The Case for Emerging Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits With U.S. equity valuations very rich by historical standards, many – including Jeremy Grantham, Rob Arnott and Vanguard – are predicting emerging markets to excel. I’ll examine the case and give my thoughts on how to invest in emerging markets.

With U.S. equity valuations very rich by historical standards, many – including Jeremy Grantham, Rob Arnott and Vanguard – are predicting emerging markets to excel. I’ll examine the case and give my thoughts on how to invest in emerging markets.

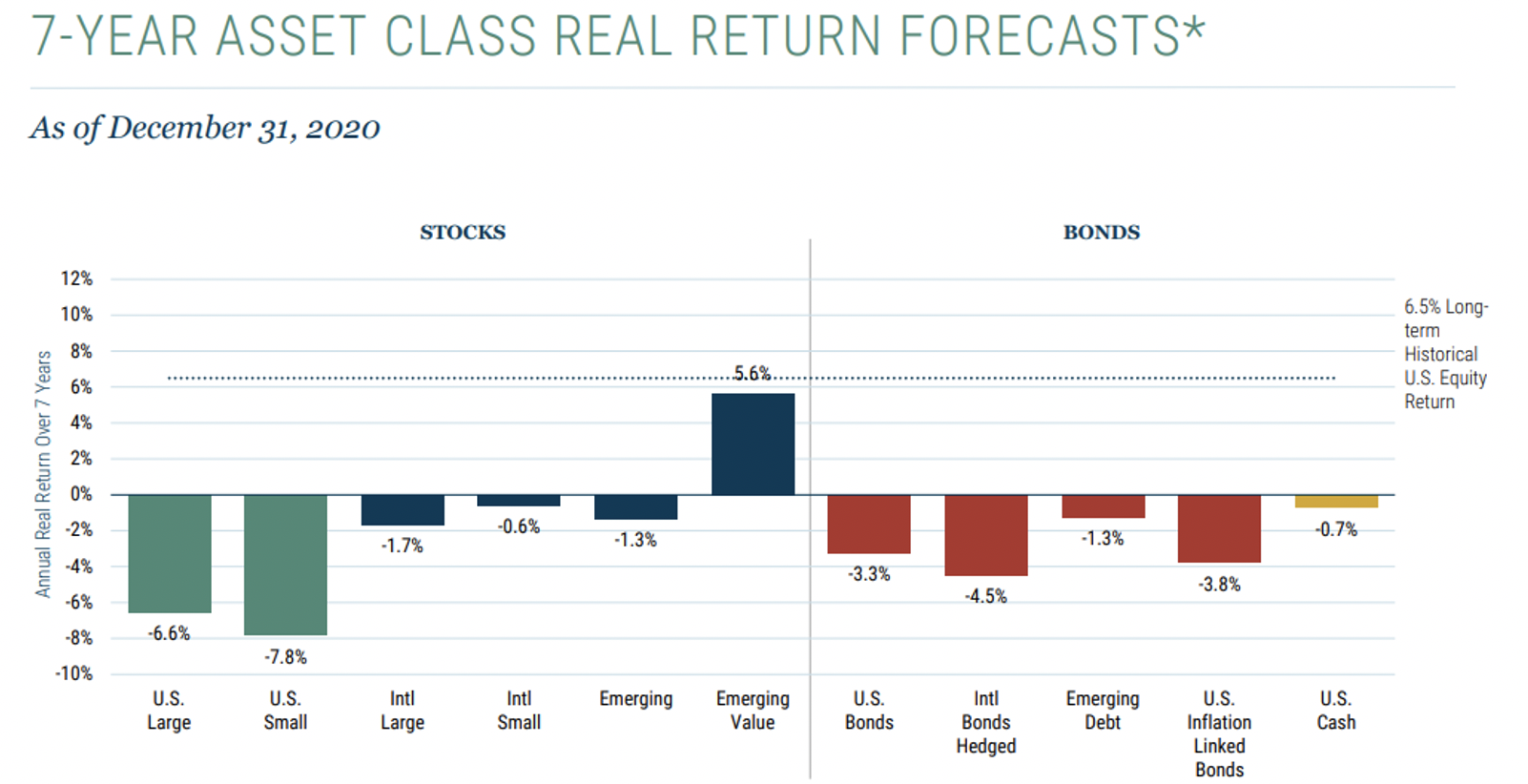

Grantham’s GMO is predicting emerging-market value stocks to outpace inflation by 5.6% annually over the next seven years. This is in stark contrast to U.S. large cap lagging inflation by 6.6% annually and small cap lagging by an even greater 7.8% annually.

And there is no safety in bonds, also lagging inflation dramatically.

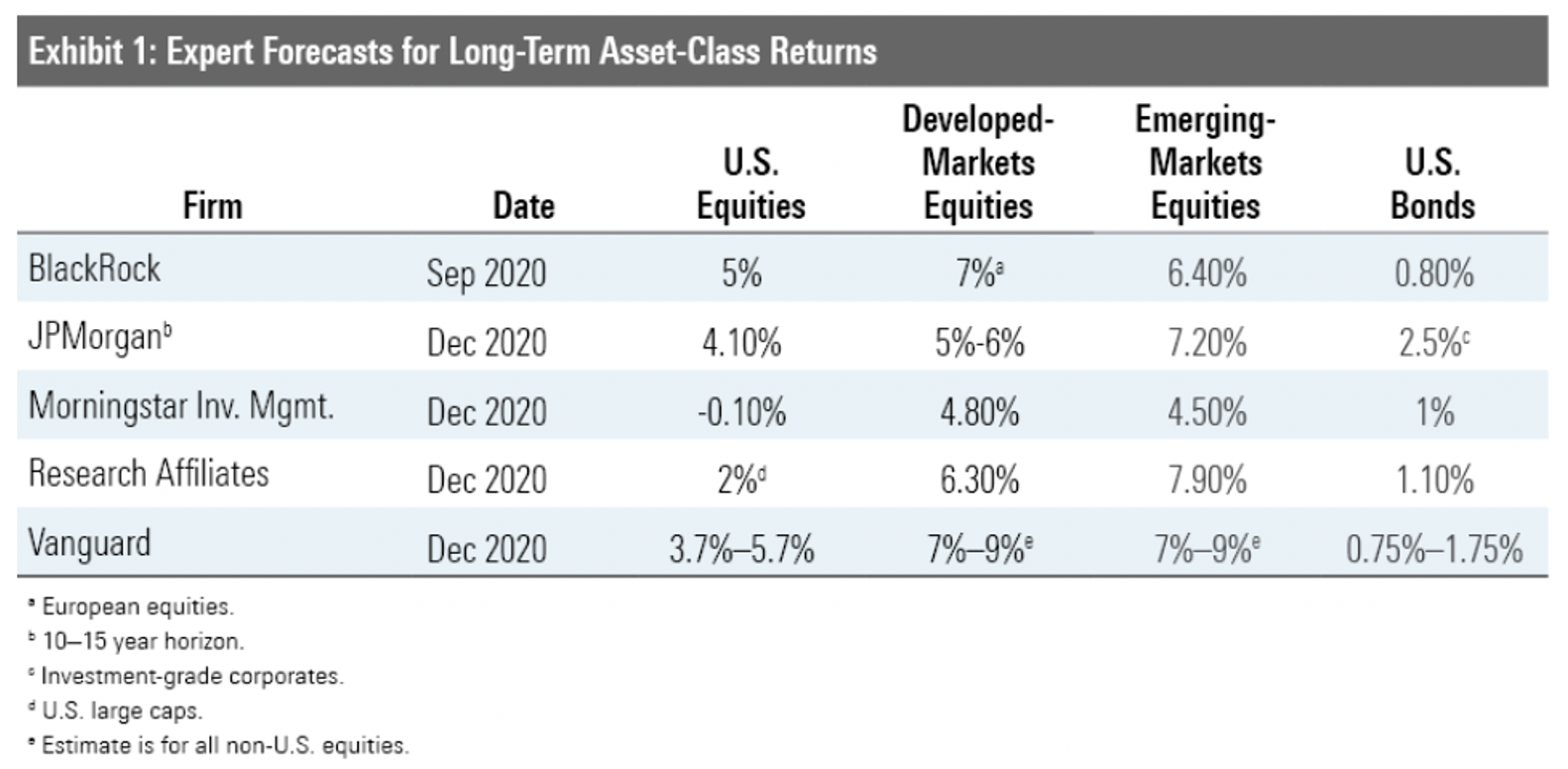

Jeremy Grantham isn’t alone. Morningstar’s Christine Benz summarized experts’ long-run forecasts, also using real inflation-adjusted returns.

Research Affiliates and Vanguard agree with Grantham on emerging markets and predict real returns between 4.5% and 9% annually, though they also predict international-developed markets will perform nearly as well as emerging markets. While not as pessimistic as GMO, the other experts predict muted US stock returns between a small loss and a 5.7% annual gain.

Based on those expert forecasts, there is a strong case for at least overweighting emerging markets and emerging-markets value in particular.

Examining the experts’ track record

Before placing credibility in a forecast, let’s take a step back and look at the past. I can’t rule out that luck played a part in a few forecasts being accurate, but it can certainly give me pause if their track record is poor.

I first went back seven years to look at GMO’s forecast to see how well things turned out. While not exactly seven years ago, MyMoneyBlog.com showed GMO’s seven year forecast as of July 31, 2013.

As you can see, GMO predicted 6.8% real returns for emerging markets and 2.1% to 2.4% returns for other international stocks. GMO predicted a negative real returns for U.S. stocks except for U.S. “high quality.” GMO defines this as companies with a record of high and stable profitability and low leverage.

GMO was wildly inaccurate, with U.S. stocks nearly turning in double-digit real returns (instead of a loss) and trouncing emerging markets, as shown below.

Vanguard’s forecast has been quite inaccurate as well. For many years, Vanguard has been predicting international to significantly outperform U.S. stocks and its economic model is saying international will outperform with less risk. And, of course, Research Affiliates’ smart beta funds haven’t done well over the past several years, as they have heavily favored value over growth.

Addiction to prediction

Market predictions, even long-term predictions, are not only worthless but dangerous. The human mind likes order and hates randomness. Thus, we and our clients try to predict the future. Whether it’s making a killing with an super-volatile stock like GameStop (GME) or picking parts of the market that will outperform, these strategies lead to lower overall returns, especially in the long-run.

Yet it could be time for emerging markets to outperform and emerging market value, which in particular has had dismal performance. The SPDR S&P Emerging Markets Dividend ETF (EDIV) performed in the bottom fifth percentile over the past five years and the bottom one percentile over the past year. It’s an extremely value-oriented fund.

Last year, emerging market returns of 15.3% still lagged the U.S. at 21.0%, using VWO and VTI total-return numbers. As of February 10 of this year, VWO has clocked in a 10.8% return versus only 5.8% for VTI. It might be a short-term blip or the beginning of a seven-to-10-year period of outperformance. But EDIV again underperformed with a 5.0% return, which is less than half the return of emerging markets as a whole and slightly lower than U.S. stocks.

How to Invest in emerging markets

I believe in emerging market stocks but not enough to overweight them as part of the portfolio in international stocks. I prefer a total-international stock index fund that includes emerging markets.

But you or your clients may not agree. The core and explore philosophy states that large-cap U.S. stocks are an efficient market but small cap, international, and especially emerging markets aren’t. Thus it’s okay to pay a bit more for an active manager.

I’ve always rejected this argument and I’ll explain why in a bit. William Sharpe’s arithmetic of active management states that:

If "active" and "passive" management styles are defined in sensible ways, it must be the case that:

- before costs, the return on the average actively managed dollar will equal the return on the average passively managed dollar; and

- after costs, the return on the average actively managed dollar will be less than the return on the average passively managed dollar.

These assertions hold for any time period. Moreover, they depend only on the laws of addition, subtraction, multiplication and division. Nothing else is required.

You can see this play out in looking at the Vanguard Small Cap Index fund (VB) which, according to Morningstar, has performed in the top seventh percentile of its peers in the last five years and the top fourth percentile over 15. Adjusting for survivor bias, performance was even stronger.

I fully expected to see similar data for emerging markets. I was wrong. The Vanguard VWO fund performed in the 58th percentile over 10 years and 55th over 15 years. Both were slightly below average. The data did not support my hypothesis. Darn it!

I looked into the Morningstar peer-group benchmarks for diversified emerging market funds. The top-performing fund over the last decade was the American Funds New World R5 (RNWFX), which earned 8.22% annually over the last 10 years ending February 5, 2001. That nearly doubled the 4.19% of the Vanguard Emerging Markets ETF (VWO). I examined the current portfolio of the American Fund and found it was comprised of:

- Nearly 20% U.S. stocks;

- Microsoft was its single largest holding; and

- Nearly 26% international-developed stocks.

During the same 10-year period, U.S. stocks earned 13.85% annually and international developed earned 5.69% annually or 1.5% percentage points a year more than emerging markets. I calculated the return of an index fund portfolio of 20% US stocks, 26% International developed, and 54% emerging markets over the 10-year period at 7.17% annually, which means that nearly 75% of the outperformance can be explained by benchmarking against only one category. The other 1.02 percentage points was outperformance and, of course, an index fund will never be the top performing fund. It’s not surprising that a fund could outperform by a percentage point a year.

Does indexing work in emerging markets? Elisabeth Kashner, director of ETF research at FactSet told me:

Indexing works as well in emerging markets as it does in the developed countries, because the law of averages applies globally. No matter the region or development status, every overweight has a corresponding underweight. One of these positions will be profitable; the other will not. After costs, the expected return of active risk is negative. Broad-based, cap-weighted indexes maintain market weighting, thus eliminating active risk. Emerging markets may provide a higher dispersion of returns than developed markets, and therefore the opportunity to win or lose by higher margins. At the end of the day, market efficiency is not a prerequisite for indexing. Instead, it all comes down to the law of averages.

David Blanchett, head of retirement research for Morningstar’s Investment Management group, agrees. After examining the data, he stated “indexing works everywhere.”

Conclusion

I don’t know if emerging markets will outperform over the next 7-10 years but it’s unlikely it will lag the U.S. as much as it has over the past. I predict the expert predictions will at least be less wrong. The same is true for value, as it would be unlikely to underperform as much as it has over the past several years. I do find it odd that many who embrace value investing are recommending countries with faster growing economies. In other words, the U.S. and Europe are value economies and emerging markets are growth economies. And, of course, one can always buy an emerging-markets value fund and invest in slower growing companies in faster growing economies.

I’m always skeptical of overweighting any part of global markets. That’s especially true when there is a consensus of outperformance.

Indexing works in emerging markets but, if you are going to go active, pick an active fund that is heavily weighted in emerging markets rather than U.S. and developed international stocks. Costs matter so look at the expense ratio rather than past performance.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies and has consulted with many others while at McKinsey & Company.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All