Safe-withdrawal rate (SWR) research has traditionally assumed annual portfolio rebalancing, and this is the frequency suggested by many advisors (although some suggest quarterly, monthly, or even daily rebalancing!). But is such frequent fiddling necessary? Rebalancing generates costs in fees and commissions and, depending on the type of account, will trigger tax liabilities.

Safe-withdrawal rate (SWR) research has traditionally assumed annual portfolio rebalancing, and this is the frequency suggested by many advisors (although some suggest quarterly, monthly, or even daily rebalancing!). But is such frequent fiddling necessary? Rebalancing generates costs in fees and commissions and, depending on the type of account, will trigger tax liabilities.

I used the “Big Picture” client education software to examine the impact of rebalancing frequency on historical SWRs and other retirement outcomes. The results argue against the notion to rebalance often.

Approach

The Big Picture software allows advisors to build hypothetical portfolios using up to 11 major asset classes and back-test them over hundreds of rolling historical periods at one-, three-, and five-year rebalancing frequencies.

The Big Picture program uses actual historical performance of indexes and inflation, based on monthly frequency total return data.

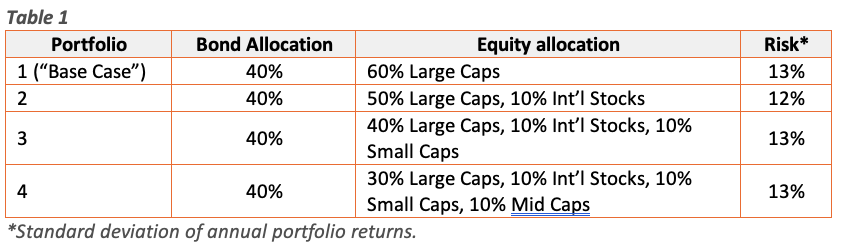

To test the effect of different rebalancing frequencies, I started with a “base case” portfolio of 60% large-cap stocks and 40% intermediate-term government bonds. I created three additional portfolios by holding the bond allocation constant while adding other equity classes. Portfolio 1, our 60/40 base case, had one equity class. Portfolio 2 had two equity classes. And so on, up to Portfolio 4.

The following table describes the composition of the test portfolios:

Adding equity classes in a different order would have produced different results. I chose the above order to ensure that all portfolios (except portfolio 1) contained international stocks – a frequently recommended constituent for achieving diversification.

Findings

Safe-withdrawal rates

Retirees’ greatest concern is their SWR. Did rebalancing at less-frequent rates diminish a portfolio’s SWR and, if so, by how much?

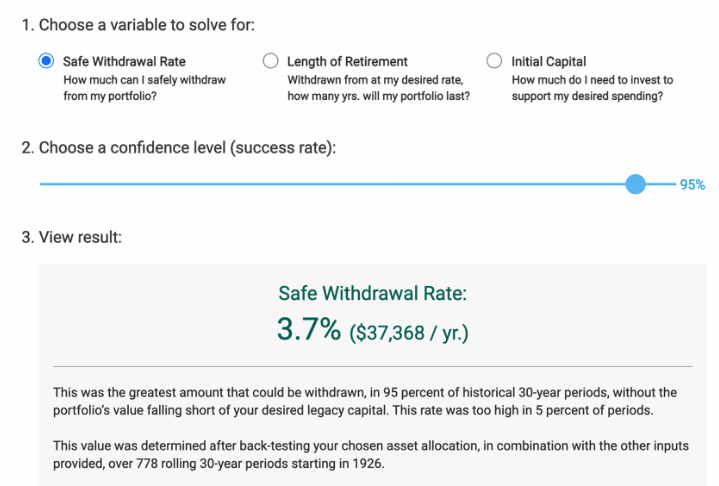

To answer this question, each of our four portfolios was back-tested over rolling 30-year retirement periods. Additionally, a confidence level (i.e. success rate) of 95% was selected. This meant that the software would solve for the greatest withdrawal rate that allowed the portfolio to remain solvent in 95% of historical 30-year periods (in 5% of periods, the withdrawal rate would be too high, and the portfolio would be exhausted before the 30 years were up).

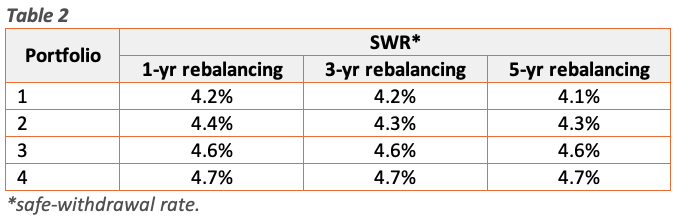

By the light of this experiment, the impact of rebalancing frequency was negligible. Portfolio 1 (base case) sustained a 4.2% withdrawal rate in 95% of historical 30-year periods when rebalanced at one- and three-year intervals, and a 4.1% withdrawal rate when rebalanced at five-year intervals. Portfolio 2 had similar changes in SWRs at the various rebalancing frequencies, while portfolios 3 and 4 had zero change in their SWRs, even when rebalanced at five-year intervals.

The following table summarizes these results.

These results, and all others discussed here, relate to the specific asset classes and weightings tested; adding other types of holdings, or different weightings, would have yielded different outcomes.

Portfolio longevity

The Big Picture software will solve for the historical longevity of a portfolio at different withdrawal rates and confidence levels.

As with SWRs, there was no decrease in longevity at with less frequent rebalancing. Small differences (of one year) were occasionally seen as the rebalancing frequency varied, but generally portfolio longevity was unaffected.

Minimum required nest egg

Provided a required spending level in retirement, asset allocation, and confidence level, the Big Picture will also solve for minimum required initial capital. Using the same 95% success threshold and 30-year timeframe as above, as well as a required $40,000 in CPI-adjusted annual spending, portfolio 1 historically would have needed a starting balance of $950,000 when rebalanced annually. Portfolio 2, meanwhile, needed a starting balance of $914,000, and portfolios 3 and 4 would have needed $879,000 and $857,000, respectively.

Once again, reducing the rebalancing frequency from annual to three- and five-year intervals did not produce substantial changes to the minimum required nest egg for any of the portfolios.

The Big Picture allows you to solve for different variables.

What about portfolio “drift”?

Some advisors are concerned that, absent frequent rebalancing, portfolio allocations will “drift” and unacceptably alter the investor’s assumed risk (where “risk” is measured as volatility).

Such concerns are overblown. Firstly, let us acknowledge that risk profiling, and hence asset allocation, is part science, part art. Risk tolerance is not consistently determined among advisors. It is determined differently by risk assessments and questionnaires, at different times in clients’ lives, and at different times in the markets. There is no definitive, static “risk number” for a given investor, and hence no reason to fret if portfolio allocations are not perfectly constant over time. It is more helpful to think in terms of allocation ranges than fixed percentages.

While substantial portfolio drift can bring greater volatility, small deviations from the original allocation are less likely to be problematic. The emotional cost of somewhat greater portfolio volatility must be weighed against the actual dollar savings of reduced friction.

Equities have at times entered extended periods of lower volatility, even as their growth has outpaced bonds and other asset classes. In these cases, portfolio volatility has actually decreased as equity allocations have drifted upward.

Try the Big Picture App

Free 30-day trial

Use the Big Picture App in client meetings. Illustrate how much money your clients need to retire or how much they can withdraw under various scenarios.

Click here to start your trial

Conclusion

In none of the test portfolios did less-frequent rebalancing produce substantially lower SWRs, reduced portfolio longevities, or higher minimum required nest egg balances. Rebalancing frequency had little to no bearing on these crucial metrics.

Retirees who wish to avoid the frictional costs of frequent rebalancing and who can tolerate some “portfolio drift” (and possible changes in portfolio volatility resulting from such drift) should consider rebalancing less frequently.

Ryan McLean is the founder of BigPicApp.co. He worked previously as an equity analyst at Morningstar. He holds an MBA in finance from McGill University.

Note: Historical data range from January 1, 1926 to December 31, 2020.

More Global Markets Topics >

Safe-withdrawal rate (SWR) research has traditionally assumed annual portfolio rebalancing, and this is the frequency suggested by many advisors (although some suggest quarterly, monthly, or even daily rebalancing!). But is such frequent fiddling necessary? Rebalancing generates costs in fees and commissions and, depending on the type of account, will trigger tax liabilities.

Safe-withdrawal rate (SWR) research has traditionally assumed annual portfolio rebalancing, and this is the frequency suggested by many advisors (although some suggest quarterly, monthly, or even daily rebalancing!). But is such frequent fiddling necessary? Rebalancing generates costs in fees and commissions and, depending on the type of account, will trigger tax liabilities.