Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Low probability, high impact, unexpected events in the financial markets and the economy (“black swans”) are evoked to explain financial crises.

Yet, black swans are rarely as surprising as the concept suggests. The dot.com bubble was acknowledged during 1999, well before its eventual collapse during 2000-2002. Similarly, the ingredients of GFC in 2008, particularly the jitters in the credit markets, were manifest in 2007. Long before the Lehman collapse in September 2008, Bear Stearns failed in March 2008. Even earlier, in July 2007, two Bear Stearns hedge funds (the Bear Stearns High-Grade Structured Credit Fund and the Bear Stearns High-Grade Structured Credit Enhanced Leveraged Fund) were forced to shut down.

The “surprise” factor about black swans concerns is less its presence and more the mechanisms of its build-up and the timing of its unwinding.

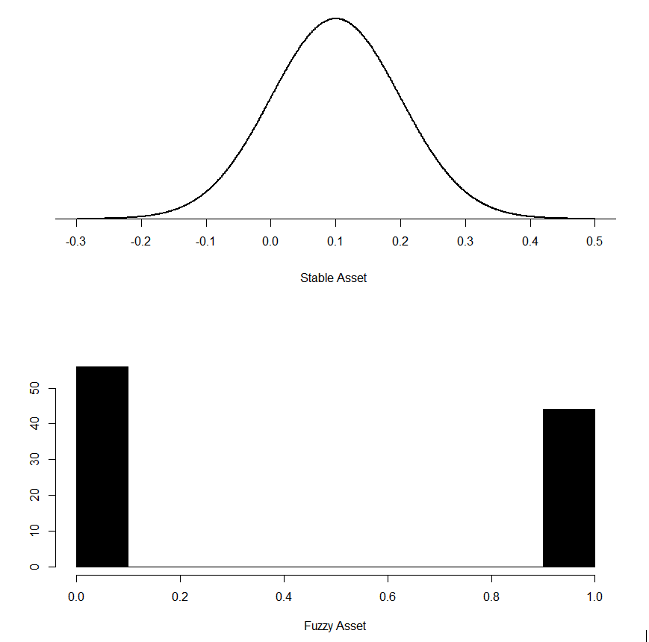

The financial theory of investments relies on their stability. This is implicit in the use of Gaussian (bell-curve) distribution and volatility in modeling both individual stocks and indices such as the S&P 500. The Gaussian distribution belongs to a class of stable distributions. However, for the last several decades, markets have faced a phenomenon that compromises this stability: lack of listing on exchanges and the distribution of less stable assets.

In many situations, instability is an integral part of the investment case. Within the venture capital (VC) industry, for instance, startups emerge from an unprofitable, unstable state to a profitable and stable one. Further, this instability is underwritten mainly by VC equity and is rarely debt financed.

Let us call assets, when listed but unstable, “fuzzy” assets.

When instability is listed in financial markets, four things happen:

- Markets price it continuously.

- The investment is shared across multiple balance sheets, not just one (entangled balance sheets).

- Since selling fuzziness into the public markets is extremely profitable, there will be abundant supply of fuzziness.

- Markets do not price fuzzy assets efficiently.

In the equities markets, instability can be due to euphoria, irrational exuberance, or optimism about a new structural and disruptive change.

Return distribution of stable assets (top) vs. fuzzy assets (bottom)