

Efficient markets dictate contangos in commodity curves as future prices have greater value than today’s price (spot) when factoring for costs of storage, insurance and interest rates. But markets are not always efficient, and curves invert due to physical shortage (or anticipation thereof) from a spike in demand or production disruption. Figure 6 illustrates the structure of futures curves for West Texas Intermediate crude oil with near-term backwardations reflecting concerns of tightening supply and producer hedgingix.

Some forward curves exhibit both contango and backwardation due to seasonality. Figure 7 shows CME natural gas futures data over a four-year period Nov. 2010-Nov 2013x. The consistent waves represent seasonality in natural gas usage, albeit this consistency can shift quickly by a sudden shortage, oversupply or weather change. It is these market inconsistencies that that traders look for and profit from through a ”carry tradexi.”.

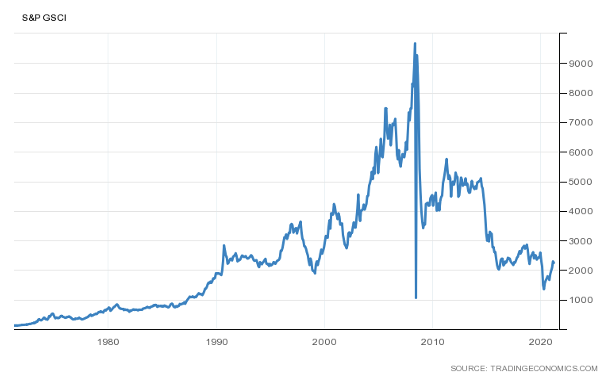

History helps to understand commodity forward curves. From 1991 through 2004 commodity prices rallied (figure 8) and most forward curves were backwardated. Backwardation creates yield premium rolling into lower-priced contracts while contango creates yield cost rolling into higher-priced contracts. Thus, long only traders lose money on the roll yield in contango markets.

Figure 8: S&P Goldman Sachs Commodity Index

Following 2005, a wall of passive, long-only money entered the market (pension and index funds) and distorted the curves to contango – a new paradigm in the commodity space. This meant that longs were hurt, even when prices were rising, as they had to pay the roll yield to maintain long contracts. Many commodity traders running hundreds of millions of dollars in legacy allocations struggled to profit. Furthermore, there was no inflation, which drove the correlations of commodities and equites to nearly 1 and minimized the commodity diversification benefits.

Thus, a better way to profit was to be short, but this is dangerous because when commodity prices rise, they tend to spike in response to a drought or mine closure. This led to a recognition that there is value in trend-following systems based on the carry trade rather than price. The models that were successful could profit while showing little to no correlation to the S&P 500 or even long commodity indices.

The trend is your friend…but not always

An RIA or fiduciary should understand the risks involved in commodity investing and explore available products. They must know if and how these products can enhance their clients’ portfolios from a risk management, diversification and profitability perspective. Consider these factors:

Calculation agentxii: An external party that serves as a calculation agent adds a level of security to any investment product. Examples are the S&Pxiii and ICExiv. These organizations not only originate and offer their own products but serve as calculation and tracking error agents for other listed products branded in their name. The agent serves as an extra set of eyes on valuation and ensures robust accounting.

Tracking error: Tracking error is the standard deviation of the difference between the returns of a portfolio and the returns of a benchmark, expressed both as an annualized number and as a percent. It sets approximate expectations for how large the difference between the benchmark and the portfolio return might be. A ”good” tracking error depends on the type of portfolio. Active managers generally have higher tracking errors than passive managers as they seek excess return through active positioning. Expect lower tracking error with passive managers, with differences triggered by mismatches in implementation, trading, imprecise cash flows, liquidity, etc. When comparing like-for-like funds, generally, the lower the tracking error, the better.

Slippage: Slippage, defined as a percent, is the difference between a trade’s entry or exit order price and the price at which the trade is filled. Its impact is simulated through back testing. Slippage can vary dramatically depending on market conditions at the time an order is executed. It is most prevalent during periods of high volatility, or when portfolio managers rebalance their holdings, place market orders or have large orders but there is little volume. When comparing like-funds, a low slippage is preferable.

Leverage: Commodities are risky assets. Adding leverage only increases this risk. While an index has no leverage, a manager can create leveraged versions of an index by offering 2x, 3x, etc. The greater the leverage, the riskier the investment as compounding can result in large losses in volatile markets. A triple-leveraged (3X) ETF comes with considerable risk and is not appropriate for long-term investing. A 3x ETF could face complete collapse should the underlying index decline by more than 33% in one day. Leveraged products use derivatives which introduce another set of risks.

Fully invested: Many funds are not fully invested, meaning some percent of assets under management remain in cash. A ”flat” position means the manager has neither a bullish nor bearish stance on a price or spread. But why pay a manager to sit in cash that earns no money?

Alpha versus smart beta

“Alpha” equates to excess return over the market, whereas “beta” is a measure of an instrument’s sensitivity to the movement of the overall market. The commodities market can be represented by the Goldman Sachs Commodity Index (GSCI) or the Bloomberg Commodity Index (BCOM), two of the more widely known, broad-based commodity indices. The beta of the GSCI or BCAM is expressed as 1.0. The beta of a commodity ETP or index is based on how it performs in relation to the index’s beta. An ETP with a beta of 1.0 indicates that it moves in tandem with commodity markets.

“Smart beta” refers to enhanced indexing strategies that seeks to exploit specific performance factors in the attempt to outperform the benchmark, thus differentiating it from traditional passive index strategies. Smart beta also differs from managed-futures accounts – primarily trend followers whose differentiating characteristics include markets traded, use of leverage, rebalancing techniques and fees.

Smart beta strategies seek to enhance returns, improve diversification and reduce risk by investing based on one or more predetermined and unique factors. Ray Murphy, a commodity index specialist, states, “Smart beta can exclude noise associated with ‘crowding’ and ‘roll slippage’ in commodity markets due to massive fund flows, factor herding, and varying cross-correlations.”

While commodity products are abundant, being sensitive to contangos and backwardations – by extracting commodity returns from spreads – could ultimately be the answer. Managers who incorporate or isolate the carry trade return component are concerned with the return stream of commodity investments, rather than the outright price of commodities such that the return stream is uncorrelated to long-only commodity indices as well as the broader markets.

RIAs and financial advisors should seek to maximize their clients’ portfolio potential by investing in transparent, highly liquid, low-fixed-fee commodity products. They should provide investors with profitable investment alternatives for those seeking an initial commodity exposure or looking to diversify a commodity allocation.

Shelley Goldberg was a commodities strategist for Brevan Howard Asset Management and Roubini Global Economics, a hedge fund manager for G3 Capital Partners and a contributing writer to Bloomberg Opinion.

i https://apnews.com/article/world-news-economic-growth-coronavirus-pandemic-economy-95c0c07f39af685fac274df73738f61a

ii https://www.cnn.com/2021/03/15/economy/stimulus-economy-biden-2022/index.html

iii Board of Governors of the Federal Reserve, Monetary Base, Total

iv Y-Charts

v Moody’s Investor Service

vi https://www.nytimes.com/live/2021/03/29/world/suez-canal-stuck-ship?campaign_id=9&emc=edit_nn_20210330&instance_id=28635&nl=the-morning®i_id=67794080&segment_id=54483&te=1&user_id=6ada279fb713fafa3f8f6a653c326db0#clearing-backlog

vii http://people.exeter.ac.uk/RePEc/dpapers/DP1902.pdf

viii Precious metals have a high value to content ratio making them easier to own in physical metal.

ix When producers purchase put options as a hedge, the counterparty (bank or brokerage house) covers its short put position by buying futures, thus driving up the price of the commodity.

x The blue line is the monthly average CME Henry hub futures market close price from Dec. 2010 to Dec 2013.

xi Commodity carry is a strategy involving profiting off the shape of the forward curve in addition to the additional component of the risk-free rate.

xii For the financial definition of a Calculation Agent, see: https://financial-dictionary.thefreedictionary.com/Calculation+Agent

xiii S&P Global Inc.

xiv Intercontinental Exchange Inc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All