Why don’t more business owners upgrade their current 401(k) plans to take full advantage of larger tax deductions and accelerated retirement savings?

The answer is misconceptions that include:

- “Retirement plans are too expensive to set-up and administer.”

- “They’re too complicated.”

- “I have to make a contribution every year.”

- “I have to provide the same contribution to the employees as for me.”

Why is this all important now? Because of COVID-19, many business owners, partners of firms, and others had to be shut down. Everyone is trying to make up for lost time and revenue.

That leaves less time for a business owner to focus on a new plan or try and improve their current retirement plan. They want to have at least a 401(k) plan in place for themselves and their helpful staff to retain talented employees and provide a retirement path. But can more be done than that?

Yes, with a profit-sharing 401(k) plan and a cash-balance plan.

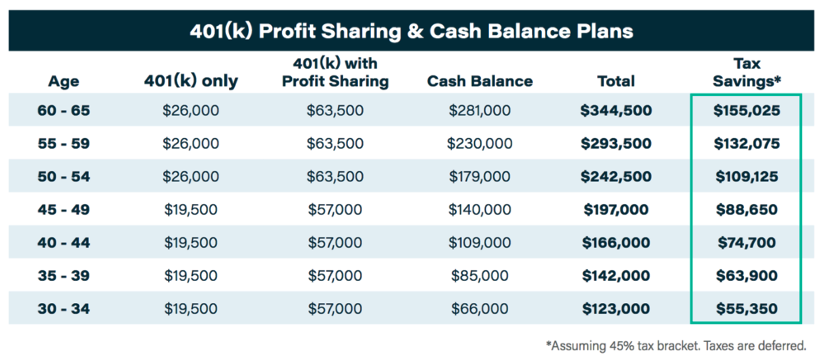

How much can be contributed to a profit-sharing or cash-balance plan?

The employer contribution, made by the business owner, is determined by a formula specified in the plan document. It can be a percentage of pay or a flat dollar amount. Below are the limits for 2020 (subject to change):

Can cash-balance plans be offered in addition to 401(k) profit sharing or other plans?

Yes, the owner can offer a combination of qualified retirement plans to produce a larger contribution. In fact, in most cases, a 401(k) profit sharing plan in conjunction with a cash balance plan is necessary to produce the maximum tax deductions and retirement savings desired for the owner and employee contributions.

What are the distribution options upon retirement or if leaving the employer? Any vested account in a cash-balance plan can be paid as a lump-sum distribution or annuity. A lump sum distribution can be rolled over to an IRA or another qualified retirement plan.

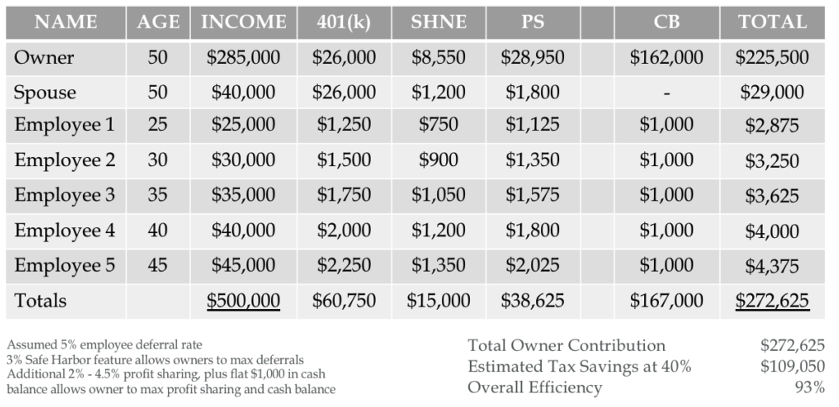

Case study example

- Business owner with spouse on staff, both 50 years old.

- Five employees with ages from 25 to 45.

- Looking to upgrade current plan with a profit-sharing 401(k) and a cash-balance plan to achieve larger tax deductions and accelerated retirement savings.

Here is an example of how a business owner can set up their profit-sharing 401(k), cash-balance plan with a safe harbor feature.

Related Articles: How To Understand Cash Balance Plans Without Being An Expert

Scott Krase is the founder and principal of CrossPoint Wealth and specializes in retirement planning for individuals over age 50. His blog is CommonFinancialSense.com

Read more articles by Scott Krase

Why don’t more business owners upgrade their current 401(k) plans to take full advantage of larger tax deductions and accelerated retirement savings?

Why don’t more business owners upgrade their current 401(k) plans to take full advantage of larger tax deductions and accelerated retirement savings?