There’s a new annuity in town: registered index-linked annuities (RILAs).1 Technically, RILAs aren’t new since they’ve been available for a decade. But given the increase in interest of RILAs and consistent growth in sales, advisors should understand the basics of the product and how it works.

There’s a new annuity in town: registered index-linked annuities (RILAs).1 Technically, RILAs aren’t new since they’ve been available for a decade. But given the increase in interest of RILAs and consistent growth in sales, advisors should understand the basics of the product and how it works.

RILAs are a riskier version of fixed-index annuities (FIAs), where the upside potential is higher than a FIA, but the investor has the possibility of incurring a loss (i.e., negative return), depending on the structure. There are two primary features of RILAs: floors and buffers. Floors limit the maximum potential loss (e.g., if the floor is 10%, you can’t lose more than 10% even if the underlying return is significantly worse), while buffers “absorb” the first amount of losses but subject the investor to the remaining downside (e.g., if the buffer is 10%, the first 10% of losses are covered, but that’s it).

I’m going to cover the features of RILAs, which is an options-based strategy, in a series of four articles, with part 1 dedicated to the basics. In part 2, I’ll review some of the different approaches that can be used to implement options-based strategies (e.g., ETFS). In part 3, I’m going to compare floors and buffers and review the some of the dynamics of the options pricing. Lastly, in part 4 I will consider these options-based strategies as part of total portfolio to understand where and how they might be a good fit.

While there are a number of important things to consider before purchasing any type of financial product, RILAs have the potential to be useful. Plus, as noted in the title – it’s good to have options.

The assembly process

Investors often want the impossible: infinite upside with no downside. While this isn’t a realistic goal, it is possible to implement a strategy with some upside potential that limits downside risk by using options such as puts and calls.

The “assembly process” creates an investment strategy that has upside potential with no downside risk and is depicted in the exhibit below. As an aside, a product with upside and no downside risk is effectively a FIA.2

Creating upside with no downside

Zero-Coupon Bond + Long Call - Short Call = Product Return

In this example, most of the initial investment goes to purchasing a zero-coupon bond, which is assumed to be free from default risk. The cost of the zero-coupon bond sets the budget that can be used to purchase call options to generate the potential upside (i.e., the “options budget”). For example, if the initial investment is $1,000, and the zero-coupon bond costs $980, the options budget would be $20 (ignoring any fees associated with operating or implementing the strategy).

The upside exposure in this example is obtained through buying an at-the-money and selling an out-of-the-money call option. The difference between the strike prices of the two options represents the potential upside. The higher the interest rate (i.e., the less the cost of the zero-coupon bond), the greater the options budget and the higher the potential upside.

An investor doesn’t have to purchase an annuity (e.g., a RILA), or any type of prepackaged product to gain the this type of market exposure. An investor could purchase a series of financial options to create the same risk profile. I will address some of this in part 2, where I compare DIY, ETF and RILA approaches.

With FIAs, RILAs, and other similar products, the upside potential is typically described in terms of the participation rate and the cap. The participation rate is the percentage return of the underlying index (e.g., the S&P 500) you can receive (or can be credited with) over the period. For example, if the participation rate is 50% and the underlier returns 30%, the product owner would only be credited with half the return (which would be 15%). The cap is the maximum potential credited return. For example, if the cap were 10%, the product owner could not earn more than 10% for the given period, even if the performance of the underlier was significantly higher.

FIAs can be attractive for investors who want some upside potential but are risk averse (i.e., don’t want to lose money). FIAs are low-risk strategies and a potential substitute for bonds.

Evolving market dynamics

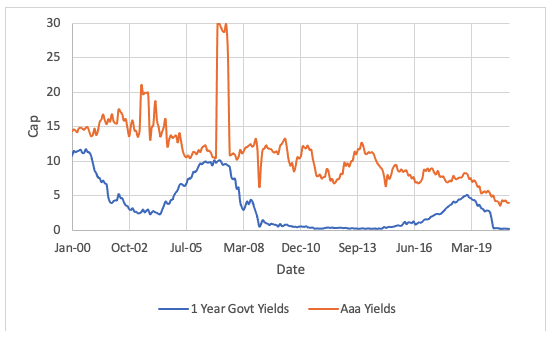

The decline in interest rates over the last several decades has resulted in a decline in options budgets. I demonstrate this effect in the exhibit below, which includes an estimate of how the cap on an investment with a one-year term with hedged exposure to downside risk has evolved from December 1999 to December 2020. The options prices are based on data from deltaneutral.com. The analysis assumes the options budget is based on one-year government yields (i.e., the risk-free rate for an individual investor) or Moody’s Aaa yields (which better reflect the options rate for insurance companies). Since options are not generally available that have a precise one-year expiration for each period, I used interpolation and run a series of regressions to estimate the costs. No additional fees or expenses are assumed for the analysis.

Historical cap rates on one-year caps for an investment with no downside risk: 2000-2020

The reduction in caps over the period can largely be attributed to the reduction in bond yields; however other factors come into play, such as implied volatility. I’m going to spend more time exploring implied volatility in part 3, but, for readers not familiar with the term, it is the volatility (i.e., input) that yields a theoretical value for the option equal to the current market price of that option when using a pricing model (such as Black-Scholes).

While implied volatility has been historically correlated to past (realized) volatility, it is a forward-looking measure. Implied volatility has not been constant across strike prices (i.e., the “smile” or “smirk” of option prices), which is important because different options are used to “build” the respective strategies (more on this part 3).

RILAs: More up with more down

The decline in caps for products with no downside risk (e.g., FIAs) makes them less attractive to investors who want more potential upside. RILAs should be attractive to those investors, who will accept some downside risk, with a cap (i.e., upside) that can be increased.

RILA strategies typically come in two flavors: floor and buffer. With floor products the downside is limited to a stated percentage, such as 10%. For example, if the floor is 10%, apart from the insurer’s default or inability to honor its claims-paying commitments, you can’t lose more than 10% regardless of the return of the underlier (e.g., the S&P 500). A RILA with a 0% floor would have the same risk profile as a FIA.

With buffer products, the first amount of loss is absorbed by the product, based on the buffer level; however, the investor would suffer any loss beyond that point. For example, if the buffer is 10% and the return of the underlier was -40%, the investor would lose 30%. If the return of the underlier is negative but greater than the noted buffer, the return would be 0% (e.g., if the buffer is 10% and the underlier returns -5%, the investor return would be 0%).

The additional upside from RILAs (versus FIAs) is generated through the premiums associated with accepting the potential losses (i.e., selling put options). The greater the potential loss, the higher the potential upside (generally speaking).

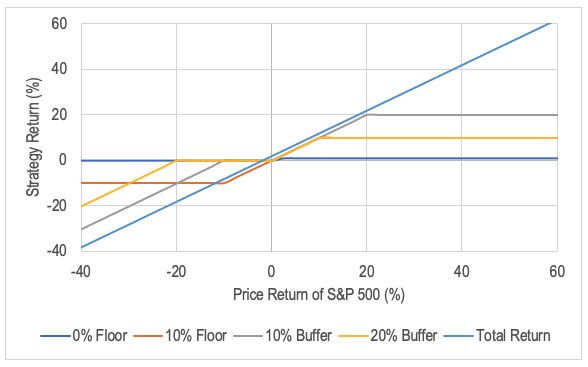

The return distribution of a RILA is going to vary significantly depending on the approach (e.g., floor versus buffer) as well as the prices of the zero-coupon bond and options purchased. This effect is demonstrated in the exhibit below, which includes the expected returns for different RILA strategies assuming the underlier is the S&P 500. The cost of options required to build the strategies is based on the Black-Scholes options pricing model, which I will discuss in greater detail in part 3.

Strategy returns versus price return of the S&P 500

An investor who directly purchases the S&P 500 (e.g., through an ETF) would earn the total return of the index (minus the investment’s fees and expenses), which is a combination of price return (capital appreciation/depreciation) and income return (dividends). Within a RILA framework, or really any type of options-based strategy, the return of the strategy would be based on the price return of the respective index (i.e., excluding dividends). This is why the “total return” in the above chart is always higher than the RILA products for a given (positive) price return.

There is a tradeoff across product exposures for positive and negative S&P 500 price returns. For example, the upside (i.e., cap) for the 0% floor is the lowest, but so is the downside (you can’t lose money).

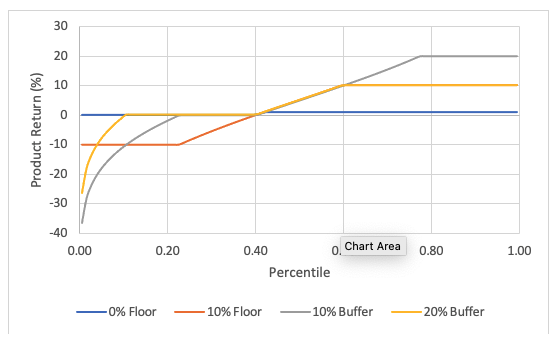

If we assume the annual returns of the S&P 500 follow a normal distribution, with an average expected price return of 5% and a standard deviation of 20%, we can estimate the probability of different returns for the various strategies, which are included below.

Distribution of strategy returns

These results look a lot like the previous chart, but this chart more accurately reflects the expected probability of the different outcomes. The downside risk of the 10% buffer is the greatest, but so is the upside. For example, it has the lowest return among the four products approximately 10% of the time, but the highest return 40% of the time.

The differences in the return profiles suggests that different types of RILAs are likely to be attractive to different types of investors. It’s more difficult to define the risk of RILAs from an equity risk perspective. For example, while FIAs are bond-like, since there is no downside risk, RILAs have significantly different risk profiles depending on the structure and the buffer and cap levels, which makes the risk of a RILA harder to measure.

Floor strategies are generally more “bond-like” than buffer strategies, since floors have a higher level of certainty of the maximum potential loss (i.e., the floor). There are exceptions, though. For example, a RILA with a 20% floor would be relatively risky even though the downside is capped.

Conclusions

As annuities become increasingly available (and of interest) to different types of advisors (e.g., the rise of fee-friendly annuities), advisors must understand how the various products work for different investors.

RILAs represent an interesting twist on more traditional annuities that employ options strategies, such as FIAs, given the higher possible upside return. But RILAs also have varying levels of downside risk. The differences in the expected return distributions of RILAs, which can be significant, make it difficult to generalize the effective risk of the products (i.e., whether they are substitute for equities, fixed income, or both), but it makes them attractive to a wider range of investors.

In part 2, I will address different product structures (DIY versus ETF versus RILA). In part 3, I will contrast buffers and floors directly and spend more time exploring options pricing. Part 4 will offer some optimizations using a utility-based resampled model.

While the benefits of RILAs, like any financial product, are investor-specific… it’s good to have options!

David Blanchett is head of retirement research for Morningstar Investment Management LLC. Views expressed are his own and do not necessarily reflect the views of Morningstar Investment Management LLC. This blog is provided for informational purposes only and should not be construed by any person as a solicitation to effect, or attempt to effect transactions in securities or the rendering of investment advice.

Note: all charts are for illustrative purposes only.

1 RILAs also have few other common names, such as indexed variable annuities and structured annuities, but I’m sticking with RILAs for this piece!

2 Assuming the product is held to its term and ignoring the implications of insurer default

Read more articles by David Blanchett

There’s a new annuity in town: registered index-linked annuities (RILAs).1 Technically, RILAs aren’t new since they’ve been available for a decade. But given the increase in interest of RILAs and consistent growth in sales, advisors should understand the basics of the product and how it works.

There’s a new annuity in town: registered index-linked annuities (RILAs).1 Technically, RILAs aren’t new since they’ve been available for a decade. But given the increase in interest of RILAs and consistent growth in sales, advisors should understand the basics of the product and how it works.